Edward Lim, CFA

In my early days as a portfolio manager, I met a highly ranked Asia strategist. He had a large institutional following partly because he was the only Asian in a bulge-bracket firm as a regional strategist and his analysis was often data-backed rather than eloquent rhetorics of most of his Caucasian peers. I can still remember one of his punch lines “The most important quality of a good strategist is to stick to your views; eventually you will be right.” Unfortunately, as the CIO of the firm, I do not have that luxury. Strategists do not run portfolios; they just write and speaks well in front of an audience. When you are managing risk like several of my colleagues do, it is imperative to mark to market developments and adjust your portfolios accordingly if there is a need to.

We entered the year, Bubblicious, with these bullish contours. First, we expect growth to remain resilient driven by accommodative fiscal policies, AI capex boom as well as fading effect of Liberation Day tariffs. We judge the recent weakness in the labour market as a low-hire, low-fire environment similar to what we have witnessed in the early 1990s when PC and enterprise adoption accelerated that entailed both job displacement and creation but was accompanied by higher productivity.

Second, on inflation, we acknowledged that inflation will not fall back to central bankers’ comfort level due to stubborn service inflation and nascent increase in goods inflation. However, it does not derail the view that most central banks will remain accommodative even as we disagree with market consensus then for further cuts by the Fed.

Third, while high valuation can put a constrain on the magnitude of upside returns in equities, we argued wide-spread earnings growth across regions and sectors and more importantly, positive earning revision momentum will underpin constructive return profiles across many asset classes favouring equities over bonds though.

But like any strategist, there must always be a hedge to the call, and we caution we are in a mature bull market now running into its fourth year. There have been several instances since 1945 when the market corrects more than -15% even in an absence of a recession. Such episodes are rarely born of fundamentals alone. They are often the inevitable consequence of complacency and hubris following extended rallies. We noted that 2026 could well prove to be such a year.

But this regime has changed all thanks to US and Israel waging a war against Iran. Not quite the regime change President Trump was hoping for, but the more deleterious change in macro-environment regime that moved away from the Recovery phase we have anchored at the start of the year where growth is rising, and inflation stabilises to several other less constructive paths. We marked to market these developments, and we believe we will move into a macro regime of decelerating, but non-recessionary growth coupled with higher inflation, but not back to Covid levels. We do not dismiss the worst-case scenario of stagflation and that would simply come from the failure to restore up to half of the flows from the Middle East by end of May.

As we have laid out in our flash Navigator published shortly after the war, Dire Straits – Money for Nothing, there is enough oil inventory to sustain 2-3 months of the global economy needs. But what we did not realise, the same cannot be said of refined products, which have little excess inventory in part because there was no incentive to stockpile them given the continuous fall in prices prior to the war.

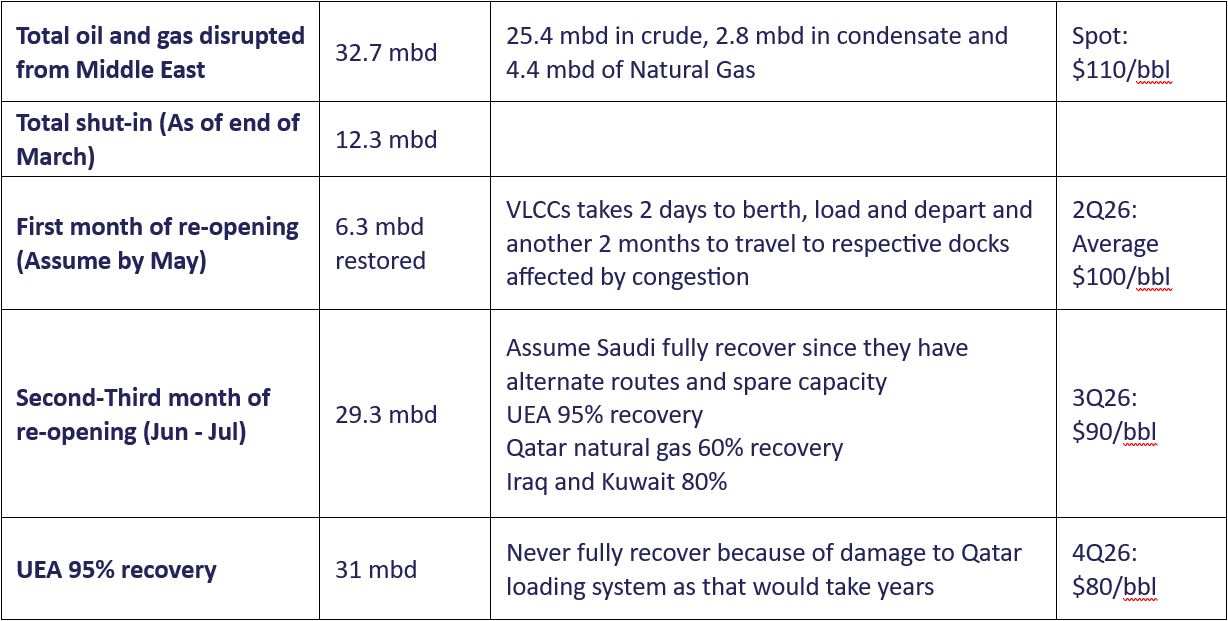

We refined our oil calculus. Before the war, the seven Gulf producers supplied 32.7mbd of molecules (25.4 mbd of crude, 2.8 mbd of condensate, 4.4 mbd of natural gas). As of writing, they have been forced to shut-in 12.3 mbd of production concentrated in 12.1 mbd of crude and condensate and 1.2mbd of natural gas. Assuming this is the peak of shut-in ie the war does not spill into a regional retaliation by the GCC, the total cuts in April would amount to 13 mbd. JP Morgan laid out the potential re-opening schedule in the table below. This underpins their oil price assumptions of $100bbl on average in 2Q26, $90/bbl in 3Q, and $80/bbl in 4Q. There are two other important takeaways from their analysis.

First, it will take at least 4 months for the world to refill their operating requirement after taking into consideration the commercial inventories available in the system. Poignantly, the last of oil tankers leaving the straits before the war reaches their port of destinations this week. Thereafter, draws on inventories and shut-ins will have to happen. Second, this means the up shot in downstream refined products prices will accelerate even further in the coming weeks. Moreover, the downstream refined products will take even longer to replenish and hence we should expect higher for longer prices for likes of diesel, jet fuel as well as petrochemical, plastic resin, and fertilizers (in which LNG is 60-70% of production cost). We are only at the beginning of cost-push inflation and demand destruction. Granted these are working assumptions and it could very well take longer and acknowledged there is non-linearity to the downside the longer the straits are constricted. But we need to work with something.

The feedback loop to higher oil prices obviously will be on growth and inflation dynamics. It is hard to be precise on their impact, but most economists have worked on the rule of thumb for every $10 increase in oil, global growth could be shaved off by 0.2 ppt and inflation increase by 0.2ppt. We started the year with consensus global GDP growth of 3.0%, 2.0% for the US, and 4.5% for China. The price of oil assumption was for $60/bbl for 2026, but oil has already averaged $78/bbl in 1Q26 and using the forecast above, oil will average $87/bbl for the full year. Global GDP growth could therefore be reduced by 0.54ppt to 2.45%, which is below trend potential but not recessionary. US and China will be downgraded by a lesser extent due to the former little dependence on Middle Eastern oil coupled with their recent OBBA tax cuts, while the latter derived nearly 30% of their energy needs from renewable sources and another 50% from coal.

