Edward Lim, CFA

First a caveat, I am but a sophomore political analyst and I certainly do not possess any information nor direct lines into the rumbunctious mind of President Trump nor the recalcitrant Iranian supreme council. But I am student of macro-economics, keen reader of history, and certainly prefer data to the cacophony of relentless “experts” going on live TV.

We will list some of our observations and key issues that we will be marking to market as this story develops.

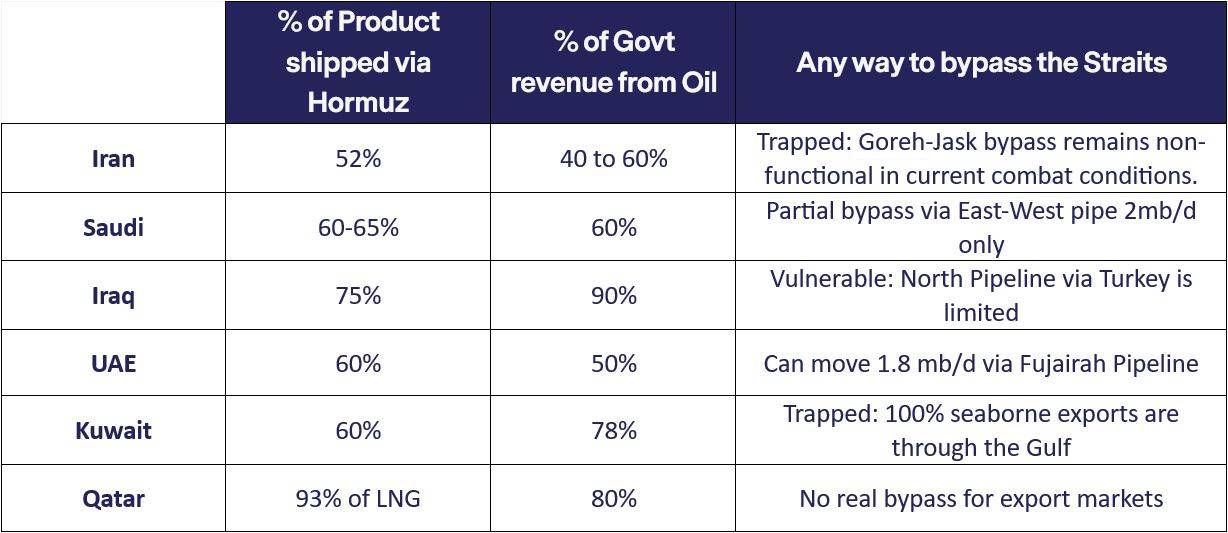

It is a well-known fact that this pivotal waterbody transport 20% of global oil demand, aka 20mn barrel per day. What many commentators failed to mention closing the straits is an economic suicide for Iran. 60% of its oil production is exported (40% is for domestic consumption) and 100% of its export goes through this passageway. 50 to 60% of Iran’s budget is funded by oil export. It is no wonder that the Rial has depreciated 75% since the start of the war. It is estimated that Iran currently stores only 30 days of oil reserve onshore and that is provided the US and Israel does not destroy these storage terminals.

Little is also said that Saudi exports 65% of its oil through the Straits, Iraq 77%, UAE 66%, Kuwait 60% and more than 90% of Qatar’s LNG exports. Each of these countries is highly dependent on oil as revenue ranging from 40 to 90% of their budget. Iran closing of the Straits is not only its own economic suicide, it is a declaration of war on all his neighbours. But it is an ingenious strategy, as Dwight Eisenhower once said, “If you can’t solve your problem, enlarge it”, Iran has intentionally and ironically coalesced friends and foes to wage economic persuasion on their behalf against the protagonists, US and Israel.

