Edward Lim, CFA

In the 1980s, the image of English football was characterised by one word, hooliganism. The nadir of English football came in 1985 when English football fans (sadly it was my team) attacked Juventus fans in Heysel Stadium, Belgium, which led to a tragic human crush that killed 39 people and injured over 600 spectators. All English clubs were subsequently banned for 6 years from competing in all European club competitions.

The 1990 World Cup was the first time the English fans travelled to Europe and into Italy, and the situation was a powder keg. The English team arrived in Italy carrying the heavy baggage of a tarnished reputation. Yet, against all odds, that summer became a turning point where the team completely rehabilitated its image, capturing the world’s imagination and kicking off a brand-new, modernized era for what a combination of football and capitalism could do. And they even advanced to the semi-finals only to be knocked out by West Germany during a dramatic penalty shootout. They did it by changing the narrative entirely and it was best captured in their theme song “World in Motion” by New Order. Instead of relying on aggressive and old-school football tactics, the song and the team embraced a fresh, creative energy that proved you can successfully reinvent both style of play and image.

Today, global markets are navigating their own ungainly transition: strained political alliances, fractured trade relationships, and a technological revolution that is as exhilarating as it is destabilising. The lesson from Italia ’90 is not merely that reputations can be rehabilitated. It is that when the old playbook no longer works, survival depends on adaptation rather than the retention of outdated strategies. In this quarter’s Navigator, we explore what this multitude of changes means for future investment opportunities.

We are witnessing the global order being rewritten in real time. The old order of a unipolar and multi-lateral world underwritten by US financial, technological, ideological, and security largess is no longer the organizing principle. Instead, we are now moving towards a multi-polar world, each jostling for their relevance on the world stage while wrestling with increasingly febrile domestic undercurrents. The advent of generative AI in the last few years is expected to bring about exciting new opportunities as well as profound changes in many existing business models and potentially a re-writing of social contracts. If not managed properly, AI will further exacerbate the schism between the haves and have-nots.

As we have mused in 2020 Navigator – The Four Horsemen of the Apocalypse how the Covid pandemic has exposed the fallacies of an inter-dependent and cooperative world of supply chain, the once-unthinkable closure of the Strait of Hormuz by Iran has now extended those fault lines from medical and food supplies to energy. The need to onshore key capabilities especially in critical resources, key industries, and securing one’s sovereign AI, has become sine qua non to not only one’s survival but also to its dominance. We have identified a few tenets of a multi-polar world and navigate through their investment implications.

1) Energy security implications: Regardless of whatever resolutions the US, Iran, and rest of GCC can eke out in the end, this episode has redrawn the terms of trades of oil security for every country, especially in Asia.

A)

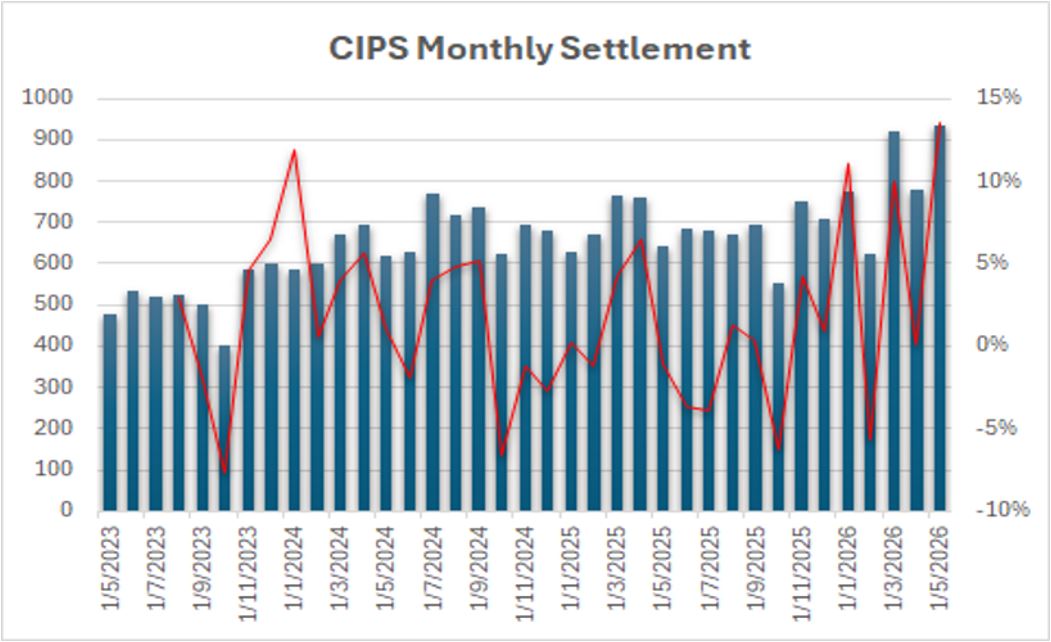

During this crisis, we saw a tectonic shift of trading oil outside of the USD. As evidenced in China’s Cross-Border Interbank System [CIPS], China’s rival platform to SWIFT, the de facto global cross-border payment system, saw a significant jump in transactions. The value of transactions from Mar-May has jumped 25% since the start of the war when compared to the previous three months. While RMB 2.6trn transaction value still represents a small percentage of global flows, if you include other currencies like Rupees, Dirhams and Euro, the war has accelerated the use of non-USD in settlement of critical resources – a trend precipitated when the US unilaterally shut Russia out of the international payment system back in 2022.