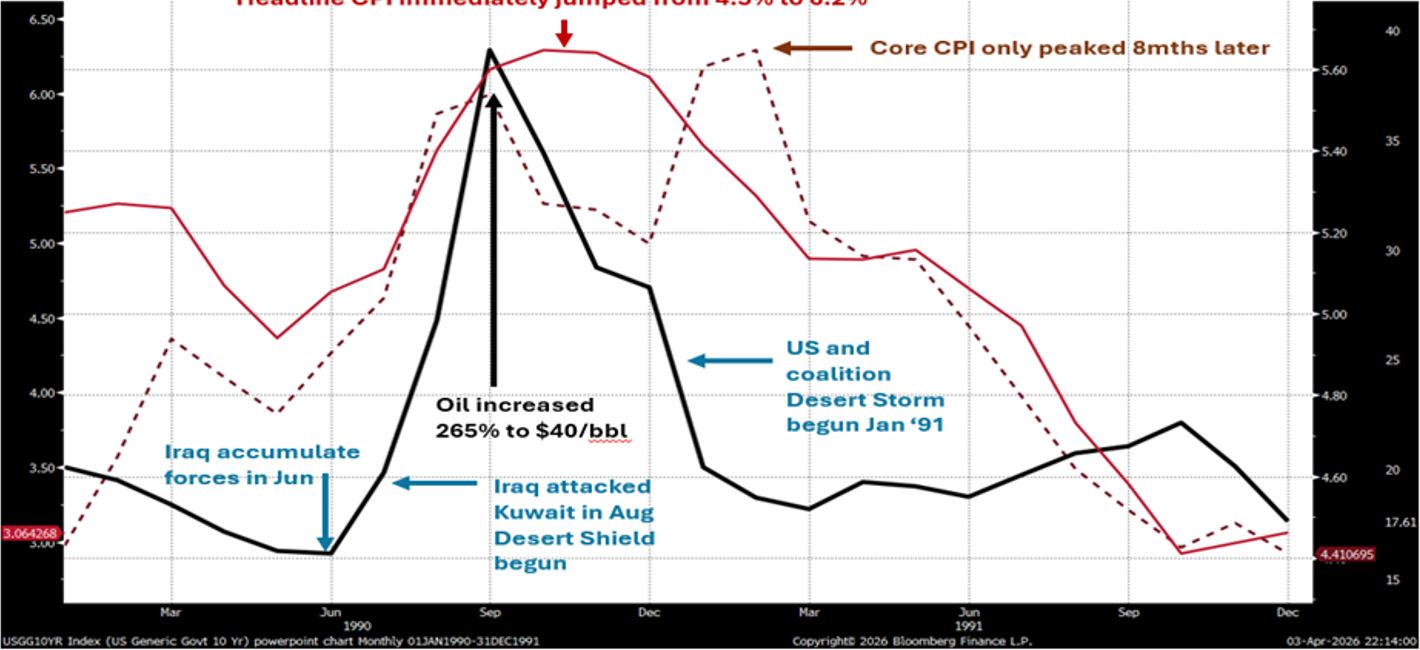

The inflation dynamics is more complex. We learned from the Ukraine-Russia war and the first Iraq war in 1990, the impact to headline inflation is almost immediate, while the inflation measure more relevant to monetary policy, core inflation, tends to be impacted with a lag of 2 to 3 months. None of these figures peaked until several months later after oil peaked. We believe the 1990 Iraq war is a better analogue to understand inflation and commiserating impact on yields and policy responses than the 2022 Ukraine-Russia invasion because inflation dynamic was complicated by post-Covid supply chain and labour shortage interruptions.

The 1990 Operation Desert Shield followed by Operation Desert Storm: Saddam Hussein started to accumulate his forces in June 1990 along the Kuwait borders. By August, Iraq invaded Kuwait and US with its coalition started their military build-up in Saudi Arabia to defend the kingdom. By Jan 1991, through the United Nations authorization, the US led a coalition of forces and embarked on Operation Desert Storm to drive the Iraqis out of Kuwait. The entire ground offensive took 1 month and 1 week to liberate Kuwait ending at the end of Feb 1991.

Starting from June 1990, oil price moved aggressively higher as the Iraqi military build-up escalated. Oil (Black line) moved from a low of $15/bbl and increased by 265% to a high of $40/bbl. It took 6 months later for oil to fall below $20/bbl. The impact to headline inflation (Solid Red line) was immediate spiking from the low of 4.3% in May 1990 to peak at 6.2% by November. Core inflation (Dotted brown line) only started to move more aggressively in July to surpass 5% and only peaked in February of 1991. We believe the current crisis impact on oil and inflation trajectories will be similar with the exception that oil from Middle East will now command a risk premium over its fundamentals because unlike previous oil shocks, Iran has now weaponized the Straits.