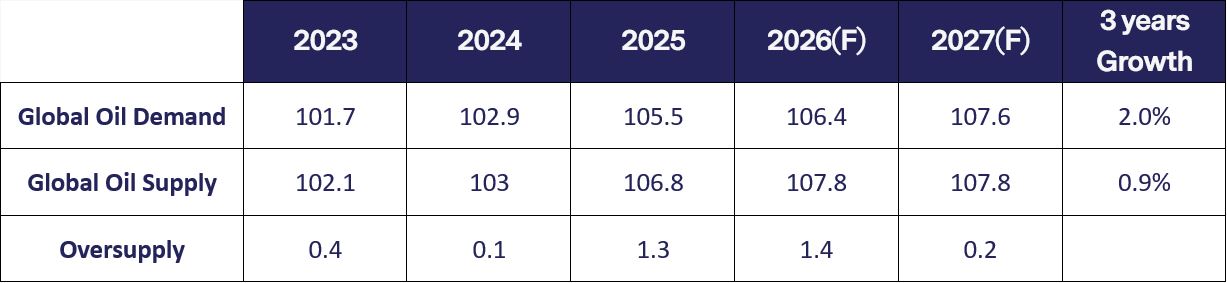

Prior to this war, there was no shortage of oil globally. In fact, the global oil supply was in a glut that lasted 3 years and was expected to increase further in 2026. There is an estimated oversupply of 1.3 to 1.5 mb/d globally driven by supply increases from non-OPEC+ producers that came online in 2023 to 2025 before supply increase abates in 2026 and 2027.

There is also oil on water storage which is estimated to be another 250mn barrels. In addition, most of the developed countries carried 1-2 months of inventory outside of their strategic reserves with China carrying the largest with 102 days’ worth of imports. Under the IEA program, the strategic reserves of 32 countries are estimated at 1.2bn. Hence, if we combine the excess supply of 1.5mb/d, oil on water coverage, inventory build, and a rumoured possibility of IEA coordinating the release of 300-400mb, the global economy can withstand up to 60-90 days of the straits closure before it substantially depletes the excess inventory located across all these channels.

At the point of this publication, oil trades around $100 having doubled in the past few weeks. This is in sharp contract of the declining price trend since it peaked in 2022 post the second Russian-Ukraine war. At $100, the risk premium of oil to its fair value implies market participants are expecting the Straits to be closed for more than 60 days. If that is the eventuality, Iran economy will collapse of what is little left now and there will also be severe ramifications to rest of the world through lower growth and higher inflation.

We are not postulating this will not happen but for the record, the Straits of Hormuz has never been closed, nor is it closed now. Traffic has merely trickled to less than 15% of pre-war traffic. This brings us to the first data point we will be monitoring; how many crossings were made and thanks to AI and plenty of alternative data out there, we can track this every day. Whether the Straits are reopened because of US backstops and protection, or Iran’s largess, or the GCC putting pressure on all parties or some adrenaline seeking captain and crew are of no interest to us. We leave that to the politicians and TV talking heads. All we care about is to see the delta of change in traffic flowing through it improves.

It is reported that during the June 2025 war, Israel has destroyed a significant amount of Iran’s ballistic missiles launchers leaving only 400-500 launchers left. We can never be sure but based on the 300-400 missiles launched in the first two days it does correspond to this capacity. It is reported that US-Israel has since destroyed another 300 units of launchers and it is no surprise the number of ballistic missiles launched has since trickled to a few per day. It could be the IRGC are conserving their resources, retaining their reserves for a ground invasion. As for drones, while the velocity of attack has also slowed, how much more inventory does Iran still have is an unknown. What we do know is the US have targeted the industrial complexes that manufacture them. We have been tracking these exchanges as crude barometers of escalating or diminishing violence.

At the start of the year, our macro views is a pro-growth global economy fuelled by continual capex investments in AI and its ancillary supporting industries, an upsurge in productivity as generative AI integrates into the physical world, a resilient consumer that bends but does not break even as a the labour market stalls and inflation remains sticky and above central banks’ targets. However, we did caution that we are in a mature bull market that started in Oct 2022 and we should be prepared for 15 to 20% correction even absent of a recession. Valuation is a headwind, but earnings growth and revision momentum have remained positive therefore anchoring a pro-risk stance in the portfolio.

As long as we do not have a standstill in the Straits that last more than 60 days, recent developments do not alter significantly the views made at the start of the year. Should oil price stay around $80/bbl but moderate further to $65 by end of the year, Goldman Sachs expects a short-term increase to global inflation of 0.2pp and a 0.1pp drag in global growth. This will not derail pre-war GDP nowcasting global growth of 3.0%, latest PMI implied growth of 2.8%ar, and consensus forecast of 3.3% for 2026. The bigger impact on inflation will be felt in Europe and EM which could truncate the expected path of further easing but historically, central bankers in developed markets has often looked beyond oil supply shocks in calibrating their interest rate policy. On balance, we do not think monetary policy will reverse to tightening because of this development especially given the fluid nature of this conflict and a labour market that is generally weakening across the US, Europe and China. However, should oil stay around $100 over the course of the year, the impact will increase to 0.4pp drag in global growth and inflation to rise by 0.7pp.

