Josh Le, CFA, MSc in FE

Global equities delivered another strong quarter despite heightened volatility. The MSCI AC World Index (ACWI) rose +14.2% in 2Q (YTD: +11.7%), recovering sharply from the Iran-war correction before pausing modestly in June. Performance was driven primarily by AI beneficiaries and resilient corporate earnings. This quarter’s commentary focuses on two key themes: the debate over a potential AI bubble, and where we still see earnings opportunities and upside in equity markets.

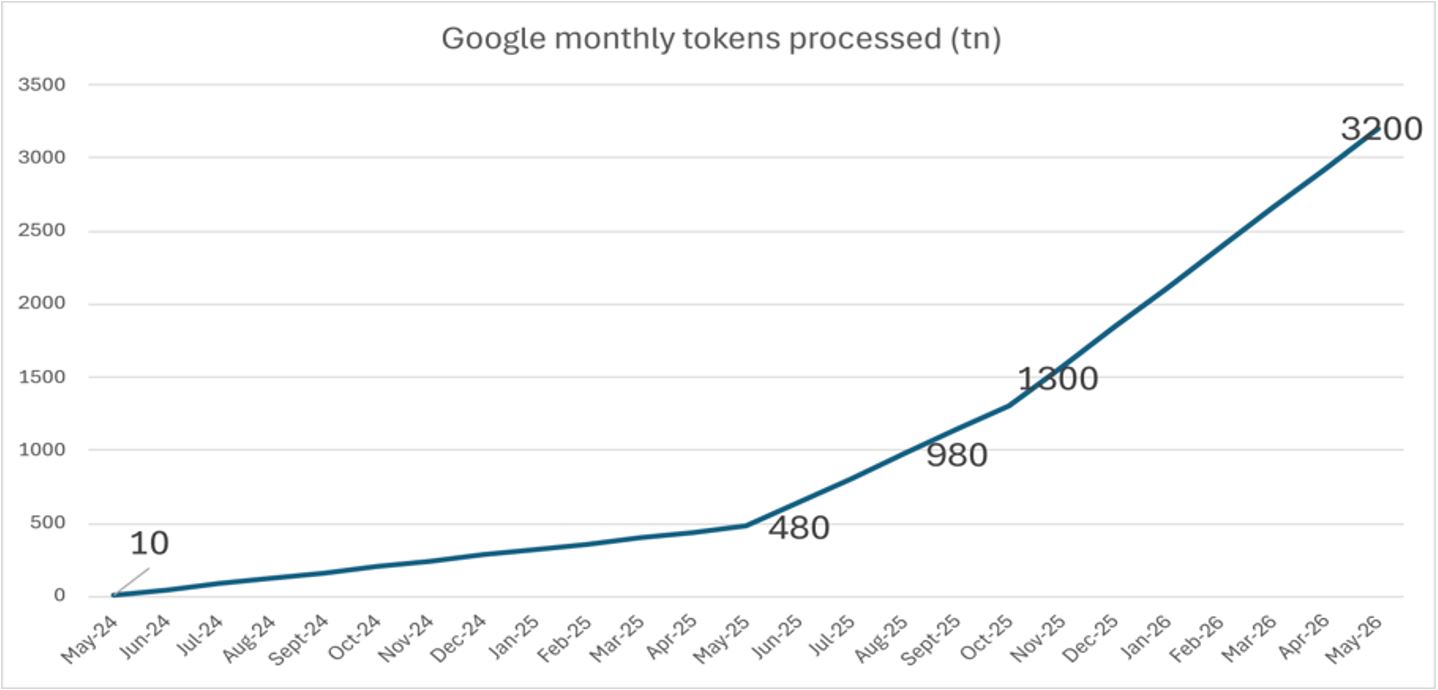

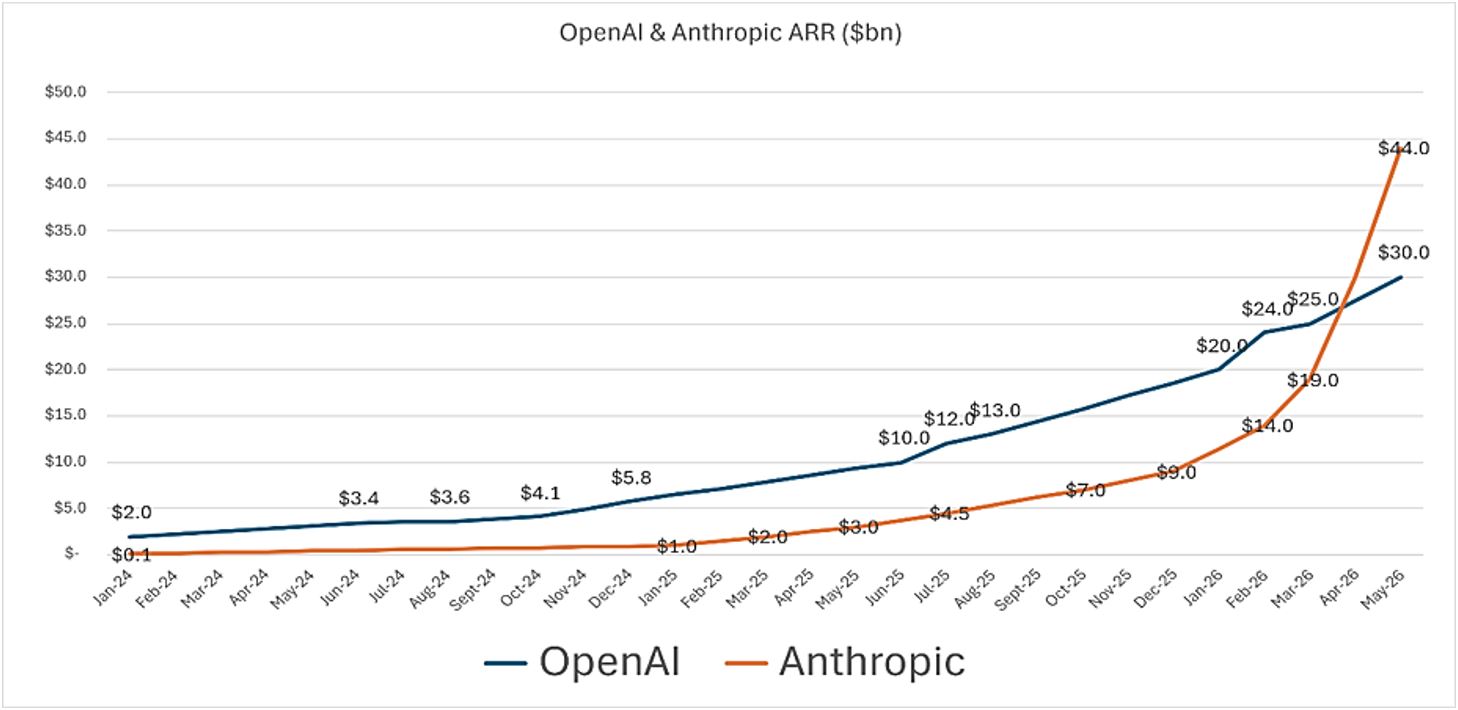

As AI continues to dominate market headlines, questions surrounding a potential AI bubble have inevitably resurfaced. Based on fundamentals, we believe that the public market is not yet in a bubble. First of all, AI adoption continues to accelerate across multiple metrics that we monitor, including the growth of the token-economy (figure 1), revenue expansion among AI “platform” companies (figure 2), and tangible productivity gains across an increasingly broad range of industries (figure 3).