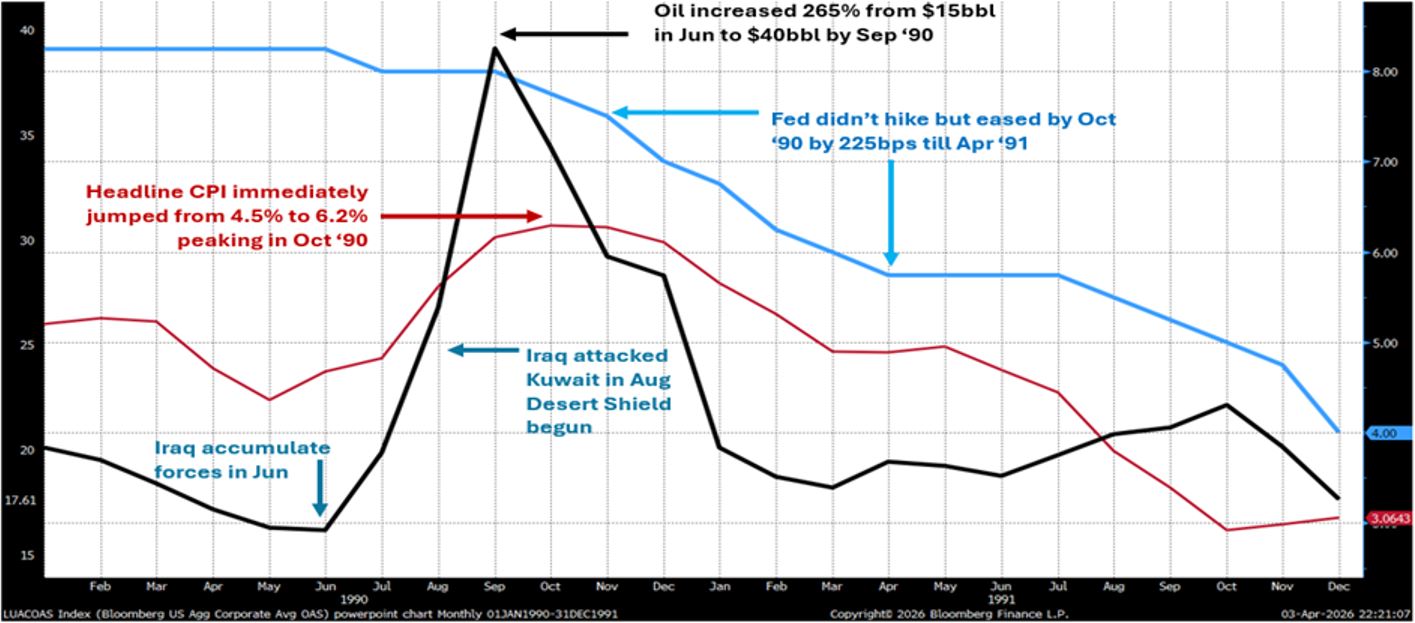

Prior to the Iraq-Kuwait conflict, the Fed was aggressively fighting inflation by tightening monetary conditions for much of 1986-1989 and only started to ease in late 1989 as the economy slumped bringing inflation down as well. It went into a wait-and-see pause mode in the first half of 1990 before the Iraq-Kuwait war upended the macro environment. Post invasion, the Fed did demonstrate restraint of not reversing its prior course of easing followed by a pause by hiking even as inflation spikes were immediate and inflation readings were all above its targets. Inflation prints did not peak until November for Headline CPI (Red line) and February for Core CPI. Instead, Fed re-assessed the balance of risk from the disruption in the oil market was tilted to growth downside and not inflationary pressure. By October 1990, it instituted a series of easing in monetary policies that did not stop till April of 1991 effectively lowering Fed Fund Effective rate (Blue line) from 8% to 5.75% (a 225bps easing).

Similarly, in this current episode, Fed easing cycle of 2024 came after a sharp hiking phase from 2022 to 2023. Prior to the US-Israel campaign against Iran, it has also paused and adopted a wait-and-see approach as it deliberates its dual mandate faced with sticky inflation versus a deteriorating labour market. We believe the Fed will also show restraint from hiking even as supply-induced inflation shocks materialised. Its toolbox is not designed to alleviate supply-shocks anyway. We also believe the next path of their policy action will mimic the 1990 episode. A 25 to 50 bps cuts is in the offing by early second half of this year. Noteworthy, we are again taking a contrarian view to the market on this issue which is pricing a hike.

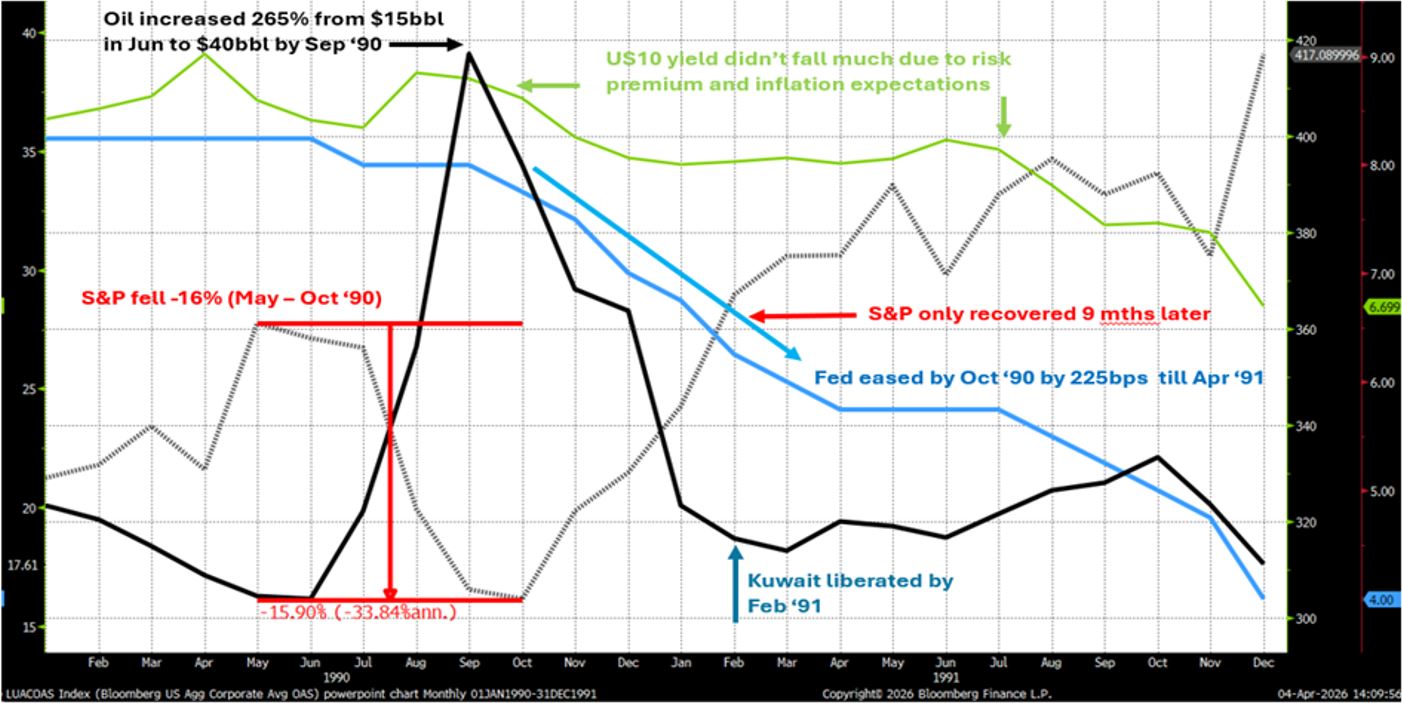

What about the equity and the bond yields in 1990? As the Fed started to ease its policy rate by October 1990, US10 yields (Green line) did not move in tandem to cuts in Fed Fund Effective rate (Blue line) and stayed elevated at 8 to 8.50% before moving marginally lower below 8% for much of 1991. This was simply due to a build-up of higher inflation expectations initially and increase in risk premia thereafter (Dear Treasury Secretary please remind your President what that means to your refinancing costs). On the other hand, US 2-year yields declined by 1.30% from Jul 1990 to February 1991 in the same period. The S&P (Grey line) fell -16% from the peak in May (a month prior to Iraqi forces build-up) and only trough when the Fed started easing in October. It took nine months to recover from its peak when Kuwait was finally liberated in the end of February of 1991. One important takeaway from this and including past oil crisis shocks is the equity market cares less who won the war but how the Fed and other central bankers react.

At Covenant Capital, we articulate our assumptions explicitly—even when they may ultimately prove imperfect. Investment without a framework is merely conjecture. We do not rely on conjectures. Our process is grounded in empirical data, historical precedents, and established economic theory as we attempt to interpret these evolving and difficult conditions. The question, then, is not what we think will happen, but what history and theories can reasonably teach us about what may come next.