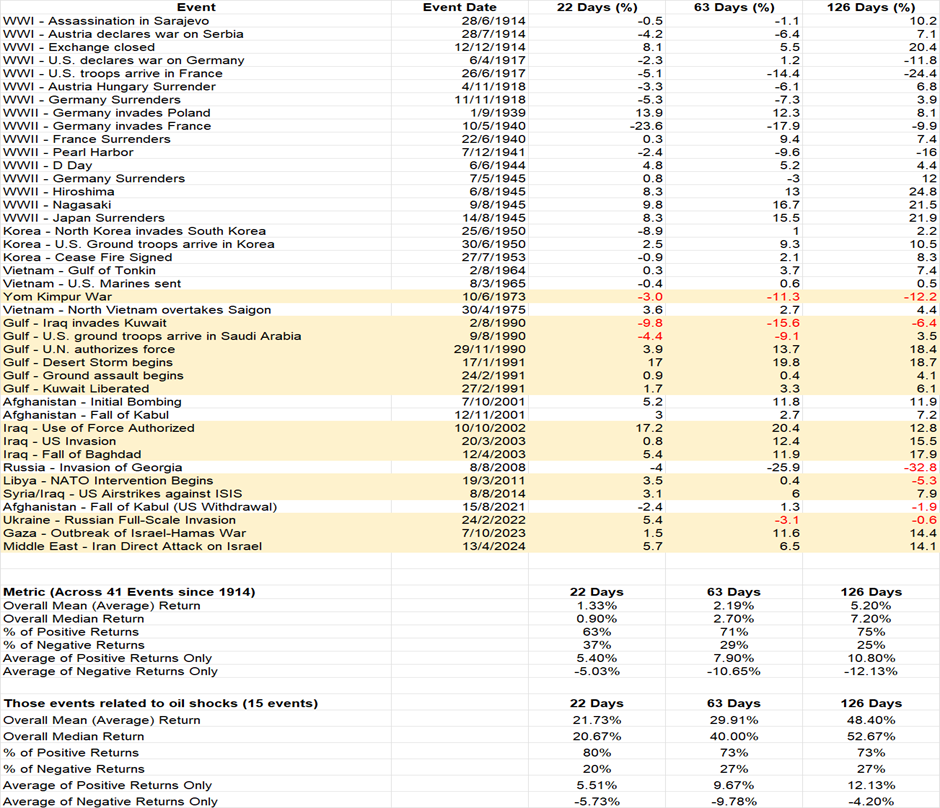

It is easy to be cowered in fear just as it is easy to be lulled into greed. This what makes the stock market function. When we analysed various incidences of conflicts or war since World War I, it is striking the market can look beyond it, most of the time. Across 41 events since 1914, the probability of DJIA Index rising 22, 63 and 126 days after the event is tilted positively with 63%, 71% and 75% of the time with the DJIA rising rather than declining. The average returns of positive outcomes are 5%, 8% and 11% respectively over those time periods. When returns are negative, they are not materially skewed against the positive outcomes. When we further analyse those events that have attendant impact to the oil markets (15 events), the probability of positive returns remained higher than negatives at 80%, 73%, 73% positive returns over 22, 63 and 126 days. The returns of positive outcomes are not dissimilar to the negative returns of 5.5%, 9.7% against -5.7%, -9.8% from 22 to 63 days. But skewed positive after 126 days with average positive returns of 12% versus -4%. Putting them together, there is asymmetry of positive outcomes over the entire series as well as a smaller cohort of events related to oil shocks.

Fixed Income: Unchanged remains underweight. While inflation could increase in the short-term, we expect central banks to look beyond this volatile category and instead focus on downside risk to growth and already tenuous labour market therefore maintaining the status quo on interest rates or with a slight bias to ease. Our fixed income managers have always been conservative in their portfolio construction. Moreover, most of them are duration unconstrained hence will have the flexibility to manage interest rate risk if required. A good example of prudence is our Global Bond Portfolio which is conservatively constructed with target yield and credit quality as the two key considerations. It tends to outperform in difficult markets and so far, year-to-date, it remains positive with a non-material decline in this month. The oil impact on the portfolio will primarily be on airlines in which we have less than 7.5% exposure and offsetting is our energy exposure of 9%. Close to 50% of the portfolio are in relatively defensive sectors like consumer staples, healthcare, utilities and tech (no software issuer, mostly semi and hardware). Yield of the portfolio is 4.98% with coupon of 5.42% and duration of 5 years and remains a BBB investment grade portfolio.