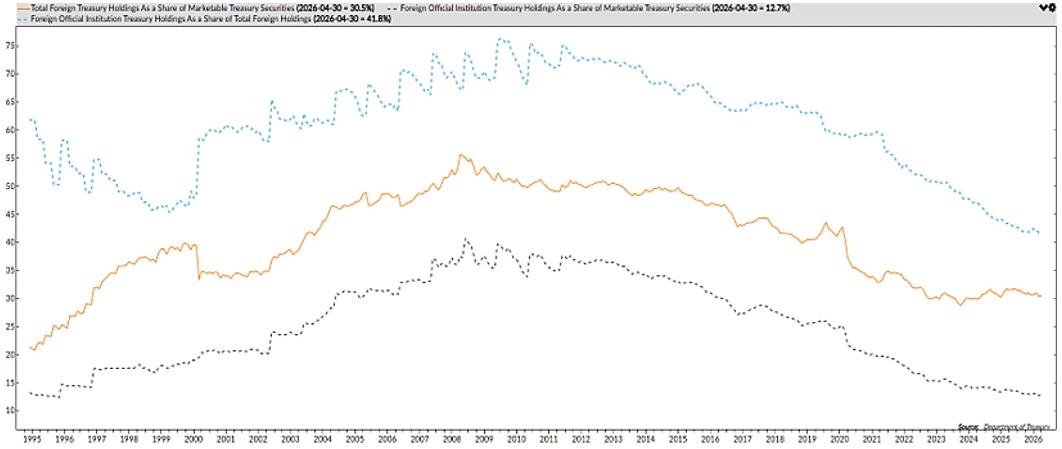

If you overlay that with the continuation of the sale of US Treasury holdings by foreign official entities, the erosion of the USD’s exorbitant privilege is already in motion. Based on IMF data, USD share of global foreign reserves has fallen from more than 70% in 2000 to less than 60% and in its place, RMB has risen from less than 1% to almost 10%. While the USD is now inexpensive relative to other majors on a Purchasing Power Parity basis when compared to the start of 2025 (it is 3 to 5% cheaper than the GBP and Euro), we note since the de-pegging of the USD from Gold in 1971, there has been times the USD has traded more than 10% lower than the implied fundamental value. Expect the USD to weaken further and domestic buyers better step in, otherwise US yields will have to rise.

B)

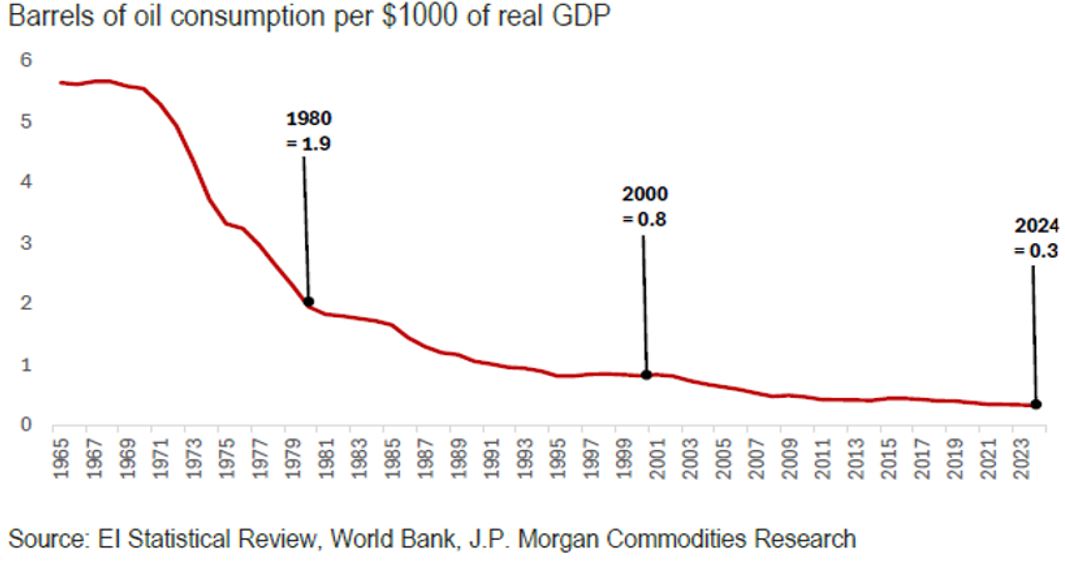

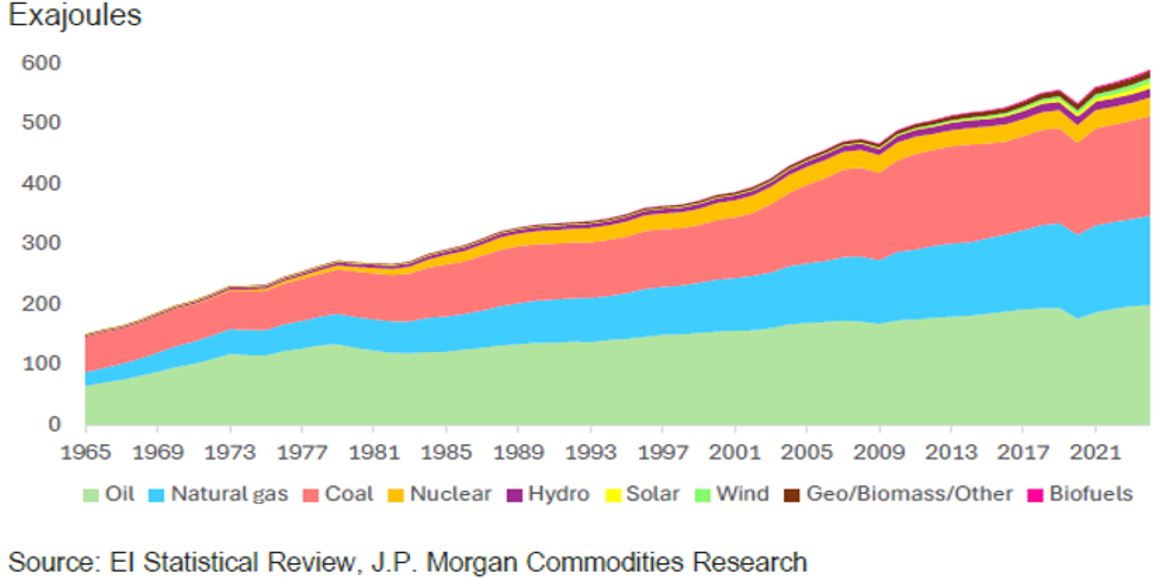

Overblown oil risk and the renaissance of renewable energy. At the start of the war, some oil experts speculated that oil price will temporarily spike above $140 and stay above $100 for a prolonged period, having modelled their views against the 1970s Arab oil embargo and Russia-Ukraine analogue. We disagree with the 1970s analogue just as we did during the second Russia-Ukraine war in 2022 arguing oil intensity have fallen dramatically and non-fossil fuel, including renewables and nuclear, now represent a larger share of energy mix.

A further lesson is that a combination of surging non-GCC oil exports – particularly from the US, which has increased exports by 50% – alongside coordinated stockpile releases and increased throughput from alternative routes such as Saudi Arabia’s East-West and the UAE’s Fujairah pipelines, has capped the surge in oil prices. Crude averaged $92/bbl during this period, rather than sustaining the $100-plus levels initially expected by many oil analysts.