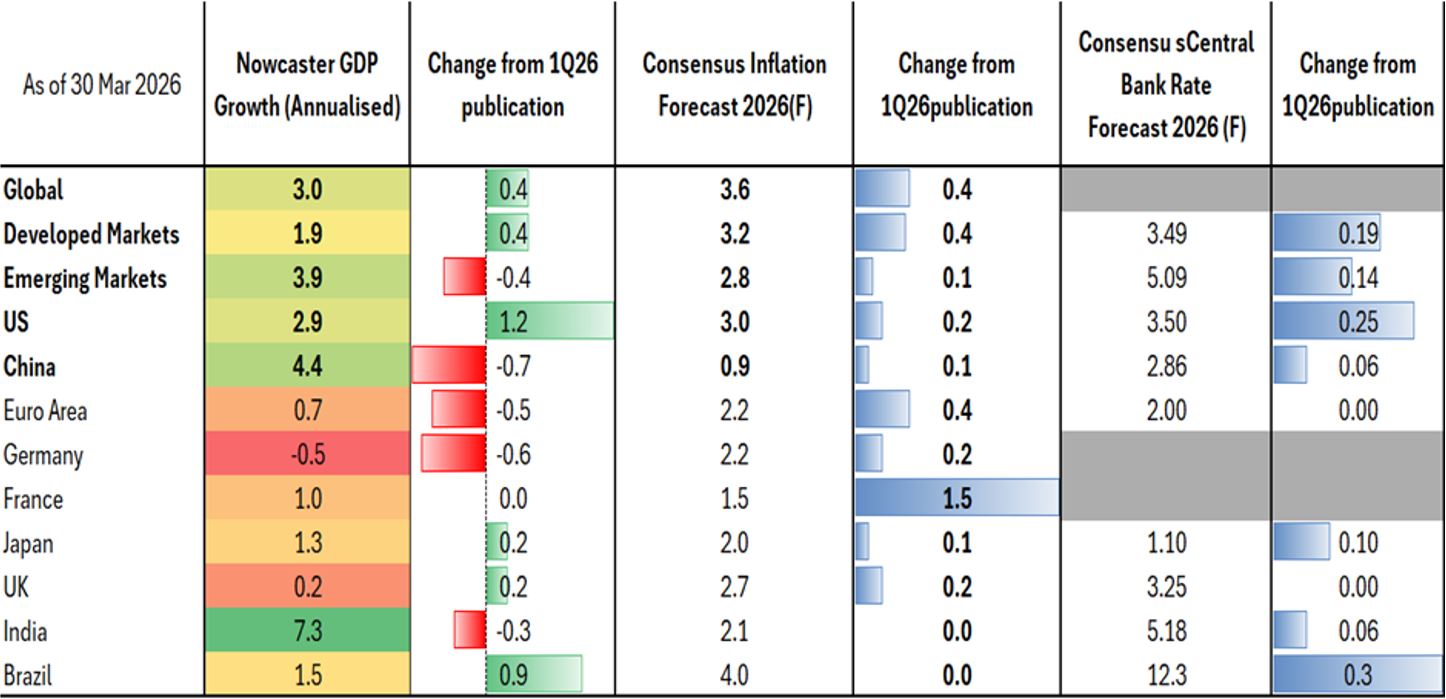

As laid out, we believe the macro regime moves from rising growth and stable inflation to two paths, with our base case as (1) Growth lower but at stable levels and higher inflation or worst case (2) Growth declining and inflation rising. Our investment clock framework corroborates this base case. The Nowcaster GDP tracker is already signalling a move down in activity in countries and regions most sensitive to oil with China, Germany, India and the broader Euro Zone and Emerging Markets from levels published in last quarter Navigator. Latest consensus forecast has moved inflation higher in every major country so has their forecast for central banks’ policy rates.

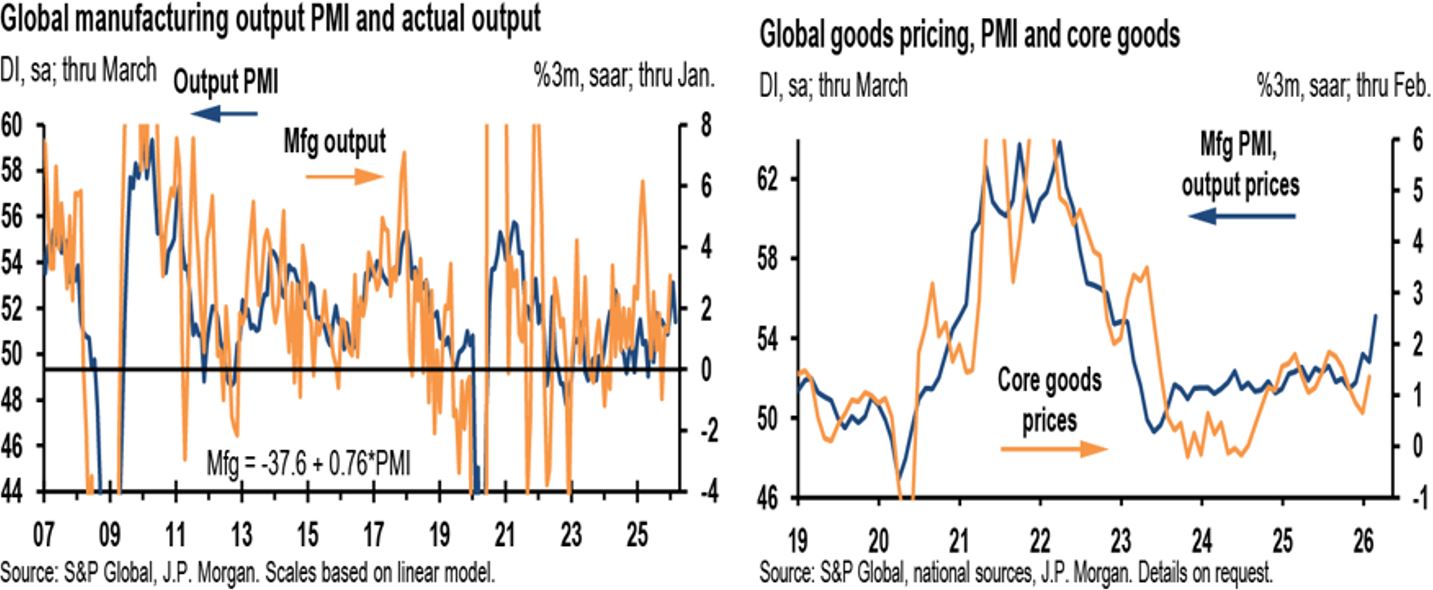

The latest Global Manufacturing PMI in March has reversed nearly all of its gain since December. The -1.7 pt fall puts the global economy growing at sub-par growth of 1.5% annualised. Under the hood, indicators such new orders, export orders and inventory accumulation are all pointing to a slowing economy. Moreover, survey respondents have also indicated outprices rising and can be seen across the globe.