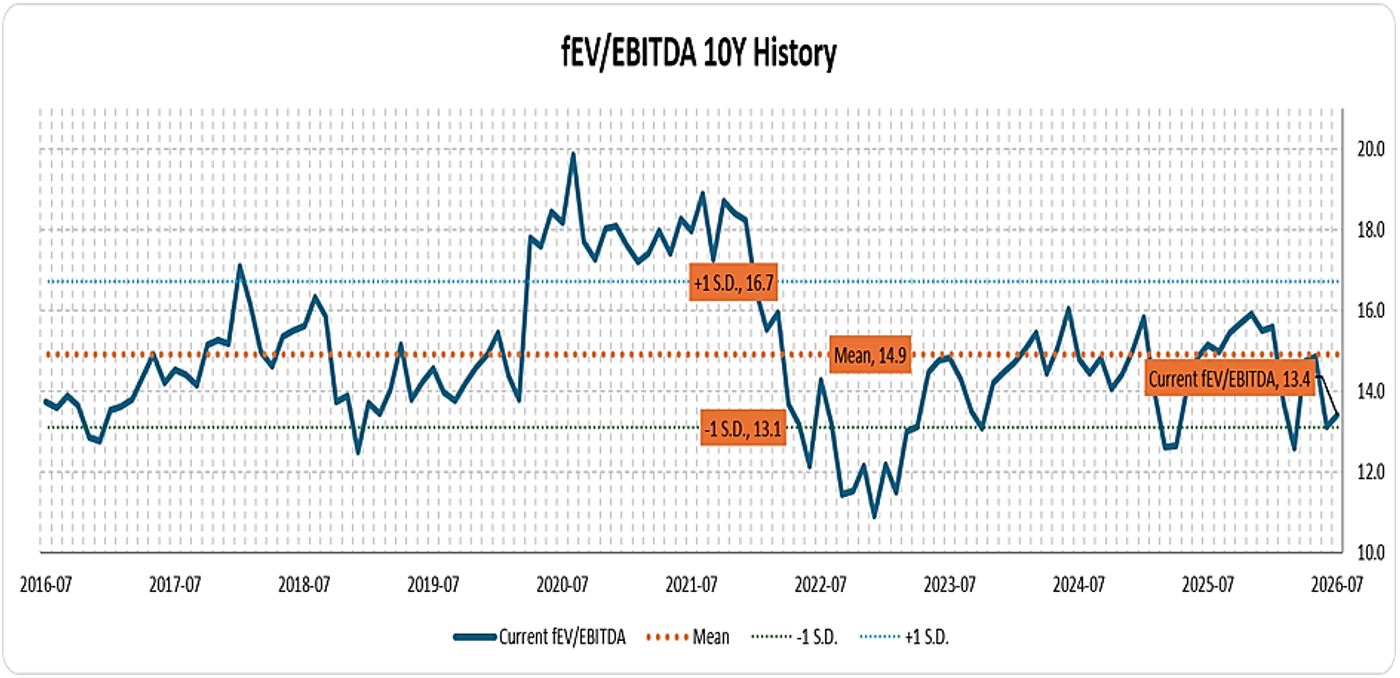

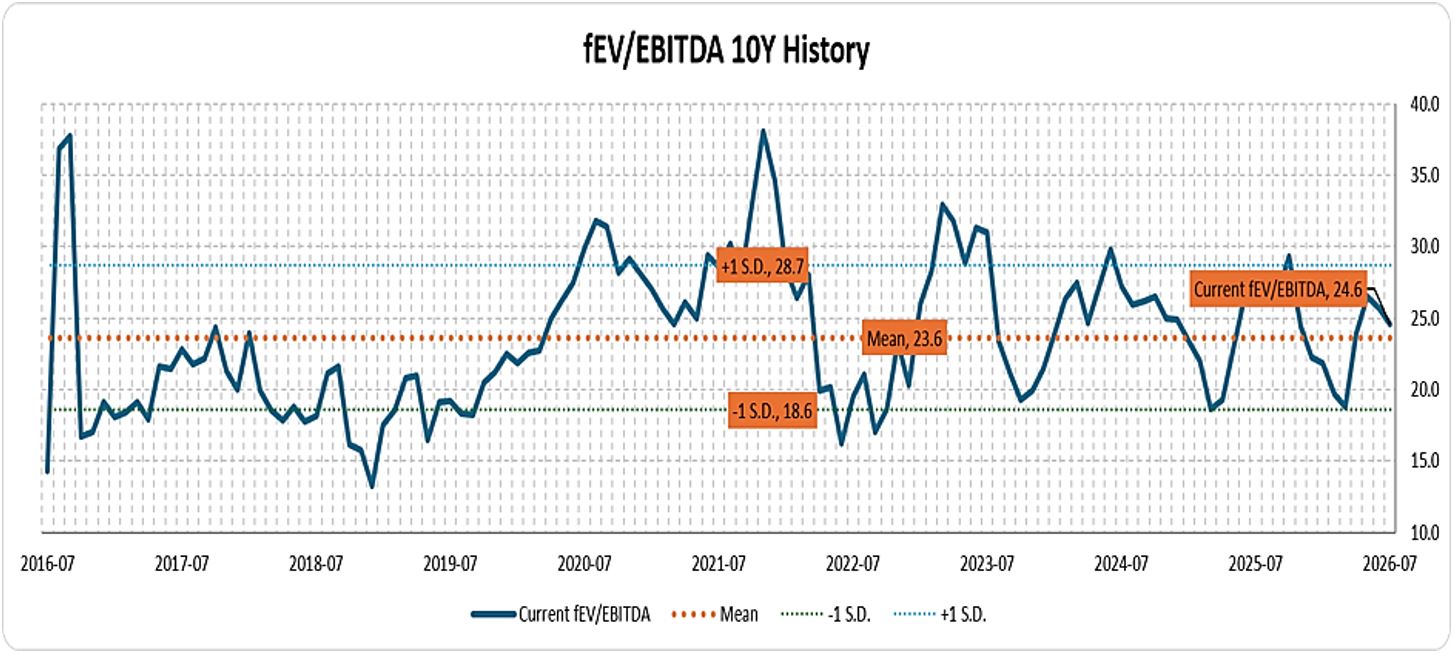

Secondly, valuations in the public market are not at all detached from fundamentals and are well-supported by earnings growth. The broad market indices, the MSCI AC World and the S&P 500, are currently trading at fPE of 17.4x/19.9x respectively, underpinned by robust 2026–2027 EPS CAGR of +20.4% p.a and +19.1% p.a, alongside record corporate profit margins. Moreover, across the AI value chain, valuations also remain broadly reasonable.