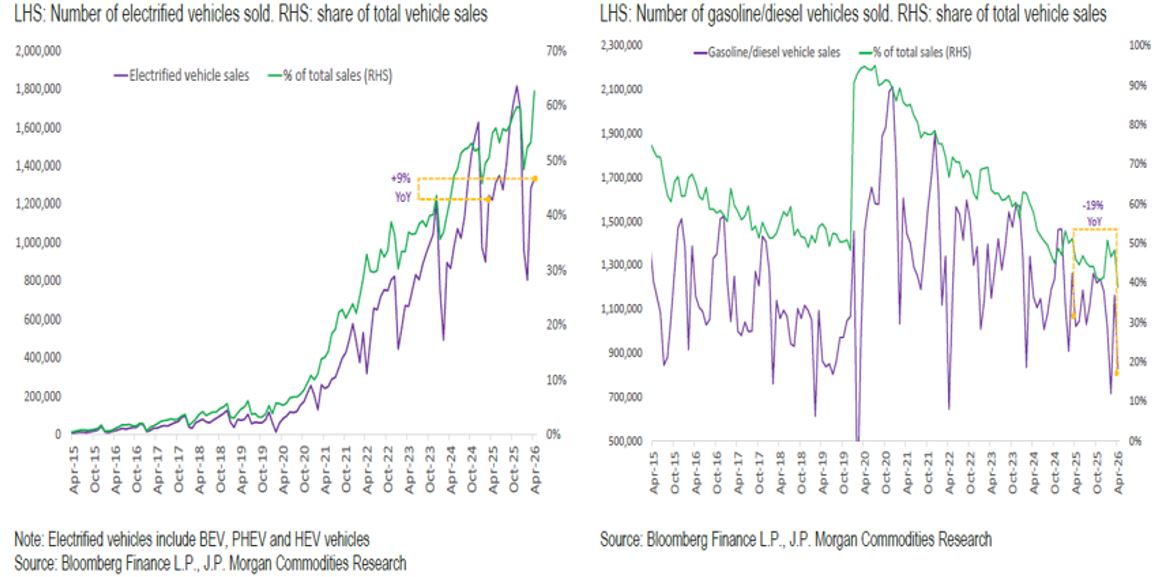

More importantly, the shock accelerated systematic substitution and demand destruction, with no country exemplifying this better than China. Already 6 out of 10 cars sold in China are EV cars. Immediately post-war, China EV sales saw a fillip of +9% yoy while conversely gasoline/diesel vehicles saw an accelerated decline of -19% yoy and now accounts for less than 30% of total vehicles sold during this period. We do not think this is just a China phenomenon. Global EV car market share since the Hormuz shock has increased 3.4pp to 27% of new car sales. During China’s last major national holiday, we also saw a significant switch from air travel to trains and cars as jet fuel spiked more than other transport fuels. This illustrates consumers are adaptive to alternative modes of transport and will switch to suit their budgetary needs.

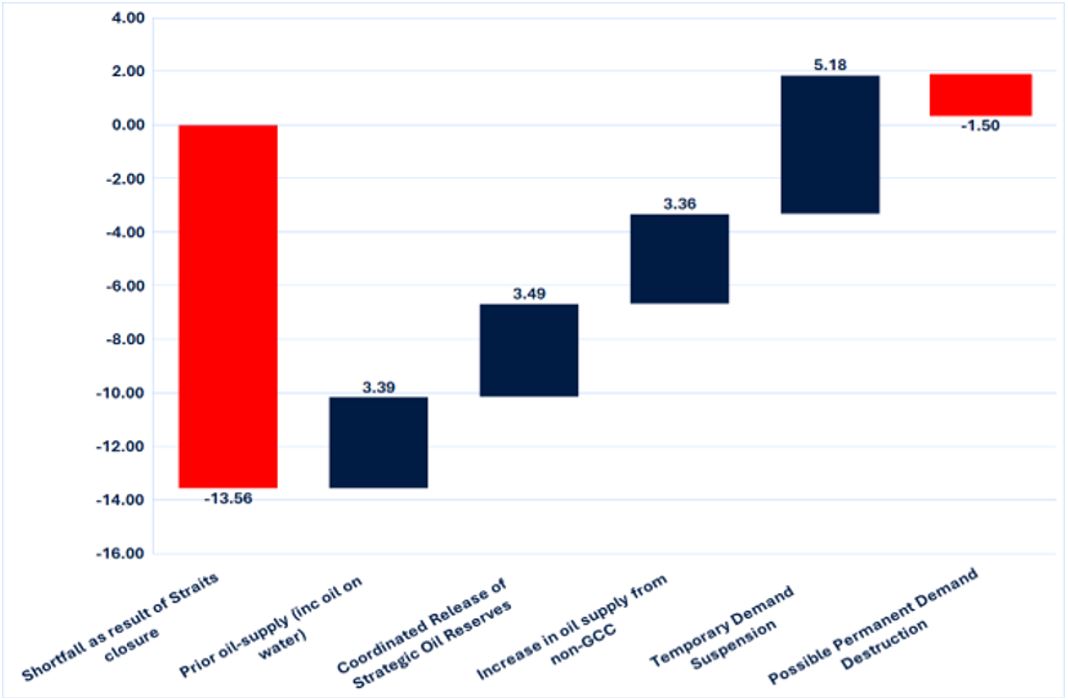

JPM estimates of the 6.68 mn b/d of demand destruction that has happened globally, about 1 to 1.5 mn b/d could be permanently destroyed through a combination of drivetrain substitution from ICE to EV, efficiency gains and material substitutions in manufacturing, and slow steaming and route optimization in shipping.

The more consequential lesson from the two recent oil crises is that energy security can no longer be taken for granted. The founding member of Singapore, Lee Kuan Yew, was once asked why Singapore liked to impose an assortment of fines. He replied human nature is such that without financial repercussions, one cannot institute behavioural changes. The rising sea tide, raging wildfires, and scorching temperature did not sustain climate investment. For most, these issues are someone else’s existential concerns, and in the current moment, they are mere short-duration discomforts until one becomes a casualty of it. It took an obvious military error by the US-Israel and an abhorrent brazen act of Iran in shutting the strait to trigger the renaissance of investment in clean energy.