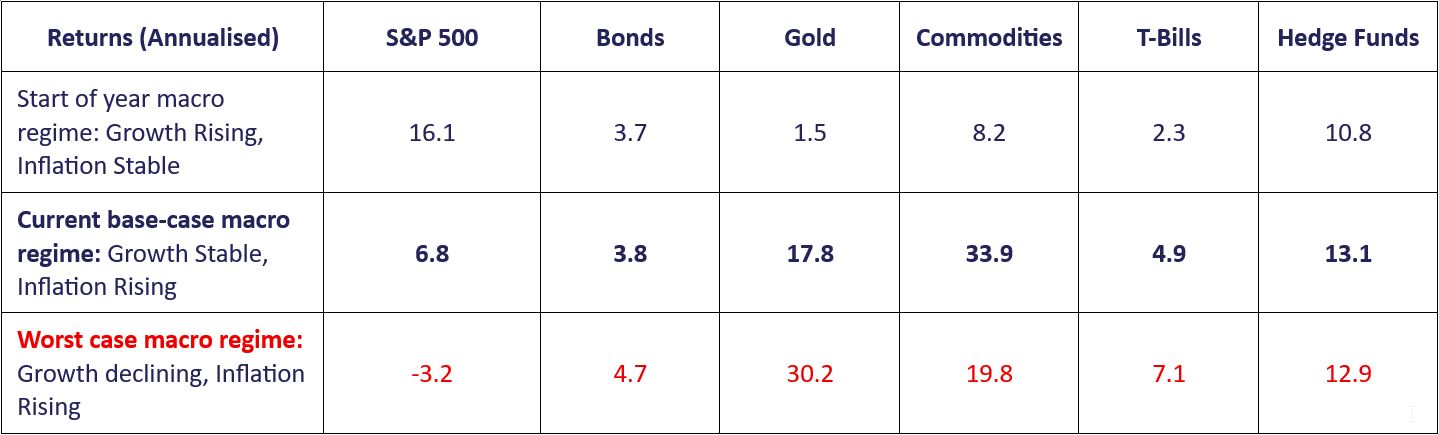

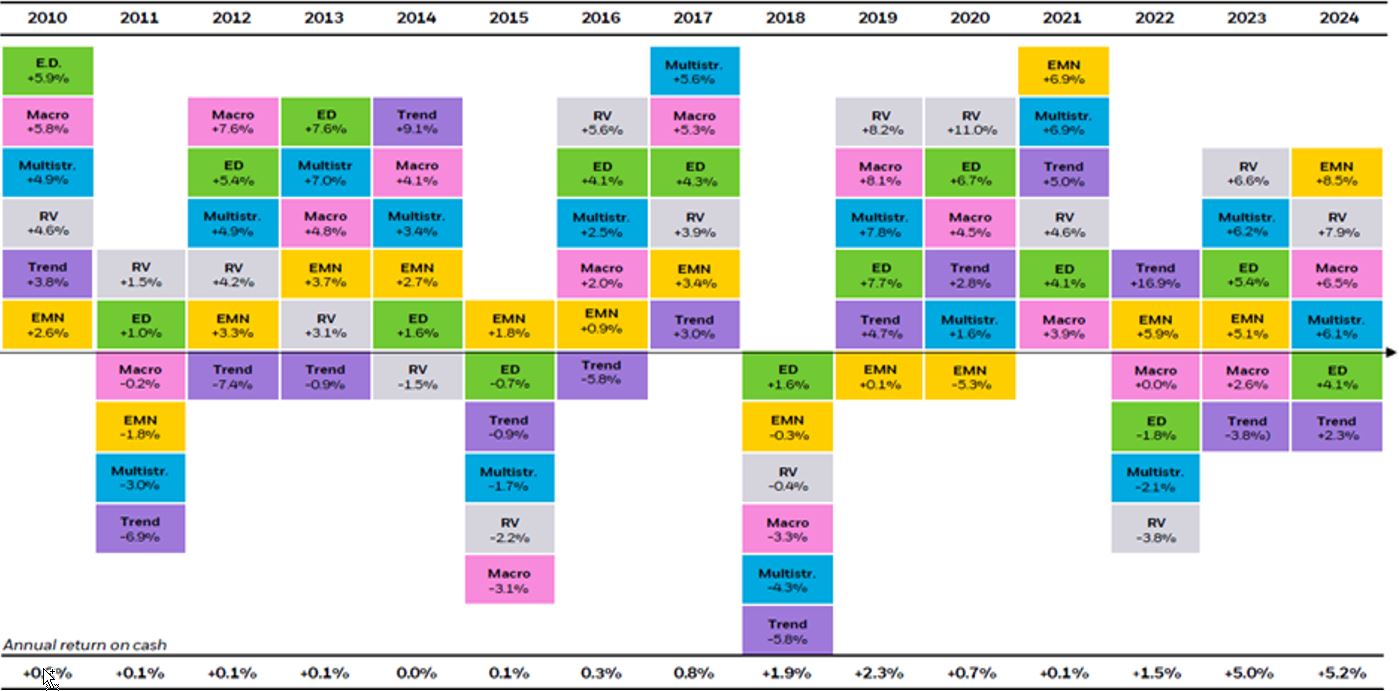

Based on NDR empirical studies from 1972 till 2025, as we move into a regime where growth forecast is downgraded but at stable level but with rising inflation, equities return falls materially from our start of the year regime of 16.1% pa to 6.8% pa. Equities do not significantly outperform Bonds (3.7% pa) and bonds do not significantly outperform cash (2.3%). Gold and Commodities performed the best. On a volatility-adjusted basis, hedge funds not only perform the best but as standalone asset class, in this regime they perform the second best across all other regimes.