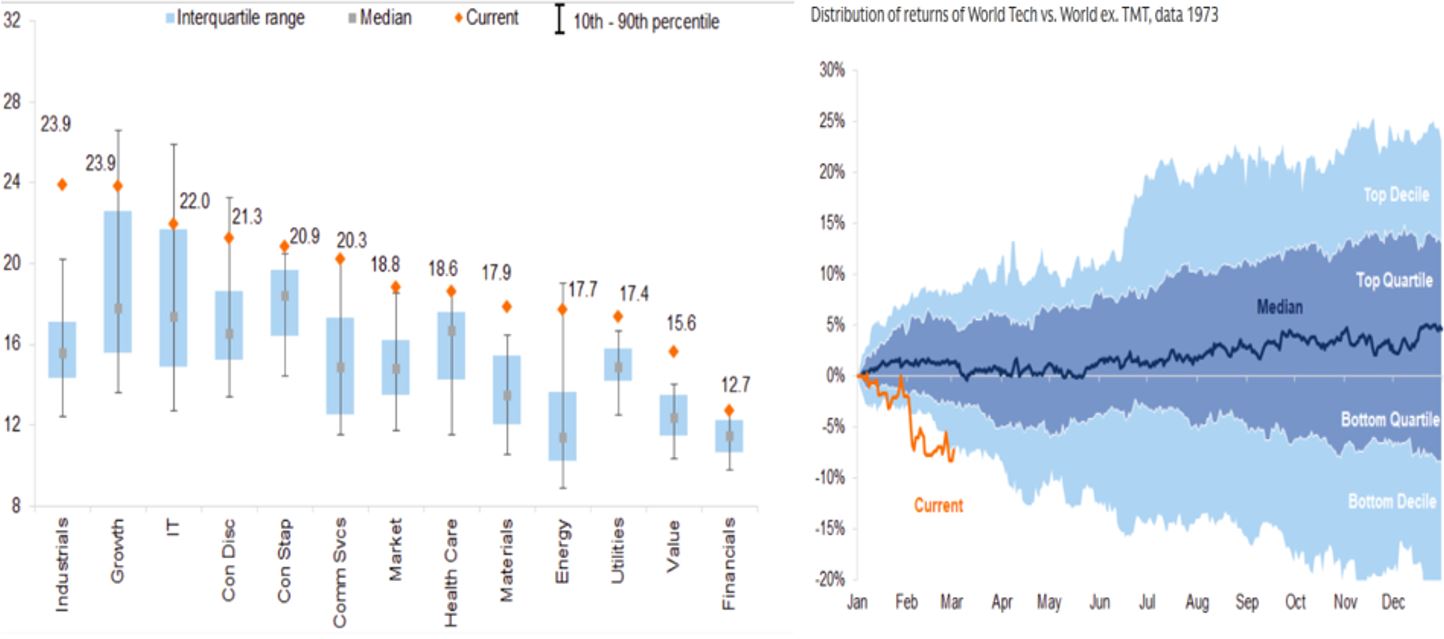

Equities: Remains overweight but vulnerable to growth risk and steep valuations. The equities complex is slightly more complicated than fixed income where yields are high enough to cushion growth and interest rate risks for the latter, but valuations are steep for the former. The current macro regime remains that of Recovery phase even with a modest downgrade from this event, hence, should still favour equities over fixed income. We believe the global economy can withstand 1-2 months of reduced traffic in the Straits but any longer, the transmission mechanism into equities will start to incorporate growth risk but also risk of tighter financial conditions. However, we are seeing interesting opportunities in the tech sector now given that sector has peaked in Oct last year and have corrected ahead of this current war driven by its own idiosyncratic concerns about AI disruption of potential profit pools. Over a 20-year period, tech is now the only sector trading within its interquartile range while the rest of the other sectors are trading closer or above 90th percentile expensive. The year-to-date performance of tech has been the worst it has been in 50 years, and this is extraordinary given that tech sector is forecast to have the highest EPS growth of 45% and 21% 2026-2027 amongst all sectors in contrast to global equities EPS growth of 17% and 14% respectively.