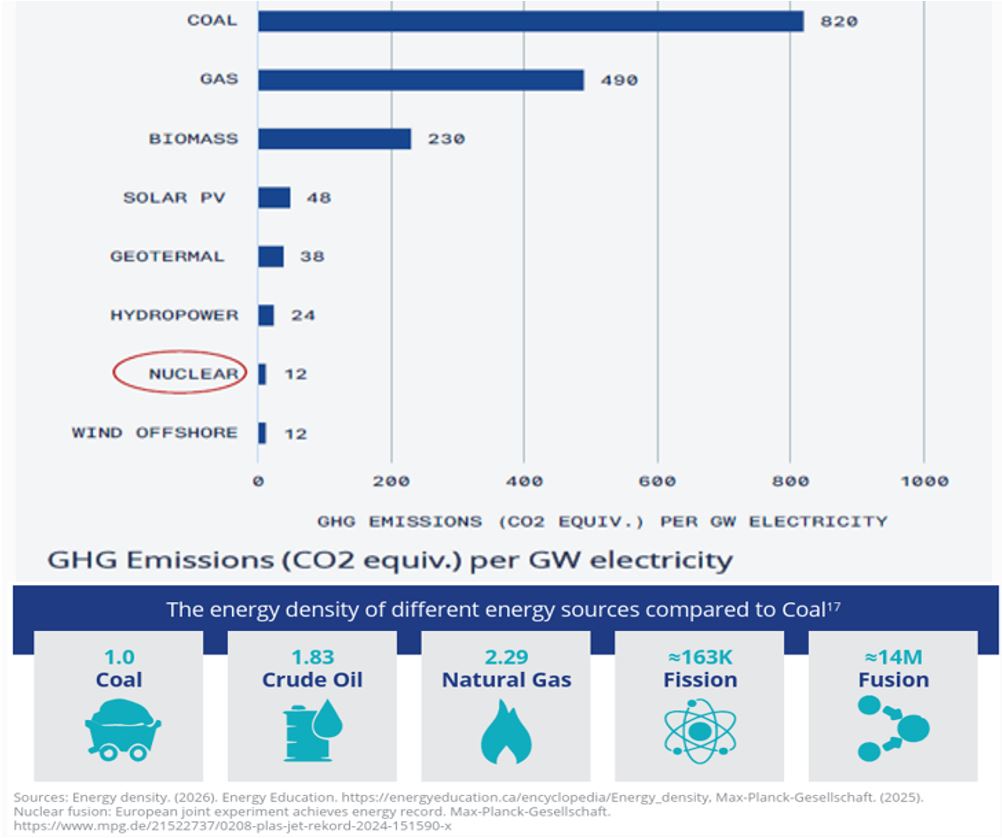

Of all the clean energy, the one we are most excited about is nuclear energy. Nuclear reactors are installed within one’s sovereign territory. They provide baseload availability, can be modulated, and are not subject to weather conditions. Nuclear produces larger energy density than any other sources and is also the second most environmentally friendly source after wind.

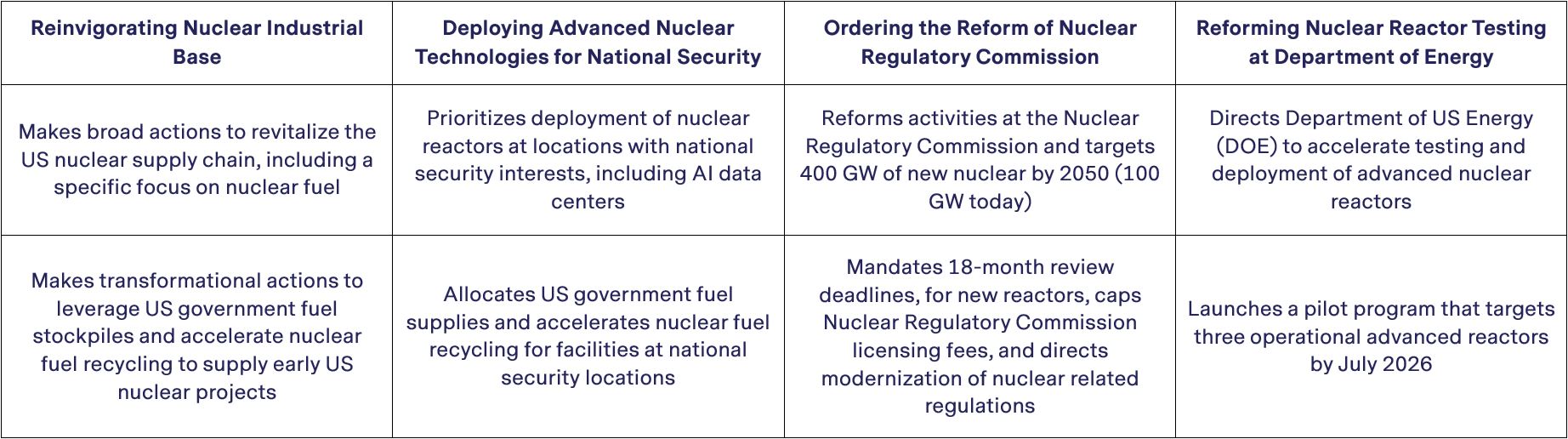

The Trump administration understands AI supremacy requires power supremacy, and it has been instrumental in jumpstarting this industry.

Technological improvements in mainstay fission technology using non-water coolant such as molten salt, gas or liquid metal have ushered improvements in fuel usage, less nuclear waste and are generally safer than water coolant reactors. Advocates of thorium instead of uranium reactors are being developed again. The benefit of Thorium reactor is it is significantly safer as they can be turned off in the event of an emergency, has a much shorter life, better energy production density than uranium reactors. And unlike uranium, thorium is less useful for weaponization.