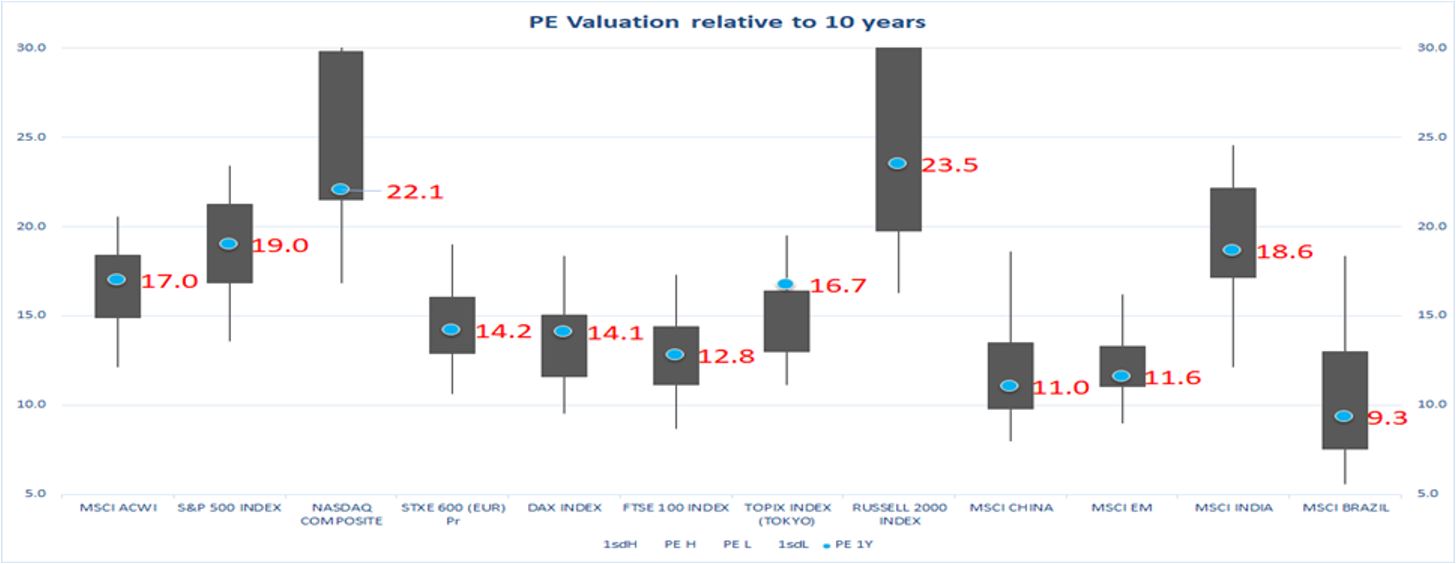

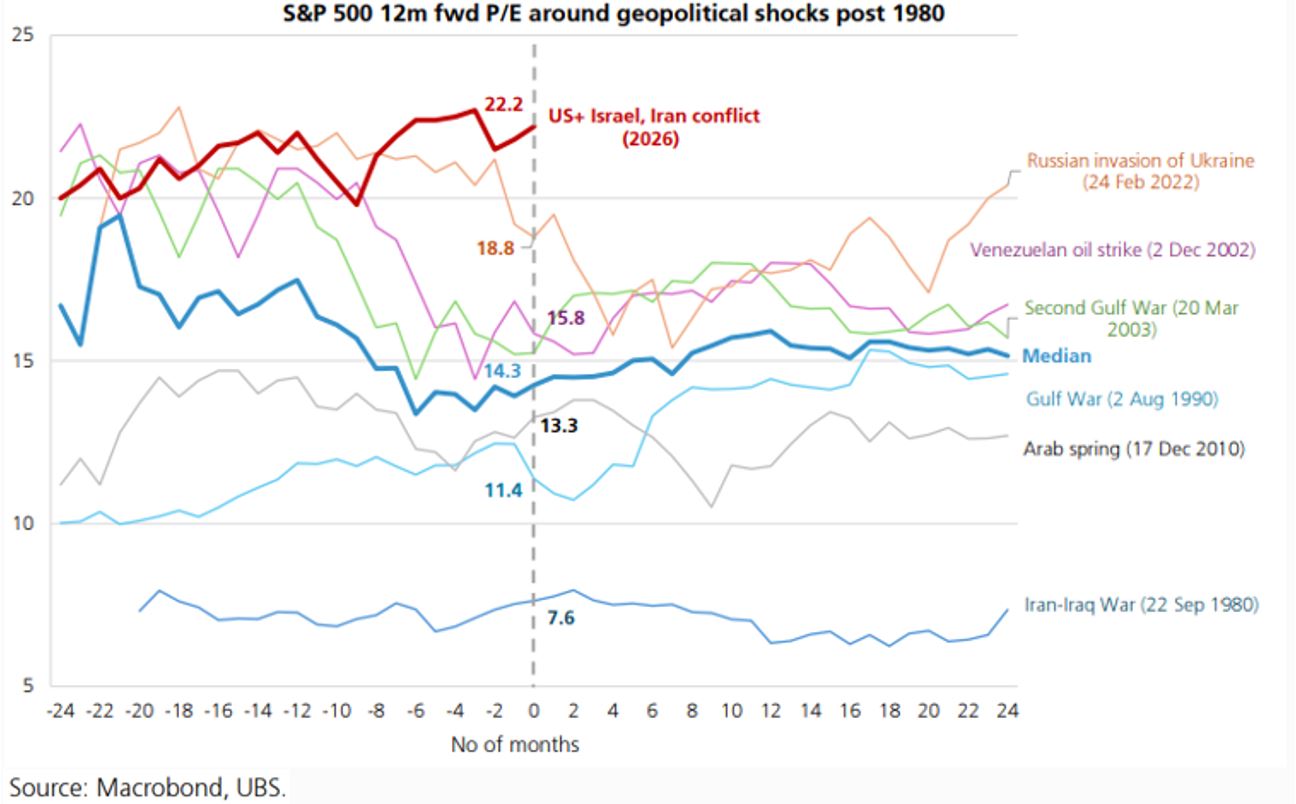

Equities Downgrade to Neutral: The downgrade in our macro views coupled with our views that the maximum impact of this current crisis has not fully run its course. GDP and earnings downgrades should ensue and inflation upgrades supports the downgrade of equities to Neutral. While we believe a relief rally can occur in the coming weeks because the market is oversold, we will be willing to reduce our equities further. Valuation has receded from its extreme expensive levels no doubt but an additional study from UBS Research shows that forward PE multiple typically corrects 6 ppt from the peak and bottoms at 14x forward PE in previous oil-shocks. The S&P is trading now at 18x having corrected from 22x. Amongst the key indices, NASDAQ looks attractive trading at close to its -1sd 10-year forward PE at 22x.

We are starting to see EPS revision momentum turned negative for every market with China EPS in negative revision zone, EM witnessing the biggest negative delta of change, and Europe and Japan likewise. Only the US is seeing upgrade driven narrowly by energy and tech sectors.

Fixed Income: Underweight. In the regime of lower but stable growth and rising inflation, the transmission mechanism to fixed income will be from an initial spike in the front end of the government bonds (2-year US Treasury has risen 47bps since the start of the war) more than the long-end of the curve (10-year +37bps) as investors price in inflationary risk and Fed hikes. But because recession is avoided, credit spreads should remain tight (investment-grade credit spread only rose 2bps, high-yield 20bps). We do not believe there will be wholesale selling of investment-grade credit space as carry is still quite attractive there. On the other hand, this spectre of rising commodities prices and the attendant move in Dollar have reduced the tailwind we were expecting at the start of the year of more easing in the emerging markets. We will be keeping our exposure in the short end of the investment grade credit but have trimmed some of our EM debt exposure. We do think chances have increased for a Fed cut in 2H26 and may move to extend duration in the later part of the year.