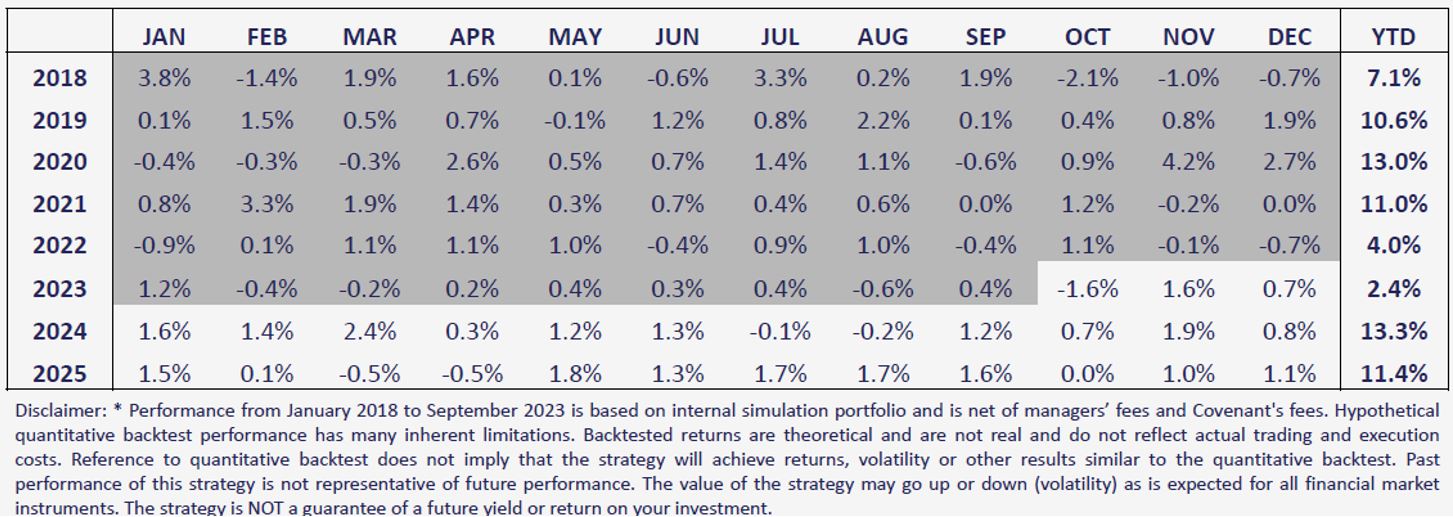

Hedge Funds: As of end of Feb, our fund of hedge funds had an impressive start with an estimated return of 5% so far. We will be compiling a mid-month review in the coming weeks and will keep all informed. It is worth nothing the fund has transversed significant economic and geopolitical events since 2018. These include US-China trade war and quantitative tightening part 1 in 2018, global pandemic in 2020, quantitative tightening part 2 in 2022, oil shock from Russia-Ukraine second war in 2022, Hamas-Israel war in 2023, Liberation Day and the Israel-Iran 12-day war in 2025, and the current second oil shock. And yet throughout this period, it has returned 9%*pa, on volatility of less than 4%, generated more than 75% of positive months with returns that are lowly correlated to the broader equities and bonds. We believe it will continue to do so even in this current climate.