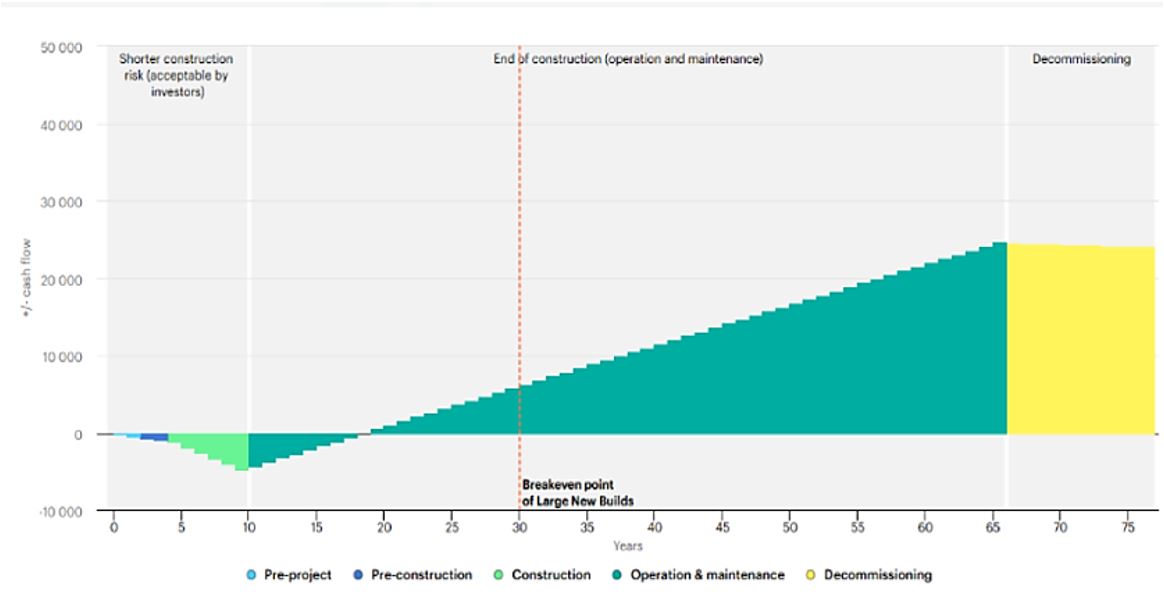

There have been several groundbreaking constructions of small modular fission reactor (SMRs) in China, Sweden, UK, and USA. Because SMRs are modular in design, they reduce construction costs and time to market significantly allowing cashflow breakeven by the 15th year; 10 years faster than large reactors.

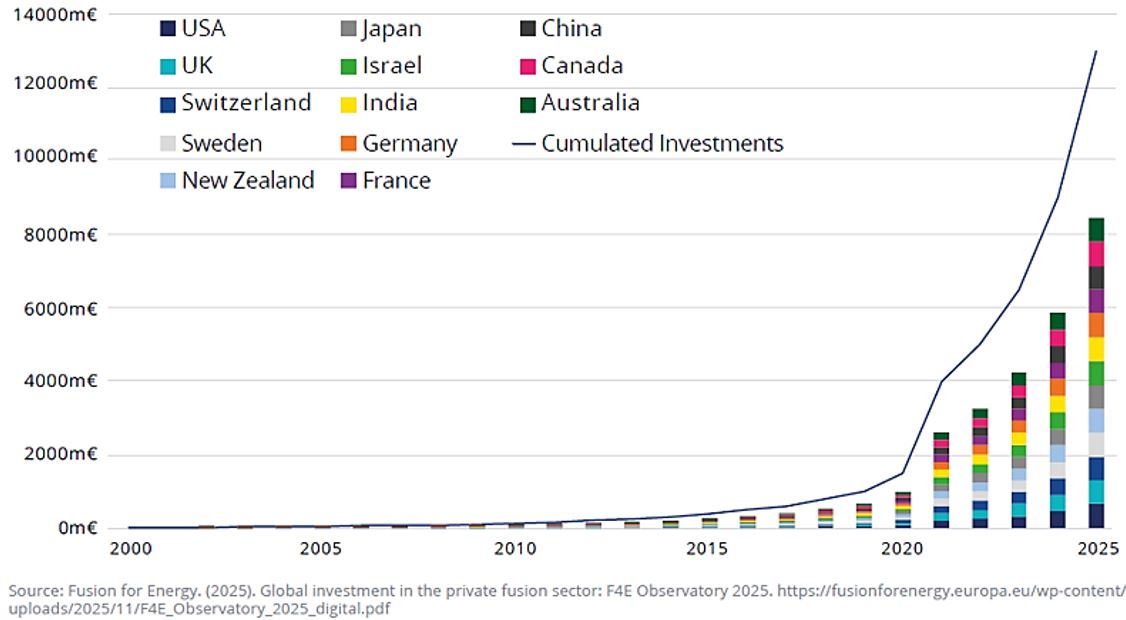

Investment in the holy grail of all energy sources, fusion technology, is also gathering pace. According to Fusion Industry Association, there has been a considerable increase in fusion technology investment. Total public-private sector investments in fusion technology amounted to $10bn in 2025 and year-to-date, it has already surpassed $10bn whereas the cumulative investment from 2020 to 2024 was only $7bn. There are significant milestones to watch out for.

Going long nuclear energy and shorting oil will be a multi-year trade.

2) Re-industrialization means higher capex: Catalysed by what happened after covid and compounded by the oil crisis of Russia-Ukraine and the Hormuz crisis, many governments have launched their own initiatives to reindustrialize and to onshore or friend shore key industries. But we will focus on the sovereign AI and the defense industries.

Jensen Huang coined the term “AI factories” and in many senses, today’s most important factories do not look like a steel mill or an automotive plant. They sit in vast tract of land, in windowless and temperature-controlled buildings, filled with servers, drawing vast amounts of electricity and turning data into economic output. Sovereign AI is not merely a technology policy; it is re-industrialisation by another name. In an era where productivity, security and economic competitiveness are increasingly shaped by compute, data and models, nations are treating AI infrastructure as the backbone of a new industrial base.

The plethora of announcements by various governments on investing in their own AI is just mind boggling. The US Stargate consortium intends to invest US$500bn over four years and explicitly frames the project as supporting America’s “re-industrialization” and national security. Across the Pacific, China is preparing a US$295bn, five-year plan to build a nationwide AI data-centre network. There is an additional of USD200bn devoted in deploying their semiconductor self-sufficiency and applications in robotics and quantum computing/ Europe, which has often been bogged down with regulation, is now responding with capital. The European Commission’s InvestAI aims to mobilise €200bn, including a €20bn fund for up to five AI gigafactories.

But it is Japan and South Korea’s announcements in the past few weeks that is a sticker shock. Japan has unveiled a 14-year investment roadmap targeting more than US$2.0tn across 17 strategic sectors. US$600bn is earmarked for AI and chips, US$65bn earmarked for physical AI investment in robotics and autonomous systems and another US$420bn for semiconductor development and mass production. South Korea’s announcement framed the plan around a “triple axis” of semiconductors, physical AI, and data centres. The investment in chip component is over US$576bn helmed by Samsung Electronics and SK Hynix to build four new chip fabrication plants in the southwest, plus US$52bn for a chip-packaging cluster near Seoul. It also targets a build out of data centre to the tune of $360bn by 2029 with an initial 8.4GW of AI data-centre capacity planned by SK, GS and Naver and the rising to US$1 trillion by 2035.

