However, looking at 122 years of data, we observe that such positive correlations with negative outcomes for both bonds and equities like what we have seen in 2022 are quite rare and even rarer to repeat in the next consecutive year.

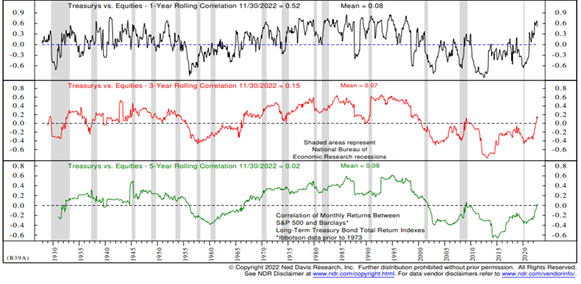

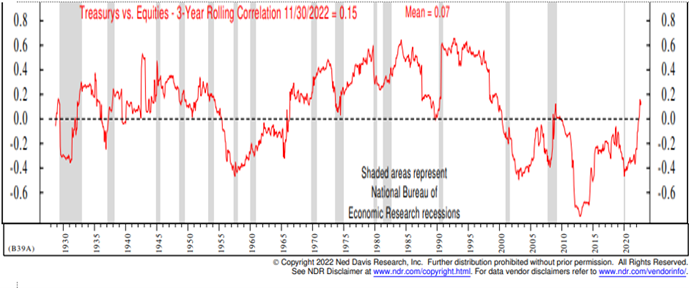

Aside from the above empirical evidence that refutes the notion equity and bond correlate often with negative returns, we took another step further to understand why and when the correlation is positive or negative. We look at their correlation relationship from 1930 onwards and we overlayed the macro-dynamics corresponding to those periods. Several important takeaways from this study.

Equity/Bond correlations are +ve in short-term, but longer term remains -ve providing diversification benefits

Four distinct periods of correlation changes since 1930

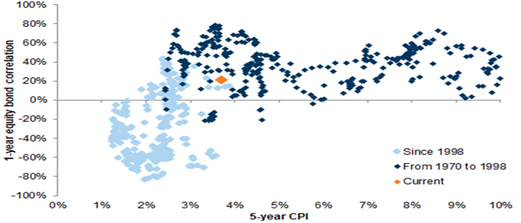

The level of inflation determines the correlation between bonds and equities (Source: Goldman Sachs)