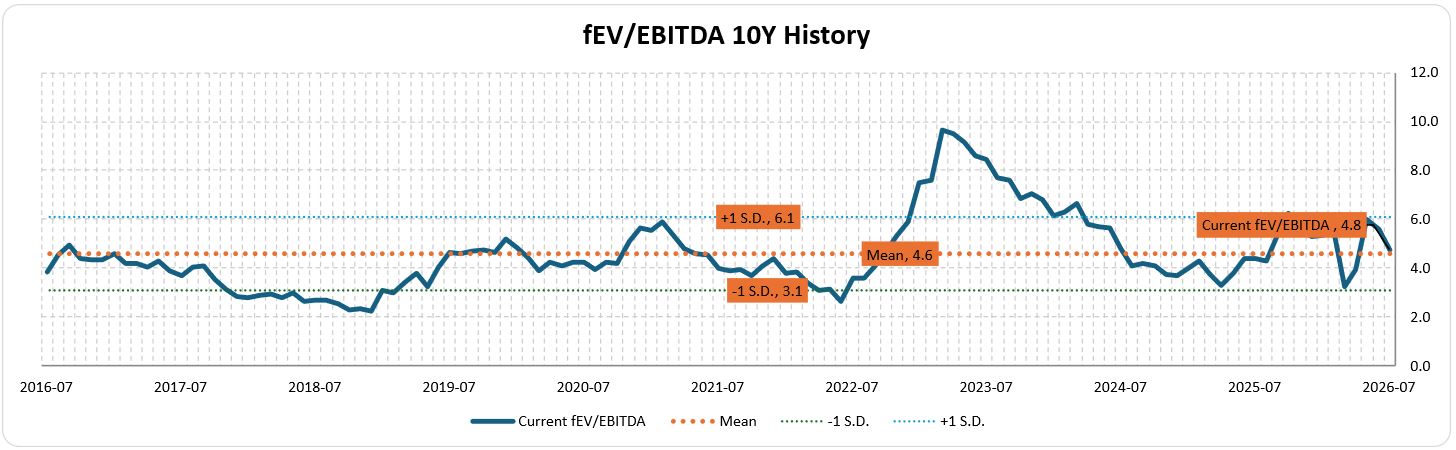

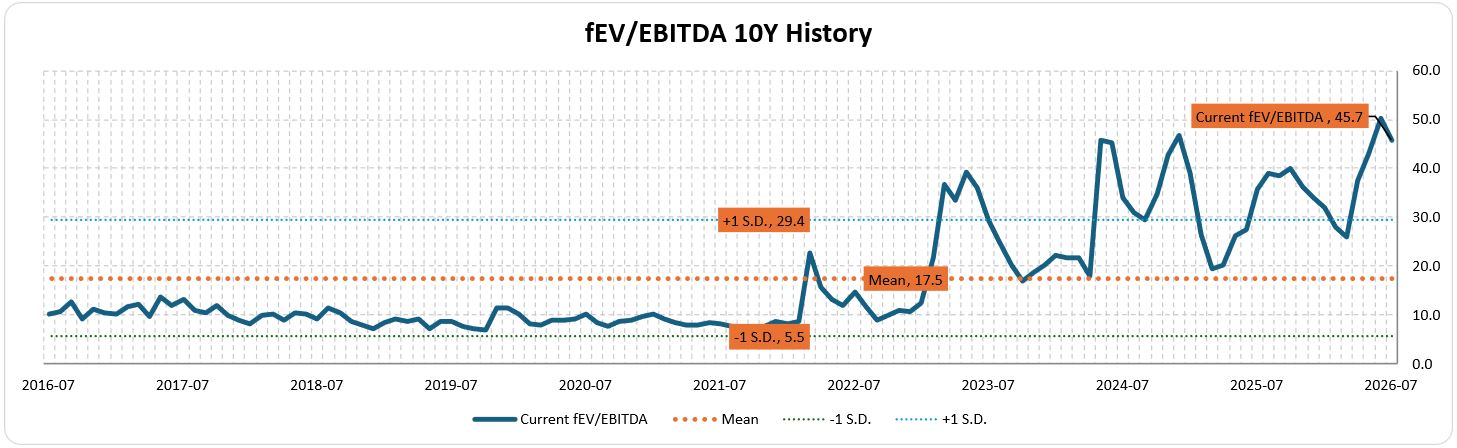

The only segment where valuations appear relatively elevated is the pure-play networking and optical companies, reflecting emerging demands from datacenter’s scale-across, accelerating adoption of silicon photonics (SiPh) and co-packaged optics (CPO), as well as hyper-growth experienced by several industry leaders:

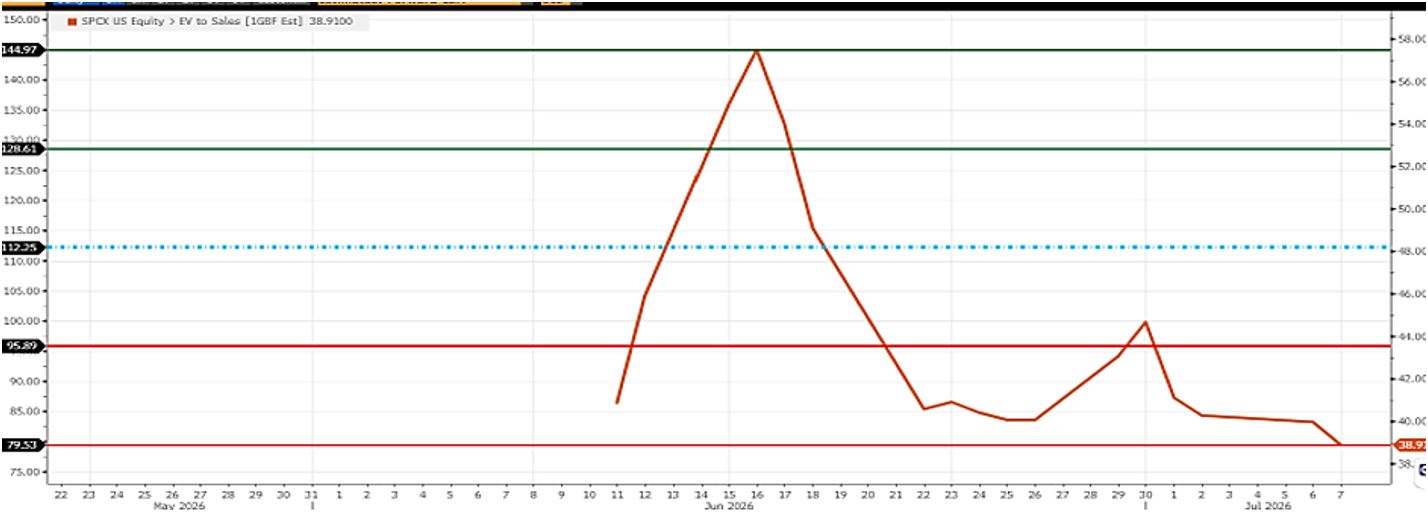

Secondly, we have previously argued that valuations in the private market have been frothier compared to the public market. As a new wave of AI-related IPOs, from SpaceX to anticipated listings of OpenAI and Anthropic, draws closer, investors have questioned the implications for public market valuations. Our view is that the valuation premium currently enjoyed by many private companies is more likely to compress after listing, converging towards the valuation multiples of established public peers, much like what Cerebras and Coreweave have experienced. So far, we have observed no significant shake-ups in the public market post these IPOs.

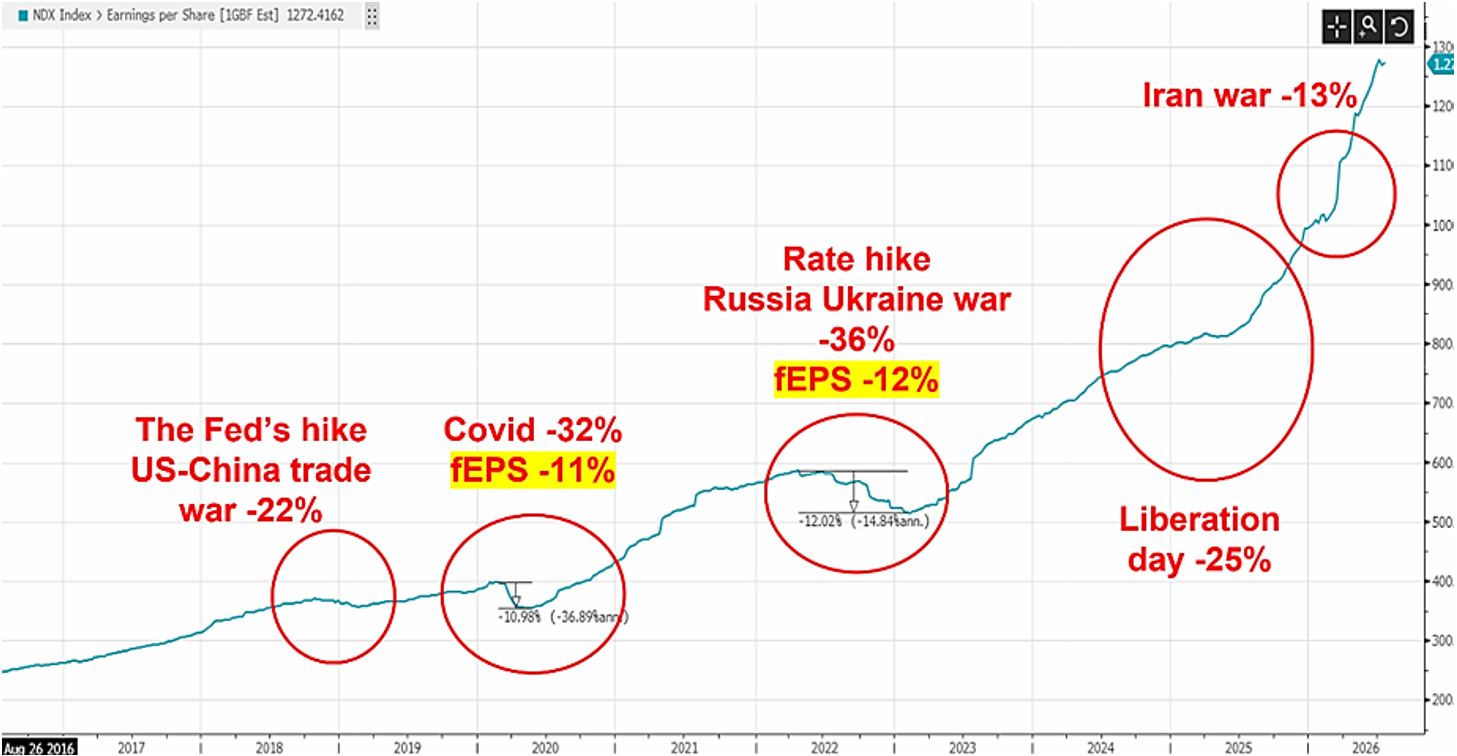

Nevertheless, while “fundamental momentum” remains robust for our AI pick-and-shovel names, investors should not rule out meaningful reversals in “price momentum”, induced by the unwinding of crowded trades, macro noise, and persistent concerns about AI CapEx and ROI. History reminds us that even during periods of robust earnings growth, both the Semiconductor Index (SOX) and the Nasdaq have experienced drawdowns of 20-40% or more. The below figure shows that the Tech-heavy Nasdaq index often experiences large pullbacks in the last 10 years.

However, with the exception of the Covid-induced selloff in 2020 and the Fed’s tightening cycle in 2022 during which forward EPS declined by -11% and -12%, respectively, most other corrections saw stable earnings.

Such volatility is a normal feature of secular growth investing rather than evidence of a broken investment thesis. This is a reminder for us to stay selective in our stock picks, focus on owning high-quality businesses with durable competitive advantages, maintain discipline around valuations and target prices, and actively adjust position sizing to manage downside risk.

Another key driver of the equity markets this quarter was the robust corporate earnings. The S&P 500’s 1Q26 EPS tracked +28% yoy growth, a significant beat compared to +12% yoy growth expectation pre-earnings season. These results raised the MSCI AC World and S&P 500’s FY2026 EPS yoy growth estimates to +24.2%/+23% yoy, respectively, from +13.6%/14% at the beginning of the year.