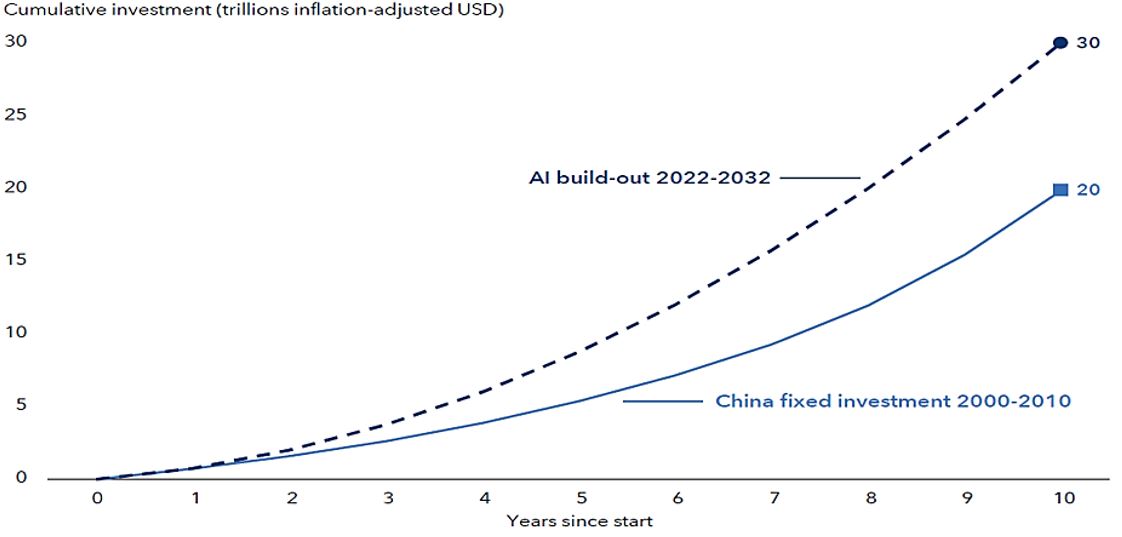

Capital Group estimates this AI buildout will be comparable to China’s modernisation push in the early 2000s, which was the largest industrial boom in modern history. After joining WTO, China invested a cumulative amount of $20 trn, they estimate AI build out into 2032 will gross over $30trn.

All of these announced initiatives signal a shift of view that AI is no longer viewed as a software layer, but as a foundational production system akin to building manufacturing capability, having the ability to develop downstream industrial and military applications, and to drive productivity gains especially for developed economies that is rapidly ageing. Critically, it is about retaining agency over their sovereign data and models too. Prefer infrastructure AI plays and we have some concerns of the rapid commoditization of frontier models.

Through Trump’s bellicose behaviour, all 32 NATO members have met the 2% GDP pa of defense spending target for the first time in 2025, with European allies and Canada increasing spending by 20% to $574 billion. Germany plans to more than double defense outlays to €162 billion by 2029, targeting 3.5% of GDP. NATO is now discussing a new 5% GDP target by 2032. It is worth noting Europe’s GDP growth has only been 1% in the last many decades, this increase in military spend is no insignificant change relative to their growth prospect. Many unconfirmed reports suggest that the critical US munitions are at a threshold of its operational requirement and will require accelerated replenishment, which could take two to three years, hence the recent activation of Defense Production Act in June.

What has happened in Iran has merely demonstrated US is equally quick to enter a war and exit with none of its strategic objectives achieved and yet wrought an unimaginable geopolitical crisis in the Middle East and energy shock to the world. All the US allies in the Pacific are astounded by US unilateralism and will surely be taken aback that despite all the pomp and ceremony, lavish gifts and the perceived security blanket that the web of US military bases in the GCC has adopted, Trump is willing to engender an Israeli hegemon in the region and leaving their region more fragile than before.

Facing an increasingly assertive China and an unreliable partner in the US, Japan has departed from its pacifist stance of over 80 years by increasing its spending from its historical less than 1% to 3.5% of GDP for the foreseeable years. South Korea too has been pressured by Trump to increase their spending, and it is expected to move to 3.5% of GDP in the near-term and 5% possibly. Taiwan has just increased their defense spending to 3.5% of GDP for the first time in 25 years. Buy defense and industrial complexes.

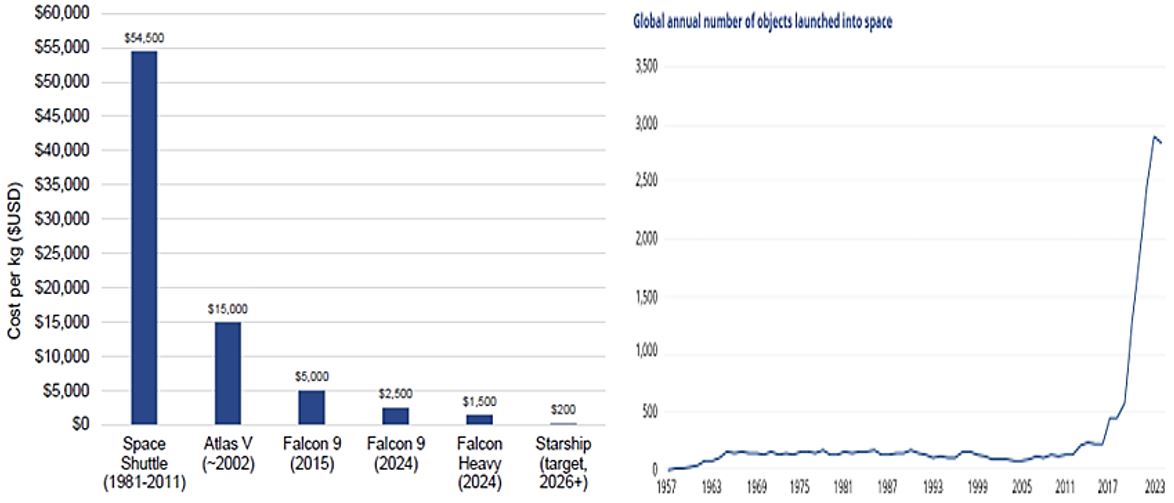

In 1914, in the opening hours of the war, Britain severed Germany’s undersea cables to impede their communications. Today that communication layer is migrating from the seabed and terrestrial to Low Earth orbit (LEO).