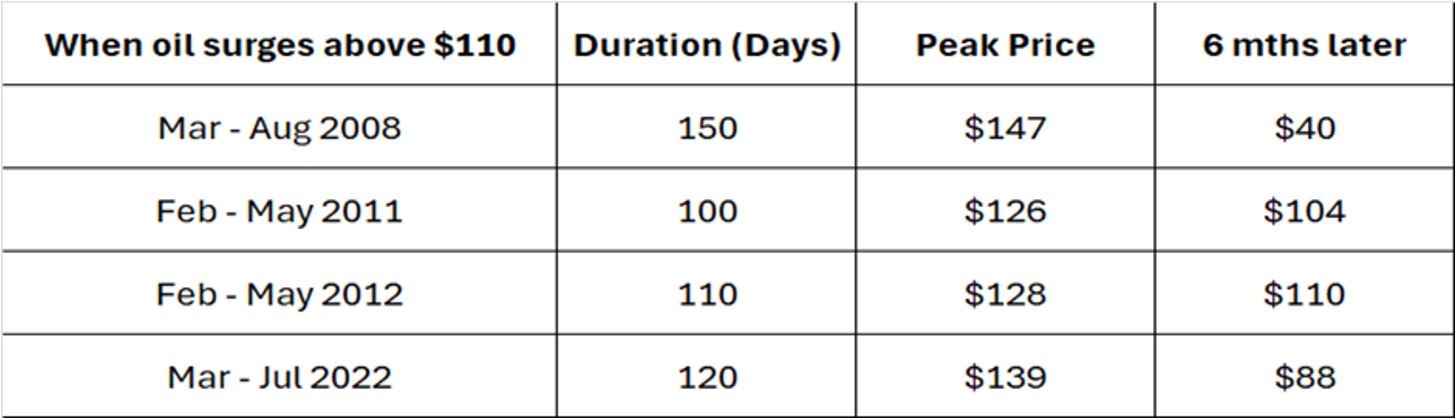

Commodities: Hold on to Gold but too volatile to go either long or short oil. When we trace back to 2008, when oil spikes aggressively, most of these oil shocks do not last forever nor do they establish a new price range. The first oil shock of 2008 when oil price spiked to $147 and many of these so-called top-rated oil analysts called for a new paradigm of $200 oil as the norm, lasted 150 days before spectacularly falling to $40 in the following six months. There is a good economic reason for this. When oil price exceeds $100, we will witness demand destruction. On the supply side, if oil stays above $70, it will encourage significant output and investments. Plus, the emergence of US shale oil, which is the 2nd lowest marginal cost of production after the Middle-east oil fields and is easier and faster to start-stop production than the Middle-east facilities, has often become the marginal supplier at both ends of the price range.

For what it is worth, Goldman Sach commodities team has modelled the potential price range in relation to the length of disruption in the Straits. If you like us do not think the Stratis will be closed for more than three weeks, oil could fall back to $71 according to their analysis. And if it is less than 10 days, it could fall back to $66 per barrel.

Edward Lim, CFA

Chief Investment Officer

edwardlim@covenant-capital.com

Risk Disclosure

Investors should consider this report as only a single factor in making their investment decision. Covenant Capital (“CC”) may not have taken any steps to ensure that the securities or financial instruments referred to in this report are suitable for any particular investor. CC will not treat recipients as its customers by their receiving the report. The investments or services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to your circumstances or otherwise constitutes a personal recommendation to you. The price, value of, and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is affected by changes in a spot or forward interest and exchange rates, economic indicators, the financial standing of any issuer or reference issuer, etc., that may have a positive or adverse effect on the income from or the price of such securities or financial instruments. By purchasing securities or financial instruments, you may incur above the principal as a result of fluctuations in market prices or other financial indices, etc. Investors in securities such as ADRs, the values of which are influenced by currency volatility, effectively assume this risk.

By entering this site you agree to be bound by the Terms and Conditions of Use. COVENANT CAPITAL PTE LTD (“CCPL”) is a Capital Markets License (AI/II) holder and regulated by the Monetary Authority of Singapore (‘MAS’).

By using this site you represent and warrant that you are an accredited investor or institutional investor as defined in the Singapore Securities and Futures Act (Chapter 289). In using this site users represent that they are an accredited and/or Institutional investor and use this site for their own information purposes only.

The information provided on this website by Covenant Capital Pte Ltd (CCPL) is intended solely for informational purposes and should not be construed as investment advice. It does not constitute legal, tax, or other professional advice. CCPL strongly recommends consulting qualified professionals for personalized guidance. The website does not offer or solicit securities transactions, and users are expected to comply with local laws. Accredited and institutional investors in Singapore may access the information solely for informational purposes.

What types of Personal Data do Covenant Capital collect?

Personal data is any information that relates to an identifiable individual, and we may collect this information when you interact with our staffs:

1. Personal Particulars (e.g. name, address, date of birth)

2. Tax, Insurance and employment details

3. Banking information and financial details

4. Details of interactions with us (eg. Images, voice recordings, personal opinions)

5. Information obtained from mobile devices with your consent

How do we collect your Personal Data?

Below are the ways that we collect your data:

1. Investment Management Agreement forms, Risk Profile forms, Subscription forms;

2. Via emails, SMSes, Whatsapps, phone calls or any other digital means to the office or its’ staffs;

3. Photos and videos of you from our events; and

4. Information about your use of our services and website, including cookies and IP address

How do we use your Personal Data?