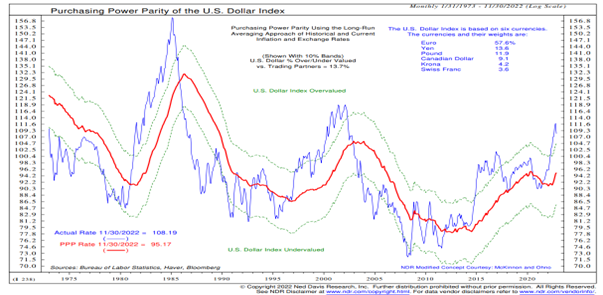

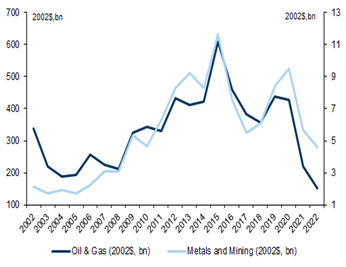

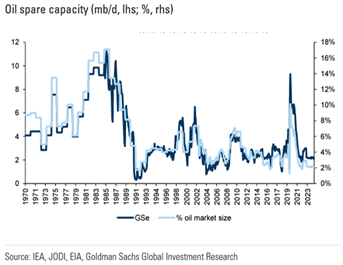

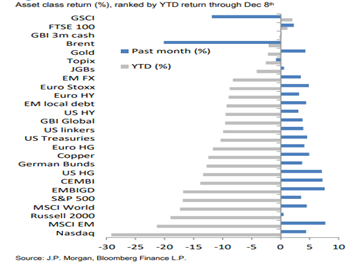

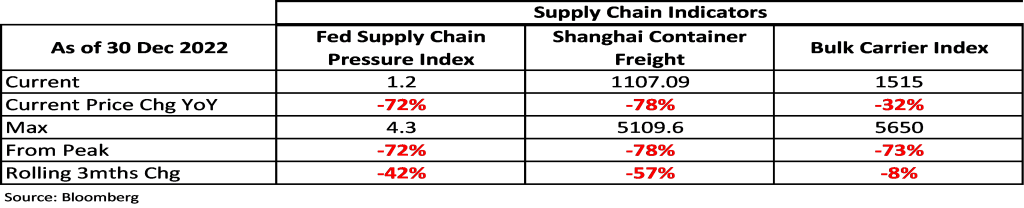

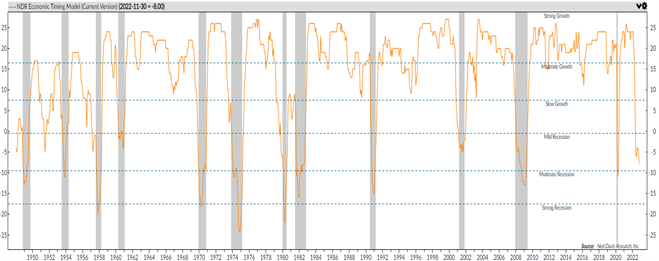

What kind of recession matters? If we enter a mild and even a moderate recession, much of the retrenchments for many asset classes are already done in 2022. However, if it morphs into a severe recession, there are still material drawdowns in nearly all equities indices. The high yield and emerging markets debts appear expensive and vulnerable to default risk, while there is moderate downside risk as credit spreads should widen further for investment-grade debt. Only Developed Markets Treasuries are cheap. Recent dollar weakness should also reverse, Gold might just have its occasional day in the sun, and oil should have further downside as demand weakens further.

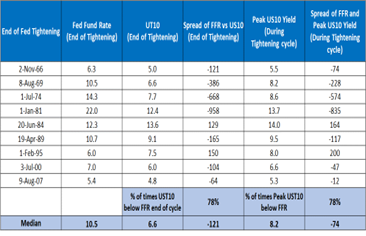

Fixed Income (Overweight in US Treasuries): Regardless of the shape of recession, Treasuries in several developed markets are preferred. Our analysis points to a peak of positive correlation between bonds and equities and suggests in the near term it will turn negative. This will revert government bonds to its role of a low-risk carry asset (3.5 to 4.0% yield) and as a portfolio diversifier. Our analysis, The Bear Necessities provides a few important conclusions and markers:

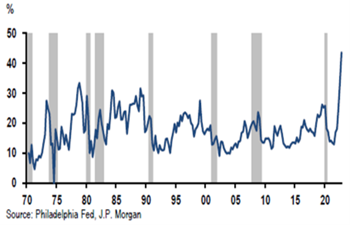

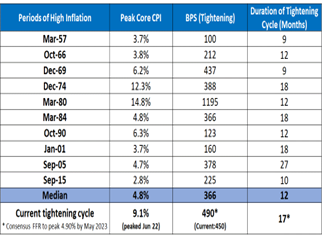

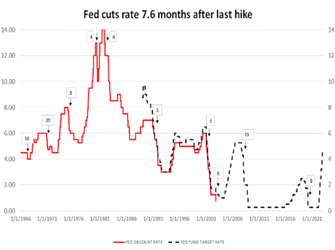

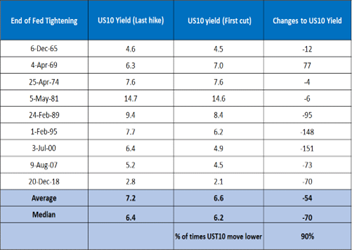

History says US10 yield peak ahead and lower than terminal Fed Fund Rate

Source: Bloomberg, Fed, NDR

Besides Treasuries, we are overweight investment grade debt as yield is attractive relative to the risk. At 5.80% yield on BBB US Corporates, this is the highest level of yield since 2008 and 140bps higher than the peak of covid 2020. On a yield per duration risk taken, it is at the most attractive level since 2008. We are mindful in our credit selection preferring to buy high quality bonds and will lean on our collaboration with Principal Asset Management in credit assessment. Timing is also important as we prefer to increase our exposures when credit spread is at recessionary level. We continue to avoid high yield debt, leveraged loans, and most of emerging market debts. We are most concerned about private credit as we believe investors have not done sufficient due diligence and been lax in demanding stronger covenants.

Equities: We have been underweight Equities since October 2021, but we think the conditions to alter this view may presents itself by February-April. Some of the conditions we are looking are as follows:

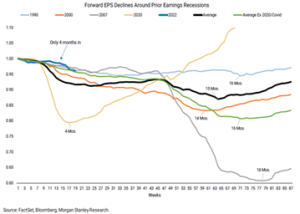

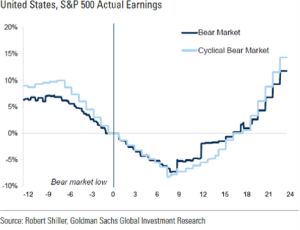

Earnings forecast needs to fall further but market bottoms 6-9 months ahead of earnings bottom