Two trends are converging that is making LEO the new frontier for science and for warfare. First, the economics of launching satellites in space is compounding fast. Reusable rockets have cut the cost of orbit to less than $200 per kg in a brief period of two and a half years, chiefly due to SpaceX’s reusable rockets technological feat. Second, this has led to connectivity expanding. JP Morgan estimates the coverage of LEO communication in 2025 was over nine million subscribers across 155-plus countries and that will double by the end of 2026. The undisputed leader in LEO is Starlink which controls three-quarters of active satellites. This single operator is already an omnipresent geopolitical asset for any military. In the early days of the second Russia-Ukraine war when Ukraine land-based communications were compromised, it was Elon’s Starlink that helped Ukraine coordinate their military responses and it is still now their dominant communication protocol.

LEO has now become the newest missile-defence layer. Of the $137 billion spent on space in 2025, defence took the majority for the first time ($73.5 billion versus $63.7 billion civil). According to the CBO, President Trump’s Golden Dome is expected to cost $1.2trn over the next twenty years. Every single country has either reorganised its military structures or created a new agency to achieve supremacy in space. Buy Space, not just SpaceX.

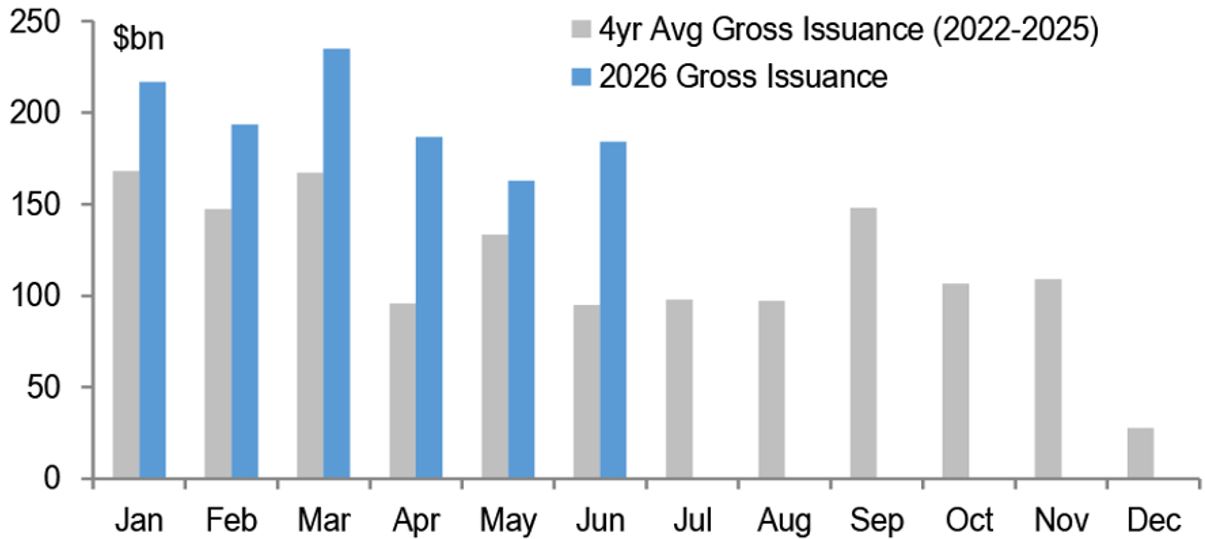

3) Capex will be large for the foreseeable future as many nations reconfigure their trade and industry, and security pacts in this multi-polar world. Demand for financing will be ratcheted higher whilst elevated level of government debt also risk of crowding out. All of this can snowball to push yields higher for longer.

As of mid-point of the year, the high-grade debt issuance in the US is now at a record of $1trn (of which $350bn are AI/Data Centre related issuance) and is up 27% yoy and that is off three consecutive years of record issuances. JP Morgan estimates a gross supply of $1.92 trn will be issued in 2026 and even after netting maturities, it would still be a $412bn increase in supply or 2.8x higher than already a record year in 2025!

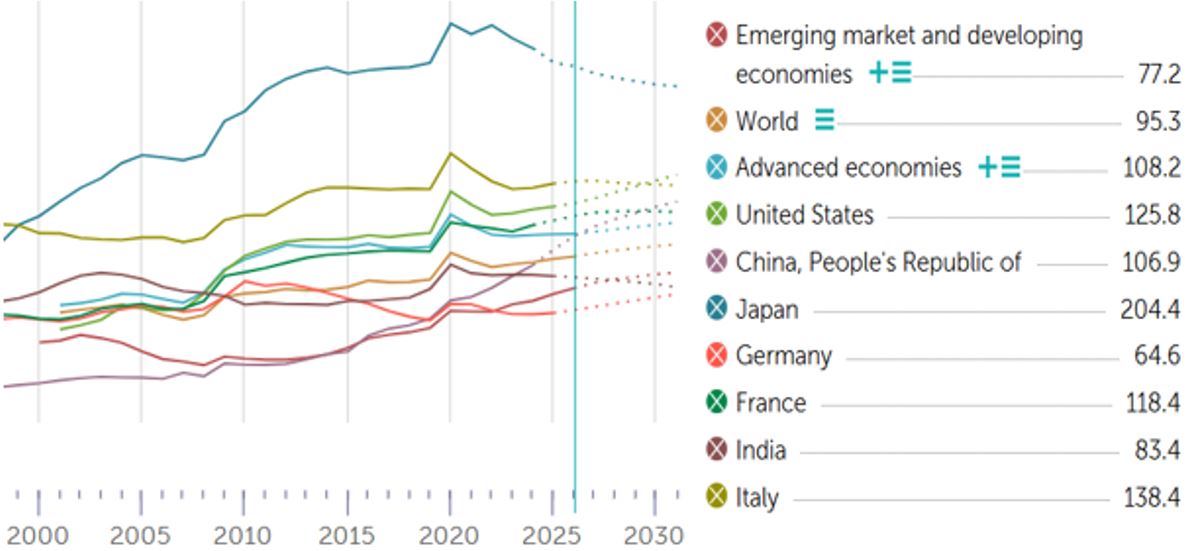

We wrote back in 2024, Now I Know When I Must Retire, “An aging demographics, the end of neoliberal economics, the rise of state-sponsored enterprises, the ascendance of the vox populi, and the emergence of a new world order” has translated to “the greatest transfer of debt from the consumer and the corporate sectors to the government”. Since then, public debt continues to rise as % of GDP in almost all developed countries and is projected by IMF to remain elevated for years to come. Empirically, IMF data shows when a country runs Debt/GDP above 100%, future growth prospects are impinged.