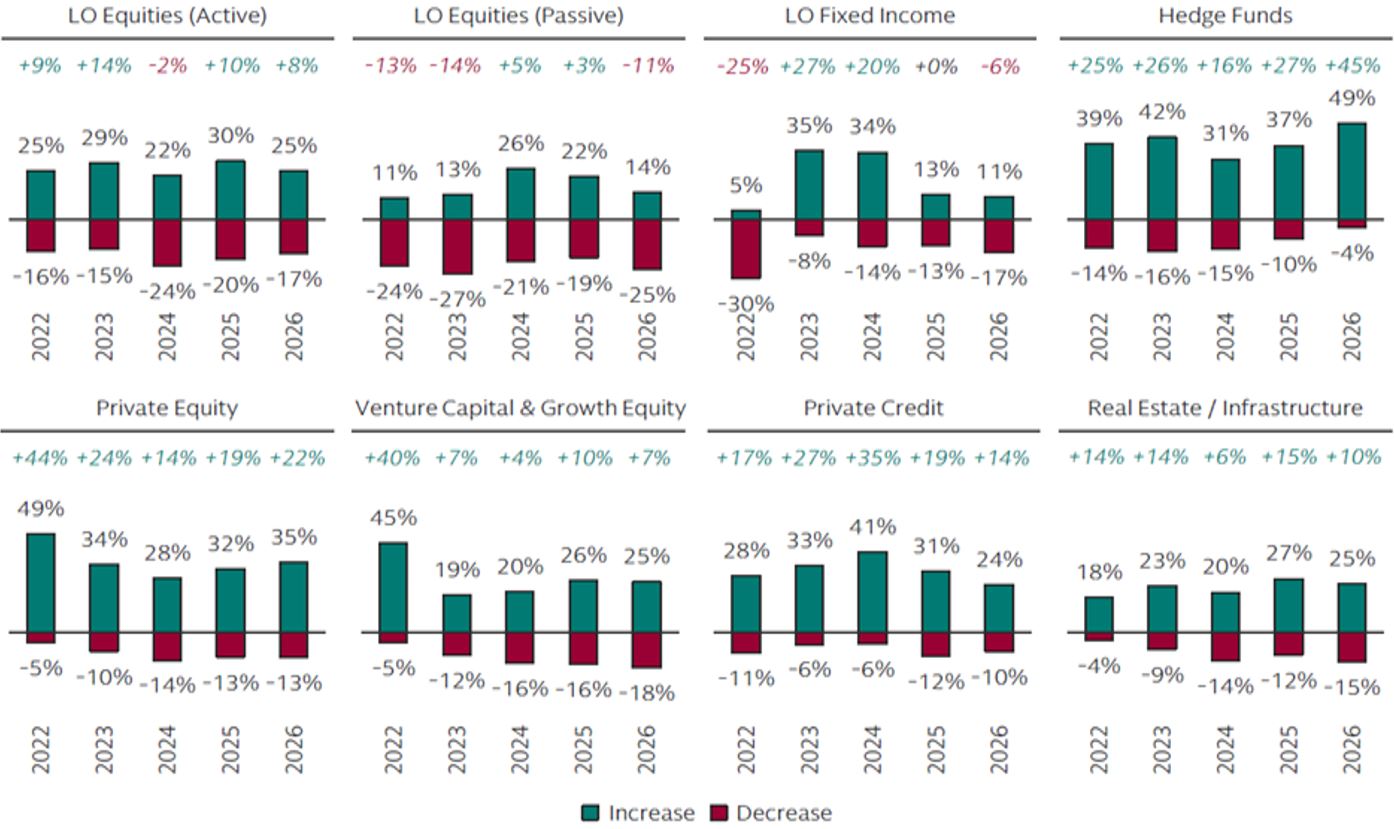

Alternatives: No change with 30% allocation to hedge funds. A recent survey by Goldman Sachs with responses from 317 global allocators accounting for $1 trillion in assets in hedge funds showed hedge funds is the asset class they will likely increase in 2026 more than public equities and bond as well as other alternatives. The key reasons they have cited are (1) better risk adjusted performances than a traditional 60/40 portfolio (2) acts as better diversifier than bonds to equities (3) more consistent returns than private equity, private credit and venture capital and (4) Hedge funds are semi-liquid while the dearth of distribution from private equity and venture capital, and the mismatch duration of private credit’s asset-liabilities are brewing concerns.

Our global, multi-manager and multi-strategy fund of hedge fund strategy is particularly suited to navigate this kind of macro regime. In fact, empirically, multi-strategy has consistently been the top few performers each year and has outperformed cash as well.

Commodities: No change with Gold range bound and keeping a small percentage of Bitcoin. We have cautioned that meteoric rise in Gold in last two quarters was driven largely by fast money and the stickier buyer in the form of central bankers’ purchases have abated. In fact, 2025 marks the lowest amount of gold central banks have purchased since 2022 and the first year, the Singapore government was net seller of gold. We were not surprised that gold has retraced sharply since it peaked in Dec at high $5,400 per ounce to a recent low of $4,200. We just witnessed the fastest ever reduction in gold futures contracted. Futures contracts outstanding for gold is still at elevated level compared to its longer-term history. In terms of flows in Gold ETF, we have seen $3bn of outflows year-to-date but accounting only for 1.8% of the ETF assets. We will be a bigger buyer of gold below $4,000 level. There are still too many specs in the system.

Cash: Keeping cash elevated until we can ascertain pass the fog of this war.

Featured Picture/Quote:

The other kind of kinder Terminator.

From Artemis II taken 4th April 2026.

Edward Lim, CFA

Chief Investment Officer

edwardlim@covenant-capital.com

Risk Disclosure

Investors should consider this report as only a single factor in making their investment decision. Covenant Capital (“CC”) may not have taken any steps to ensure that the securities or financial instruments referred to in this report are suitable for any particular investor. CC will not treat recipients as its customers by their receiving the report. The investments or services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to your circumstances or otherwise constitutes a personal recommendation to you. The price, value of, and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is affected by changes in a spot or forward interest and exchange rates, economic indicators, the financial standing of any issuer or reference issuer, etc., that may have a positive or adverse effect on the income from or the price of such securities or financial instruments. By purchasing securities or financial instruments, you may incur above the principal as a result of fluctuations in market prices or other financial indices, etc. Investors in securities such as ADRs, the values of which are influenced by currency volatility, effectively assume this risk.

By entering this site you agree to be bound by the Terms and Conditions of Use. COVENANT CAPITAL PTE LTD (“CCPL”) is a Capital Markets License (AI/II) holder and regulated by the Monetary Authority of Singapore (‘MAS’).

By using this site you represent and warrant that you are an accredited investor or institutional investor as defined in the Singapore Securities and Futures Act (Chapter 289). In using this site users represent that they are an accredited and/or Institutional investor and use this site for their own information purposes only.

The information provided on this website by Covenant Capital Pte Ltd (CCPL) is intended solely for informational purposes and should not be construed as investment advice. It does not constitute legal, tax, or other professional advice. CCPL strongly recommends consulting qualified professionals for personalized guidance. The website does not offer or solicit securities transactions, and users are expected to comply with local laws. Accredited and institutional investors in Singapore may access the information solely for informational purposes.

What types of Personal Data do Covenant Capital collect?

Personal data is any information that relates to an identifiable individual, and we may collect this information when you interact with our staffs:

1. Personal Particulars (e.g. name, address, date of birth)

2. Tax, Insurance and employment details

3. Banking information and financial details

4. Details of interactions with us (eg. Images, voice recordings, personal opinions)

5. Information obtained from mobile devices with your consent

How do we collect your Personal Data?

Below are the ways that we collect your data:

1. Investment Management Agreement forms, Risk Profile forms, Subscription forms;

2. Via emails, SMSes, Whatsapps, phone calls or any other digital means to the office or its’ staffs;

3. Photos and videos of you from our events; and

4. Information about your use of our services and website, including cookies and IP address

How do we use your Personal Data?

1. For General Support

Verify your identity before providing our services, or responding to any of your queries, feed-back and complaints.

2. For our Internal Operations

a. Aid our analysis so that the company can improve our services and products.

b. Manage the company’s day-to-day business operations.

c. Ensure that the information that the company have on you is current and up to date.

d. Conducting Due Diligence checks to reduce Money Laundering and Terrorist

3. Financing Schemes

e. Comply with all laws and obligations from any legal authorities.

f. Seek professional advice, including legal.

g. Provide updates to you.

4. Posting on LinkedIn and Website

We may post personal data, including pictures and videos, on our LinkedIn page and website for purposes such as:

Who do we share your Personal Data with?

1. Any officer or employee of the company and its related companies;

2. Third parties (and their sub-contractors if applicable) that works with us, such as Custodian Bank of choice, Fund Administrators for the Funds that we manage, any third party Fund’s Administrators, IT support who back up our database and other service providers;

3. Relevant authorities such as government or regulatory authorities, statutory bodies, law enforcement agencies.

4. Relevant authorities such as government or regulatory authorities, statutory bodies, law enforcement agencies.

5. We require all personnel of the company and third party to ensure that any of your data disclosed to them is kept confidential and secure

6. We do not sell your Personal Data to any third party, and we shall comply fully with any duty and obligation of confidentiality that governs our relationship with you

When the company discloses your personal data to third-parties, the company will, to the best of its abilities, exercise reasonable due diligence that they are contractually bound to protect your personal data in accordance with applicable laws and regulations, save in cases where by your personal data is publicly available.