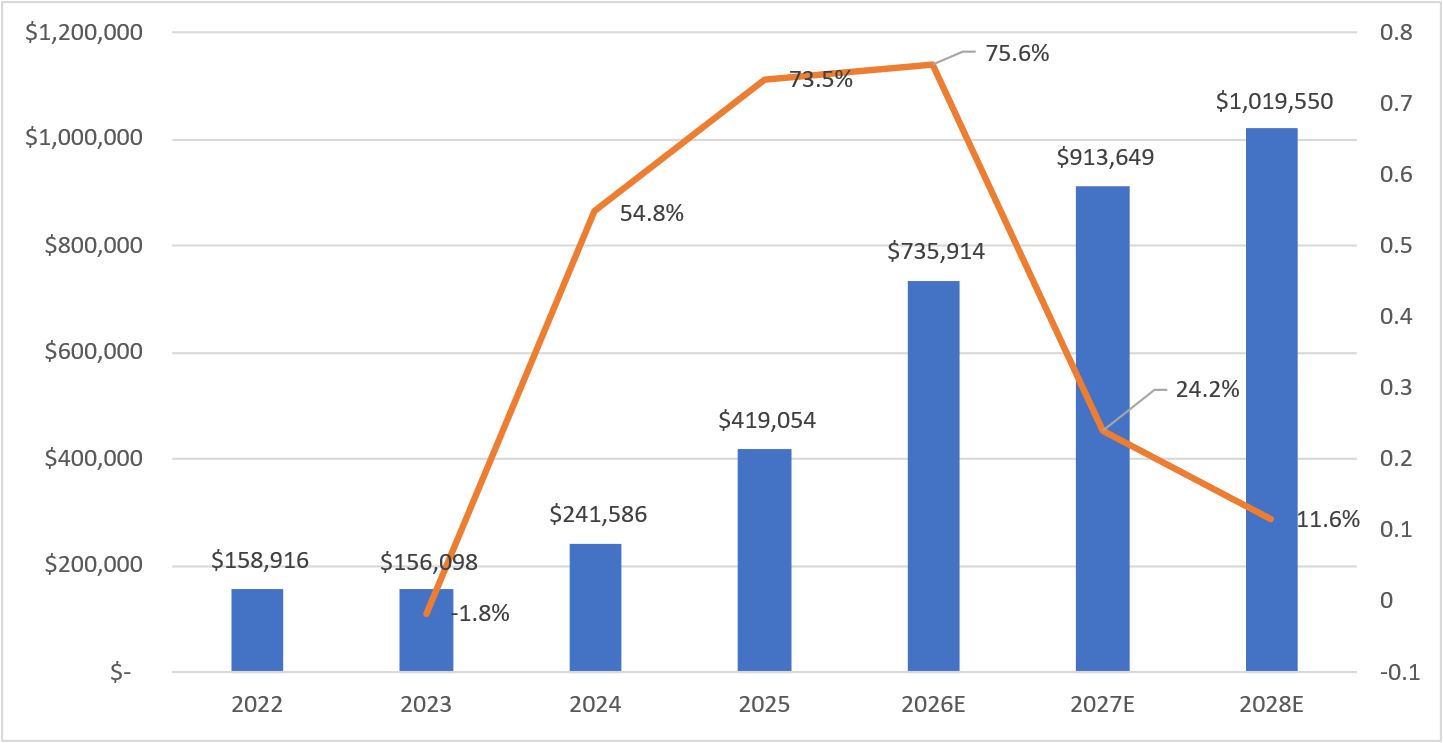

The main catalyst of earnings upgrades has been the continued surge in hyperscalers’ AI CapEx. The 2026 CapEx estimate now stands at ~$736bn, reflecting a sharp acceleration to +75.6% yoy growth, compared to the expectation of +33% growth earlier in the year.

One important takeaway from the earnings season is the accelerating growth across hyperscalers’ cloud businesses: Alphabet’s GCP +63% yoy, Microsoft’s Azure +40% yoy, and Amazon’s AWS +28% yoy. Additionally, these companies have debunked the market’s belief that their margins would compress heavily thanks to AI investments. GCP and AWS delivered 400-600 bps beat on their cloud margins, prompting analysts to upgrade their margin forecast meaningfully.

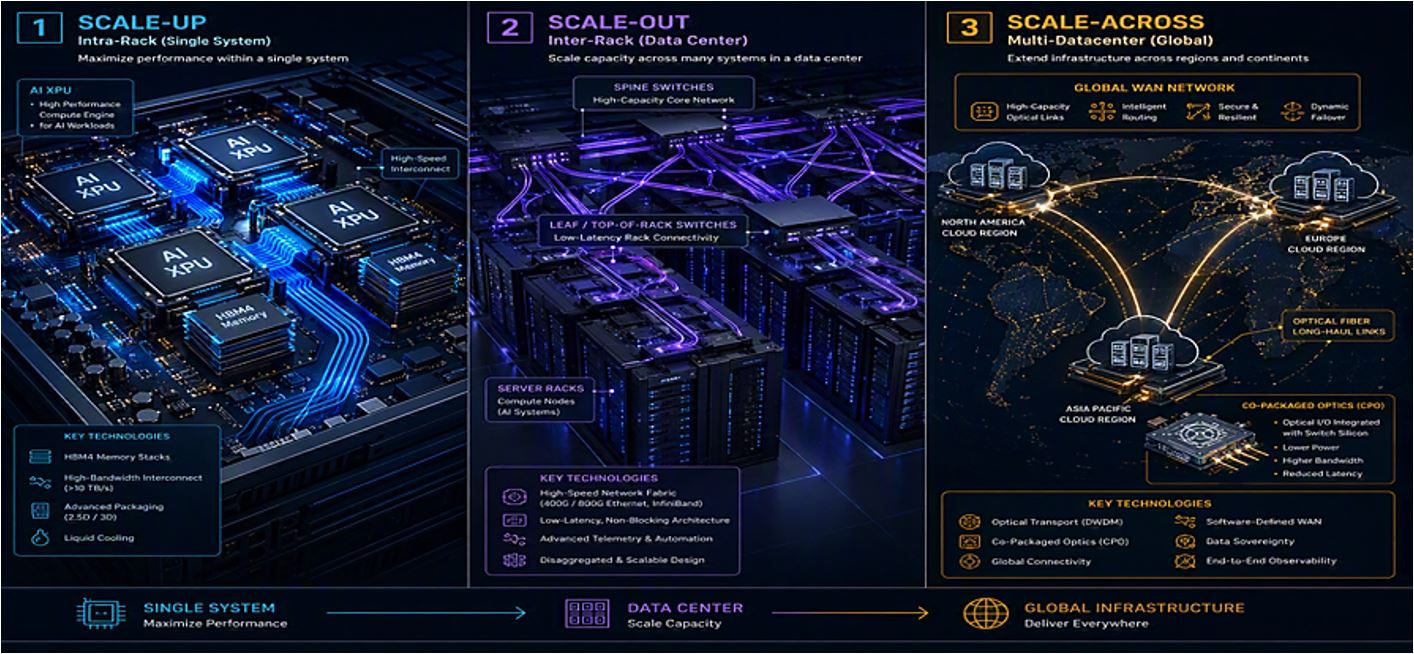

This trend continues to benefit our infrastructure plays, particularly semiconductor and infrastructure software companies. In the recent years, we have positioned to benefit from AI’s “scale-up”, “scale-out” and “scale-across” trends:

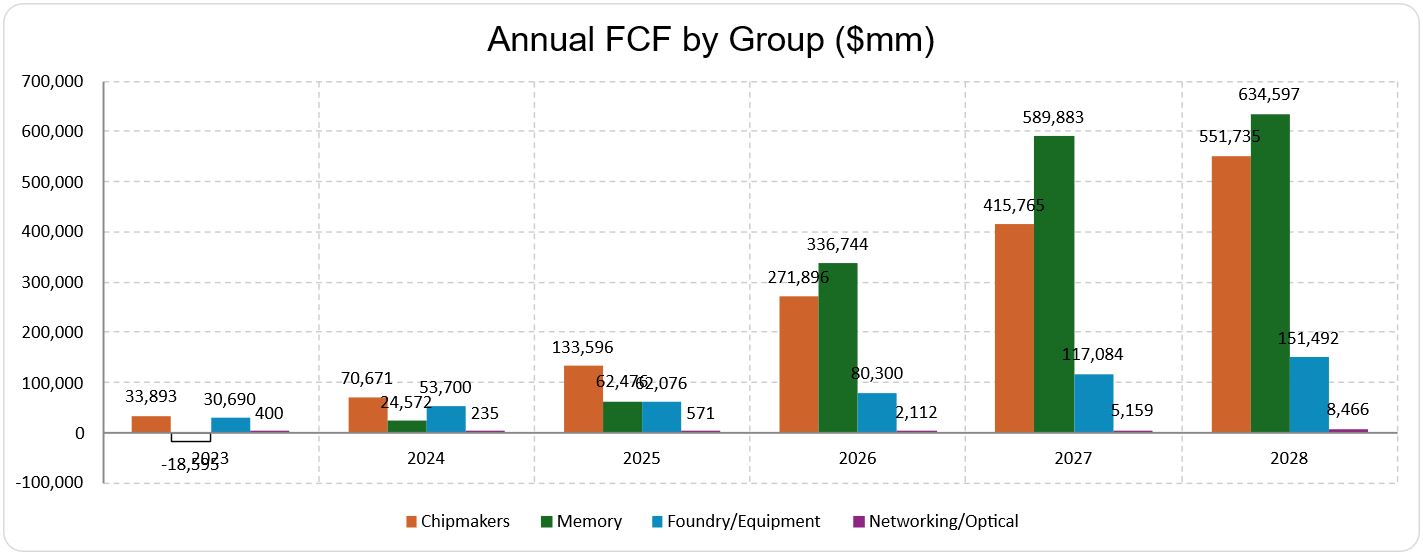

… and across different segments: ASIC chipmakers (Broadcom, Marvell), memory (Micron), semi-equipment (ASML) and networking/optical (Astera Lab, Lumentum) as the AI CapEx continued to translate into their free cash flow (FCF):

Nonetheless, we did not maintain exposure to CPUs after closing our AMD and Arm holdings positions in 2025. Given the view that Agentic AI requires 3-5x the CPU cores to GPU ratio compared to traditional AI training, we estimate that the TAM (total addressable market) of AI CPUs could exceed $125bn by 2030, up from a mere <$10bn in 2025. In light of this, we have turned more constructive on AMD’s prospects.