1. For General Support

Verify your identity before providing our services, or responding to any of your queries, feed-back and complaints.

2. For our Internal Operations

a. Aid our analysis so that the company can improve our services and products.

b. Manage the company’s day-to-day business operations.

c. Ensure that the information that the company have on you is current and up to date.

d. Conducting Due Diligence checks to reduce Money Laundering and Terrorist

3. Financing Schemes

e. Comply with all laws and obligations from any legal authorities.

f. Seek professional advice, including legal.

g. Provide updates to you.

4. Posting on LinkedIn and Website

We may post personal data, including pictures and videos, on our LinkedIn page and website for purposes such as:

Who do we share your Personal Data with?

1. Any officer or employee of the company and its related companies;

2. Third parties (and their sub-contractors if applicable) that works with us, such as Custodian Bank of choice, Fund Administrators for the Funds that we manage, any third party Fund’s Administrators, IT support who back up our database and other service providers;

3. Relevant authorities such as government or regulatory authorities, statutory bodies, law enforcement agencies.

4. Relevant authorities such as government or regulatory authorities, statutory bodies, law enforcement agencies.

5. We require all personnel of the company and third party to ensure that any of your data disclosed to them is kept confidential and secure

6. We do not sell your Personal Data to any third party, and we shall comply fully with any duty and obligation of confidentiality that governs our relationship with you

When the company discloses your personal data to third-parties, the company will, to the best of its abilities, exercise reasonable due diligence that they are contractually bound to protect your personal data in accordance with applicable laws and regulations, save in cases where by your personal data is publicly available.

Accessing and Correction Request and Withdrawal of Consent

Please contact your advisor/banker or alternatively you can contact ccops@covenant-capital.com should you have the following queries.

1. Regarding the company’s data protection policies and processes

2. Request access to and/or make corrections to your personal data in the company’s possession; or

3. Wish to withdraw your consent to our collection, use or disclosure of your personal data.

The company endeavours to respond to you within 30 days of the submission.

Should you choose to withdraw your consent to any or all use of your personal data, the company might not be able to continue to provide any further services or maintain further relationships. Such withdrawal may also result in the termination of any agreement or relationship that you have with us.

Complaints

If you wish to make a complaint with regards to the handling and treatment of your personal data, please contact the company’s Data Protection Officer, mentioned below, directly. The DPO shall contact you within 5 working days to provide you with an estimated timeframe for the investigation and resolution of your complaint.

Should the outcome of the resolution is not satisfactory, you may refer to the Personal Data Protection Commission (PDPC) for any further resolutions.

If you have any doubt, please contact Mr Tay Kian Ngiap, the PDPA Data Protection Officer for Covenant Capital Pte. Ltd. He can be reached at kntay@covenant-capital.com

By accessing this website, you hereby agree to the terms listed on the website, all applicable laws and regulations, and agree that you are responsible for compliance with any applicable local laws. Any claim relating to Covenant Capital’s website shall be governed by the laws of the Republic of Singapore without regard to its conflict of law provisions.

1. License to Use

Permission is granted to download information and materials on Covenant Capital’s website for personal, non-commercial viewing only. This is the grant of a license, not a transfer of title, and under this license you may not:

i) modify or copy the information and materials;

ii) use the information and materials for any commercial purpose, or for any public display (commercial or non- commercial);

iii) attempt to decompile or reverse engineer any software contained on Covenant Capital’s web site;

iv) remove any copyright or other proprietary notations from the materials; or

v) transfer the materials to another person or “mirror” the materials on any other server.

All content, including but not limited to logo, tagline, graphics, images, text contents, buttons, icons, design and structure are property of Covenant Capital. All content on this website is protected by copyright, patent and trademark laws.

The Covenant Capital logo should not be used for any purpose whatsoever beyond what is available on the website, unless you have obtained written approval from us.

2. Disclaimer

The materials on Covenant Capital’s website are provided “as is”. Covenant Capital makes no warranties, expressed or implied, and hereby disclaims and negates all other warranties, including without limitation, implied warranties or conditions of merchantability, fitness for a particular purpose, or non-infringement of intellectual property or other violation of rights. Further, Covenant Capital does not warrant or make any representations concerning the accuracy, likely results, or reliability of the use of the materials on its Internet web site or otherwise relating to such materials or on any sites linked to this site.