Accessing and Correction Request and Withdrawal of Consent

Please contact your advisor/banker or alternatively you can contact ccops@covenant-capital.com should you have the following queries.

1. Regarding the company’s data protection policies and processes

2. Request access to and/or make corrections to your personal data in the company’s possession; or

3. Wish to withdraw your consent to our collection, use or disclosure of your personal data.

The company endeavours to respond to you within 30 days of the submission.

Should you choose to withdraw your consent to any or all use of your personal data, the company might not be able to continue to provide any further services or maintain further relationships. Such withdrawal may also result in the termination of any agreement or relationship that you have with us.

Complaints

If you wish to make a complaint with regards to the handling and treatment of your personal data, please contact the company’s Data Protection Officer, mentioned below, directly. The DPO shall contact you within 5 working days to provide you with an estimated timeframe for the investigation and resolution of your complaint.

Should the outcome of the resolution is not satisfactory, you may refer to the Personal Data Protection Commission (PDPC) for any further resolutions.

If you have any doubt, please contact Mr Tay Kian Ngiap, the PDPA Data Protection Officer for Covenant Capital Pte. Ltd. He can be reached at kntay@covenant-capital.com

By accessing this website, you hereby agree to the terms listed on the website, all applicable laws and regulations, and agree that you are responsible for compliance with any applicable local laws. Any claim relating to Covenant Capital’s website shall be governed by the laws of the Republic of Singapore without regard to its conflict of law provisions.

1. License to Use

Permission is granted to download information and materials on Covenant Capital’s website for personal, non-commercial viewing only. This is the grant of a license, not a transfer of title, and under this license you may not:

i) modify or copy the information and materials;

ii) use the information and materials for any commercial purpose, or for any public display (commercial or non- commercial);

iii) attempt to decompile or reverse engineer any software contained on Covenant Capital’s web site;

iv) remove any copyright or other proprietary notations from the materials; or

v) transfer the materials to another person or “mirror” the materials on any other server.

All content, including but not limited to logo, tagline, graphics, images, text contents, buttons, icons, design and structure are property of Covenant Capital. All content on this website is protected by copyright, patent and trademark laws.

The Covenant Capital logo should not be used for any purpose whatsoever beyond what is available on the website, unless you have obtained written approval from us.

2. Disclaimer

The materials on Covenant Capital’s website are provided “as is”. Covenant Capital makes no warranties, expressed or implied, and hereby disclaims and negates all other warranties, including without limitation, implied warranties or conditions of merchantability, fitness for a particular purpose, or non-infringement of intellectual property or other violation of rights. Further, Covenant Capital does not warrant or make any representations concerning the accuracy, likely results, or reliability of the use of the materials on its Internet web site or otherwise relating to such materials or on any sites linked to this site.

It is your responsibility to evaluate the accuracy, completeness, or usefulness of any information, advice and other content available through this website.

You should not solely rely on the information, advice and other contents available on our website for decisions on investment(s) or decision with respect to our company’s products and services. You are advised to seek additional information required for you to make sound, well-informed and reasonable decision.

3. Limitations

In no event shall Covenant Capital or its suppliers be liable for any damages (including, without limitation, damages for loss of data or profit, or due to business interruption,) arising out of the use, inability to use or user’s reliance on the materials obtained through Covenant Capital’s web site, even if Covenant Capital or a Covenant Capital authorized representative has been notified orally or in writing of the possibility of such damage.

4. No Offer

Nothing in this website constitutes a solicitation, an offer, or a recommendation to buy or sell any investment instruments, to effect any transactions, or to conclude any legal act of any kind whatsoever. The information on this web site is subject to change (including, without limitation, modification, deletion or replacement thereof) without prior notice. When making decision on investments, you are advised to seek additional information required for you to make sound, well-informed and reasonable decision.

5. Revisions and Errata

The materials appearing on Covenant Capital’s website may include technical, typographical, or photographic errors. Covenant Capital does not warrant that any of the materials on its website are accurate, complete, or current. Covenant Capital may make changes to the materials contained on its website at any time without notice. Covenant Capital does not, however, make any commitment to update the materials.

6. Site Terms of Use Modifications

Covenant Capital may revise these terms of use for its web site at any time without notice. By using this website you are agreeing to be bound by the then current version of these Terms and Conditions of Use. If any of the term or change is deemed not acceptable to you, you should not continue to browse this site.

Your privacy is very important to us and we respect your online privacy. This Policy has been developed in order for you to understand how we collect, use, communicate and disclose and make use of personal information. We are committed to conducting our business in accordance with these principles in order to ensure that the confidentiality of personal information is protected and maintained.

1. Collection and Use of Information

We may collect personal identifiable information, such as names, postal addresses, email addresses, etc., when voluntarily submitted by visitors to our website. This information is only used to fulfill your specific request, unless further permission is provided to us to use it in any other manner or for any other purpose.

2. Web Cookies / Tracking Technology

A cookie is a small file which seeks permission to be placed on your computer’s hard drive. Once you are agreeable to the use of cookies, the file is added and the cookie helps analyse web traffic and tracks visits to a particular website. Cookies allow web applications to respond to you as an individual. The web application can tailor its operations to your needs, likes and dislikes by gathering and remembering information about your preferences.

We use traffic log cookies to identify which pages are being used. This helps us analyse data about website traffic and improve our website in order to tailor it to customer needs. We only use this information for statistical analysis purposes and then the data is removed from the system.

Overall, cookies help us provide you with a better website by enabling us to monitor which pages you find useful and which you do not. A cookie in no way gives us access to your computer or any information about you, other than the data you choose to share with us.

You can choose to accept or decline cookies. Most web browsers automatically accept cookies, but you can usually modify your browser setting to decline cookies if you prefer. This may prevent you from taking full advantage of the website.

3. Links to other websites

Our website may contain links to other websites of interest. However, once you have used these links to leave our site, you should note that we do not have any control over that other website. Therefore, we cannot be responsible for the protection and privacy of any information that you provide whilst visiting such sites, and this privacy statement does not govern such sites. You should exercise caution and review the privacy statement applicable to that particular website.

4. Distribution of Information

We will not sell, distribute or lease your personal information to third parties unless we have your permission or are required by law to do so. We may use your personal information to send you promotional information about third parties’ products or services, which we think you may find interesting if you tell us that you wish this to happen.

If you believe that any information we are holding on you is incorrect or incomplete, please write to or email us as soon as possible at the above address. We will promptly correct any information found to be incorrect.

When required by law, we may share information with governmental agencies or other companies assisting in the investigations. The information is not provided to these companies for marketing purposes.

5. Commitment to Data Security

To make sure your personal information is secured, we communicate our privacy and security guidelines to all Covenant Capital’s employees and strictly enforce privacy safeguards within the company.

Your personal identifiable information is kept secure. Only authorised employees, agents and contractors who have a direct need to access the information will be able to view this information.

We reserve the right to make changes to this policy. Any changes to this policy will be posted.