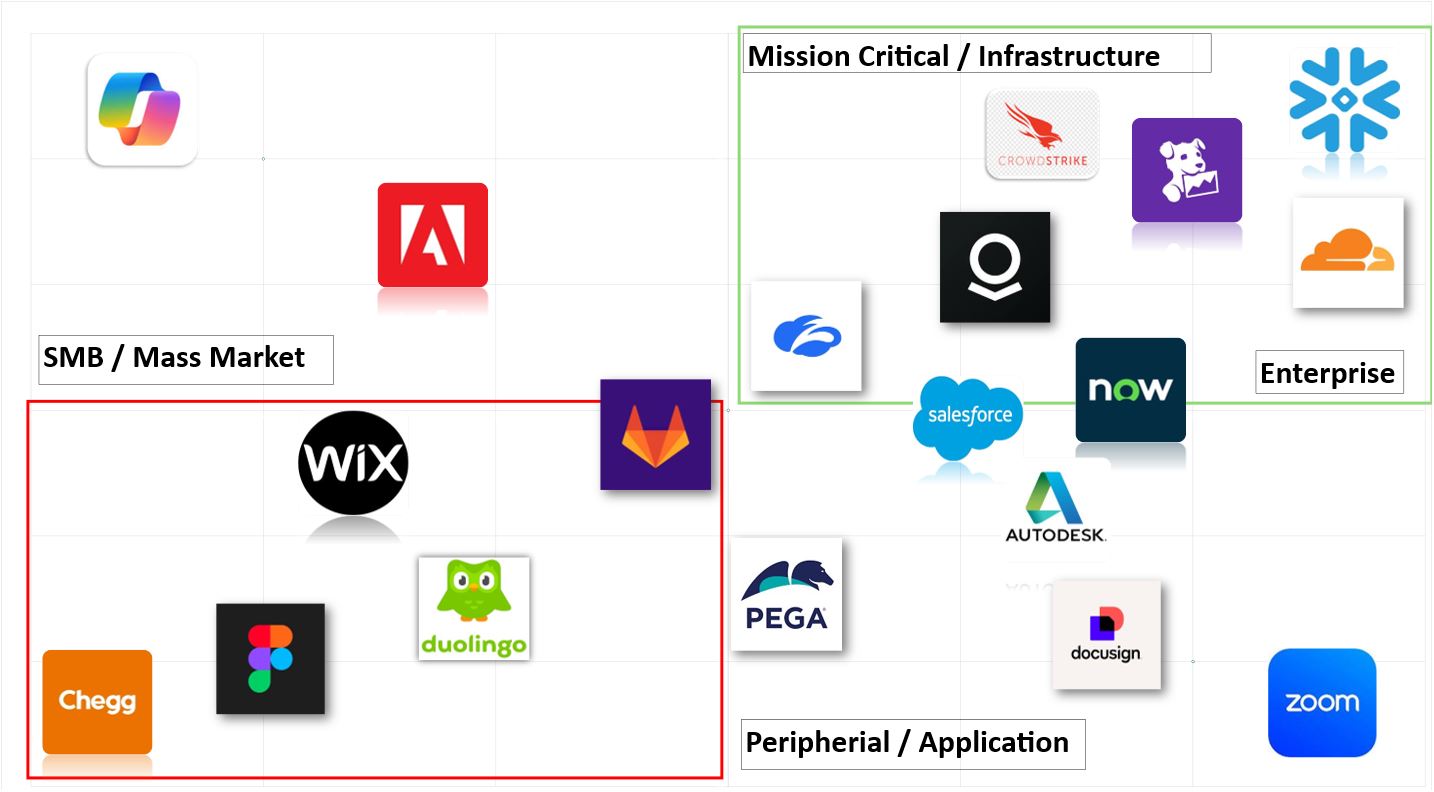

While we have written extensively about semiconductors in the recent quarters, the sharp rebound in our preferred software holdings also deserves attention. The bearish “SaaSpocalypse” narrative was initially ignited by concerns that AI would replace software seats and disrupt workflow automation, structurally weakening growth across the sector. While this threat remains valid for certain vulnerable incumbents, this quarter’s earnings demonstrated the “Jevons Paradox” – the idea that greater efficiency from technological advances will increase, rather than reduce, overall consumption – is indeed taking place. Instead of the expected slowdown and seat contraction, our software companies (Snowflake, Datadog, and MongoDB) showcased clear revenue reacceleration with Snowflake and Datadog’s revenues reaccelerating to the “30% growth” band.

Snowflake was one of the primary casualties of the initial SaaSpocalypse sentiment, weighed down by the market perception that new AI architectures might bypass traditional database management layers entirely. Nonetheless, the company successfully regained the growth momentum of its core business by integrating native Cortex AI capabilities, its suite of fully managed Large Language Models (LLMs) and machine learning tools, directly into the platform. Rather than cannibalizing usage, these AI-driven coding and analytics tools lowered the barrier to entry, spurring greater application development and ultimately driving higher overall data consumption within the Snowflake platform.

As investors, our job is not to predict every market rotation or macro noise, but to identify enduring trends and allocate capital to businesses that compound value over many years. The AI revolution is unlikely to be free of corrections or disappointments, yet the pace of innovation, enterprise adoption, and earnings growth suggests that we remain in the early innings of a much longer journey. By staying anchored to fundamentals rather than sentiment, we believe periods of volatility will continue to present opportunities rather than reasons for a capitulation.

Josh Le, CFA, MSc in FE

Senior Vice President

Portfolio Manager

joshle@covenant-capital.com

Risk Disclosure

Investors should consider this report as only a single factor in making their investment decision. Covenant Capital (“CC”) may not have taken any steps to ensure that the securities or financial instruments referred to in this report are suitable for any particular investor. CC will not treat recipients as its customers by their receiving the report. The investments or services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to your circumstances or otherwise constitutes a personal recommendation to you. The price, value of, and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is affected by changes in a spot or forward interest and exchange rates, economic indicators, the financial standing of any issuer or reference issuer, etc., that may have a positive or adverse effect on the income from or the price of such securities or financial instruments. By purchasing securities or financial instruments, you may incur above the principal as a result of fluctuations in market prices or other financial indices, etc. Investors in securities such as ADRs, the values of which are influenced by currency volatility, effectively assume this risk.

By entering this site you agree to be bound by the Terms and Conditions of Use. COVENANT CAPITAL PTE LTD (“CCPL”) is a Capital Markets License (AI/II) holder and regulated by the Monetary Authority of Singapore (‘MAS’).

By using this site you represent and warrant that you are an accredited investor or institutional investor as defined in the Singapore Securities and Futures Act (Chapter 289). In using this site users represent that they are an accredited and/or Institutional investor and use this site for their own information purposes only.

The information provided on this website by Covenant Capital Pte Ltd (CCPL) is intended solely for informational purposes and should not be construed as investment advice. It does not constitute legal, tax, or other professional advice. CCPL strongly recommends consulting qualified professionals for personalized guidance. The website does not offer or solicit securities transactions, and users are expected to comply with local laws. Accredited and institutional investors in Singapore may access the information solely for informational purposes.

What types of Personal Data do Covenant Capital collect?

Personal data is any information that relates to an identifiable individual, and we may collect this information when you interact with our staffs:

1. Personal Particulars (e.g. name, address, date of birth)

2. Tax, Insurance and employment details

3. Banking information and financial details

4. Details of interactions with us (eg. Images, voice recordings, personal opinions)

5. Information obtained from mobile devices with your consent

How do we collect your Personal Data?

Below are the ways that we collect your data:

1. Investment Management Agreement forms, Risk Profile forms, Subscription forms;

2. Via emails, SMSes, Whatsapps, phone calls or any other digital means to the office or its’ staffs;

3. Photos and videos of you from our events; and

4. Information about your use of our services and website, including cookies and IP address

How do we use your Personal Data?

1. For General Support

Verify your identity before providing our services, or responding to any of your queries, feed-back and complaints.

2. For our Internal Operations

a. Aid our analysis so that the company can improve our services and products.

b. Manage the company’s day-to-day business operations.

c. Ensure that the information that the company have on you is current and up to date.

d. Conducting Due Diligence checks to reduce Money Laundering and Terrorist

3. Financing Schemes

e. Comply with all laws and obligations from any legal authorities.

f. Seek professional advice, including legal.

g. Provide updates to you.

4. Posting on LinkedIn and Website

We may post personal data, including pictures and videos, on our LinkedIn page and website for purposes such as:

Who do we share your Personal Data with?

1. Any officer or employee of the company and its related companies;

2. Third parties (and their sub-contractors if applicable) that works with us, such as Custodian Bank of choice, Fund Administrators for the Funds that we manage, any third party Fund’s Administrators, IT support who back up our database and other service providers;

3. Relevant authorities such as government or regulatory authorities, statutory bodies, law enforcement agencies.

4. Relevant authorities such as government or regulatory authorities, statutory bodies, law enforcement agencies.

5. We require all personnel of the company and third party to ensure that any of your data disclosed to them is kept confidential and secure

6. We do not sell your Personal Data to any third party, and we shall comply fully with any duty and obligation of confidentiality that governs our relationship with you

When the company discloses your personal data to third-parties, the company will, to the best of its abilities, exercise reasonable due diligence that they are contractually bound to protect your personal data in accordance with applicable laws and regulations, save in cases where by your personal data is publicly available.

Accessing and Correction Request and Withdrawal of Consent

Please contact your advisor/banker or alternatively you can contact ccops@covenant-capital.com should you have the following queries.