It is your responsibility to evaluate the accuracy, completeness, or usefulness of any information, advice and other content available through this website.

You should not solely rely on the information, advice and other contents available on our website for decisions on investment(s) or decision with respect to our company’s products and services. You are advised to seek additional information required for you to make sound, well-informed and reasonable decision.

3. Limitations

In no event shall Covenant Capital or its suppliers be liable for any damages (including, without limitation, damages for loss of data or profit, or due to business interruption,) arising out of the use, inability to use or user’s reliance on the materials obtained through Covenant Capital’s web site, even if Covenant Capital or a Covenant Capital authorized representative has been notified orally or in writing of the possibility of such damage.

4. No Offer

Nothing in this website constitutes a solicitation, an offer, or a recommendation to buy or sell any investment instruments, to effect any transactions, or to conclude any legal act of any kind whatsoever. The information on this web site is subject to change (including, without limitation, modification, deletion or replacement thereof) without prior notice. When making decision on investments, you are advised to seek additional information required for you to make sound, well-informed and reasonable decision.

5. Revisions and Errata

The materials appearing on Covenant Capital’s website may include technical, typographical, or photographic errors. Covenant Capital does not warrant that any of the materials on its website are accurate, complete, or current. Covenant Capital may make changes to the materials contained on its website at any time without notice. Covenant Capital does not, however, make any commitment to update the materials.

6. Site Terms of Use Modifications

Covenant Capital may revise these terms of use for its web site at any time without notice. By using this website you are agreeing to be bound by the then current version of these Terms and Conditions of Use. If any of the term or change is deemed not acceptable to you, you should not continue to browse this site.

Your privacy is very important to us and we respect your online privacy. This Policy has been developed in order for you to understand how we collect, use, communicate and disclose and make use of personal information. We are committed to conducting our business in accordance with these principles in order to ensure that the confidentiality of personal information is protected and maintained.

1. Collection and Use of Information

We may collect personal identifiable information, such as names, postal addresses, email addresses, etc., when voluntarily submitted by visitors to our website. This information is only used to fulfill your specific request, unless further permission is provided to us to use it in any other manner or for any other purpose.

2. Web Cookies / Tracking Technology

A cookie is a small file which seeks permission to be placed on your computer’s hard drive. Once you are agreeable to the use of cookies, the file is added and the cookie helps analyse web traffic and tracks visits to a particular website. Cookies allow web applications to respond to you as an individual. The web application can tailor its operations to your needs, likes and dislikes by gathering and remembering information about your preferences.

We use traffic log cookies to identify which pages are being used. This helps us analyse data about website traffic and improve our website in order to tailor it to customer needs. We only use this information for statistical analysis purposes and then the data is removed from the system.

Overall, cookies help us provide you with a better website by enabling us to monitor which pages you find useful and which you do not. A cookie in no way gives us access to your computer or any information about you, other than the data you choose to share with us.

You can choose to accept or decline cookies. Most web browsers automatically accept cookies, but you can usually modify your browser setting to decline cookies if you prefer. This may prevent you from taking full advantage of the website.

3. Links to other websites

Our website may contain links to other websites of interest. However, once you have used these links to leave our site, you should note that we do not have any control over that other website. Therefore, we cannot be responsible for the protection and privacy of any information that you provide whilst visiting such sites, and this privacy statement does not govern such sites. You should exercise caution and review the privacy statement applicable to that particular website.

4. Distribution of Information

We will not sell, distribute or lease your personal information to third parties unless we have your permission or are required by law to do so. We may use your personal information to send you promotional information about third parties’ products or services, which we think you may find interesting if you tell us that you wish this to happen.

If you believe that any information we are holding on you is incorrect or incomplete, please write to or email us as soon as possible at the above address. We will promptly correct any information found to be incorrect.

When required by law, we may share information with governmental agencies or other companies assisting in the investigations. The information is not provided to these companies for marketing purposes.

5. Commitment to Data Security

To make sure your personal information is secured, we communicate our privacy and security guidelines to all Covenant Capital’s employees and strictly enforce privacy safeguards within the company.

Your personal identifiable information is kept secure. Only authorised employees, agents and contractors who have a direct need to access the information will be able to view this information.

We reserve the right to make changes to this policy. Any changes to this policy will be posted.