1. Regarding the company’s data protection policies and processes

2. Request access to and/or make corrections to your personal data in the company’s possession; or

3. Wish to withdraw your consent to our collection, use or disclosure of your personal data.

The company endeavours to respond to you within 30 days of the submission.

Should you choose to withdraw your consent to any or all use of your personal data, the company might not be able to continue to provide any further services or maintain further relationships. Such withdrawal may also result in the termination of any agreement or relationship that you have with us.

Complaints

If you wish to make a complaint with regards to the handling and treatment of your personal data, please contact the company’s Data Protection Officer, mentioned below, directly. The DPO shall contact you within 5 working days to provide you with an estimated timeframe for the investigation and resolution of your complaint.

Should the outcome of the resolution is not satisfactory, you may refer to the Personal Data Protection Commission (PDPC) for any further resolutions.

If you have any doubt, please contact Mr Tay Kian Ngiap, the PDPA Data Protection Officer for Covenant Capital Pte. Ltd. He can be reached at kntay@covenant-capital.com

By accessing this website, you hereby agree to the terms listed on the website, all applicable laws and regulations, and agree that you are responsible for compliance with any applicable local laws. Any claim relating to Covenant Capital’s website shall be governed by the laws of the Republic of Singapore without regard to its conflict of law provisions.

1. License to Use

Permission is granted to download information and materials on Covenant Capital’s website for personal, non-commercial viewing only. This is the grant of a license, not a transfer of title, and under this license you may not:

i) modify or copy the information and materials;

ii) use the information and materials for any commercial purpose, or for any public display (commercial or non- commercial);

iii) attempt to decompile or reverse engineer any software contained on Covenant Capital’s web site;

iv) remove any copyright or other proprietary notations from the materials; or

v) transfer the materials to another person or “mirror” the materials on any other server.

All content, including but not limited to logo, tagline, graphics, images, text contents, buttons, icons, design and structure are property of Covenant Capital. All content on this website is protected by copyright, patent and trademark laws.

The Covenant Capital logo should not be used for any purpose whatsoever beyond what is available on the website, unless you have obtained written approval from us.

2. Disclaimer

The materials on Covenant Capital’s website are provided “as is”. Covenant Capital makes no warranties, expressed or implied, and hereby disclaims and negates all other warranties, including without limitation, implied warranties or conditions of merchantability, fitness for a particular purpose, or non-infringement of intellectual property or other violation of rights. Further, Covenant Capital does not warrant or make any representations concerning the accuracy, likely results, or reliability of the use of the materials on its Internet web site or otherwise relating to such materials or on any sites linked to this site.

It is your responsibility to evaluate the accuracy, completeness, or usefulness of any information, advice and other content available through this website.

You should not solely rely on the information, advice and other contents available on our website for decisions on investment(s) or decision with respect to our company’s products and services. You are advised to seek additional information required for you to make sound, well-informed and reasonable decision.

3. Limitations

In no event shall Covenant Capital or its suppliers be liable for any damages (including, without limitation, damages for loss of data or profit, or due to business interruption,) arising out of the use, inability to use or user’s reliance on the materials obtained through Covenant Capital’s web site, even if Covenant Capital or a Covenant Capital authorized representative has been notified orally or in writing of the possibility of such damage.

4. No Offer

Nothing in this website constitutes a solicitation, an offer, or a recommendation to buy or sell any investment instruments, to effect any transactions, or to conclude any legal act of any kind whatsoever. The information on this web site is subject to change (including, without limitation, modification, deletion or replacement thereof) without prior notice. When making decision on investments, you are advised to seek additional information required for you to make sound, well-informed and reasonable decision.

5. Revisions and Errata

The materials appearing on Covenant Capital’s website may include technical, typographical, or photographic errors. Covenant Capital does not warrant that any of the materials on its website are accurate, complete, or current. Covenant Capital may make changes to the materials contained on its website at any time without notice. Covenant Capital does not, however, make any commitment to update the materials.

6. Site Terms of Use Modifications

Covenant Capital may revise these terms of use for its web site at any time without notice. By using this website you are agreeing to be bound by the then current version of these Terms and Conditions of Use. If any of the term or change is deemed not acceptable to you, you should not continue to browse this site.

Your privacy is very important to us and we respect your online privacy. This Policy has been developed in order for you to understand how we collect, use, communicate and disclose and make use of personal information. We are committed to conducting our business in accordance with these principles in order to ensure that the confidentiality of personal information is protected and maintained.

1. Collection and Use of Information

We may collect personal identifiable information, such as names, postal addresses, email addresses, etc., when voluntarily submitted by visitors to our website. This information is only used to fulfill your specific request, unless further permission is provided to us to use it in any other manner or for any other purpose.

2. Web Cookies / Tracking Technology

A cookie is a small file which seeks permission to be placed on your computer’s hard drive. Once you are agreeable to the use of cookies, the file is added and the cookie helps analyse web traffic and tracks visits to a particular website. Cookies allow web applications to respond to you as an individual. The web application can tailor its operations to your needs, likes and dislikes by gathering and remembering information about your preferences.

We use traffic log cookies to identify which pages are being used. This helps us analyse data about website traffic and improve our website in order to tailor it to customer needs. We only use this information for statistical analysis purposes and then the data is removed from the system.

Overall, cookies help us provide you with a better website by enabling us to monitor which pages you find useful and which you do not. A cookie in no way gives us access to your computer or any information about you, other than the data you choose to share with us.

You can choose to accept or decline cookies. Most web browsers automatically accept cookies, but you can usually modify your browser setting to decline cookies if you prefer. This may prevent you from taking full advantage of the website.

3. Links to other websites

Our website may contain links to other websites of interest. However, once you have used these links to leave our site, you should note that we do not have any control over that other website. Therefore, we cannot be responsible for the protection and privacy of any information that you provide whilst visiting such sites, and this privacy statement does not govern such sites. You should exercise caution and review the privacy statement applicable to that particular website.

4. Distribution of Information

We will not sell, distribute or lease your personal information to third parties unless we have your permission or are required by law to do so. We may use your personal information to send you promotional information about third parties’ products or services, which we think you may find interesting if you tell us that you wish this to happen.

If you believe that any information we are holding on you is incorrect or incomplete, please write to or email us as soon as possible at the above address. We will promptly correct any information found to be incorrect.

When required by law, we may share information with governmental agencies or other companies assisting in the investigations. The information is not provided to these companies for marketing purposes.

5. Commitment to Data Security

To make sure your personal information is secured, we communicate our privacy and security guidelines to all Covenant Capital’s employees and strictly enforce privacy safeguards within the company.

Your personal identifiable information is kept secure. Only authorised employees, agents and contractors who have a direct need to access the information will be able to view this information.

We reserve the right to make changes to this policy. Any changes to this policy will be posted.