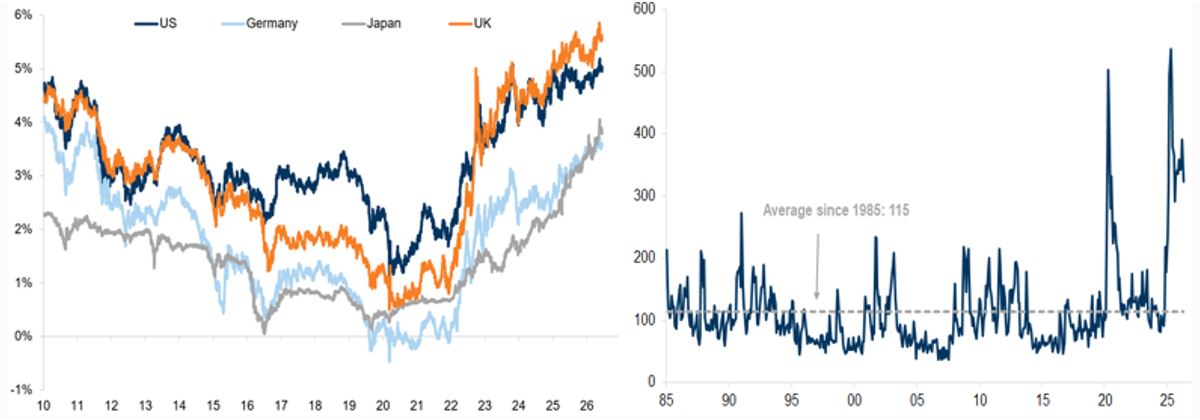

If you combine the increase in corporate debt issuance and bloated public debt, yields will remain high for longer. And if it does, it will make economies more vulnerable to moves in yields as it curtails policy flexibility. It also makes asset prices more vulnerable since the longer-dated end of the sovereign yield curve underpins a company’s cost of financing and an investor’s discounting mechanism for all assets.

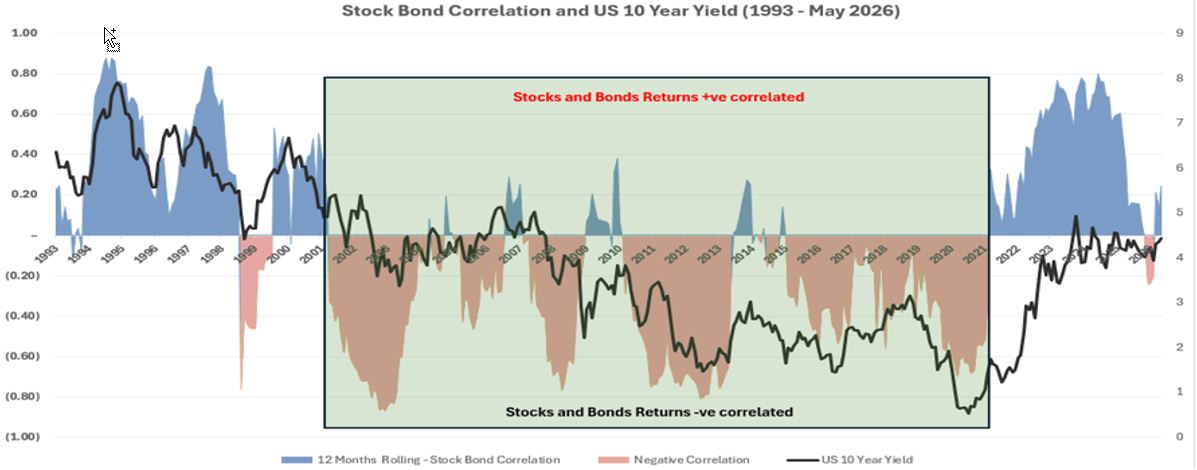

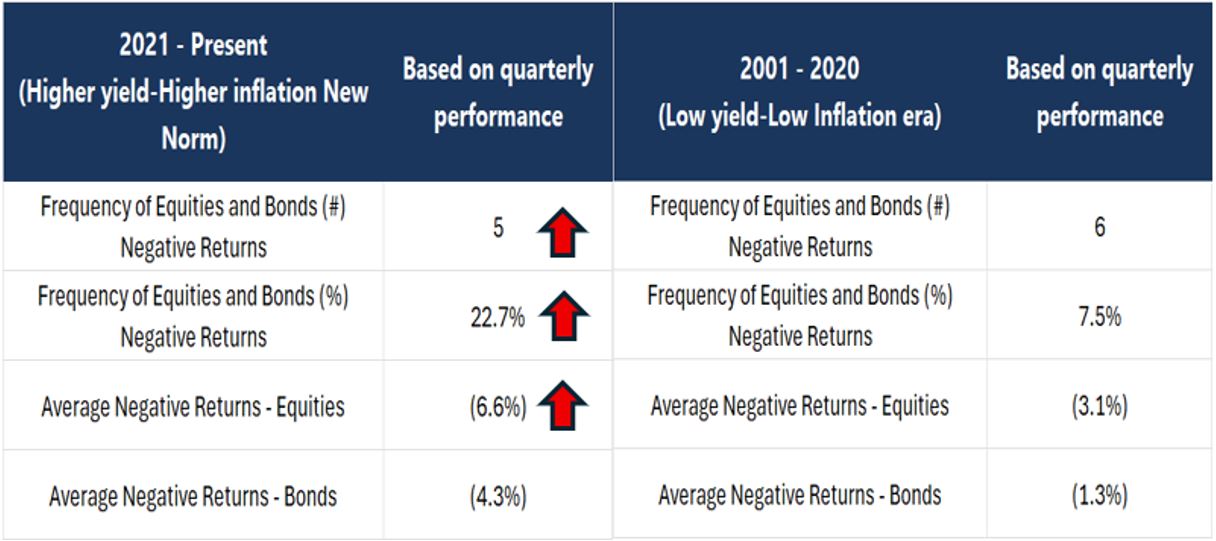

The most material and deleterious implication of a rising higher yield is it will challenge the 60/40 stocks/bond portfolio. Many of us have been schooled with the concept that bonds offer diversification to equities. But as shown in the chart below, the world is in motion. Yes, that adage has held true since the dot-com bust of 2001 until 2020 as stock and bond returns have been negatively correlated with only a few episodical convergences. But during that period, we have also seen yields on a downward trend driven by easy and unorthodox monetary policy (average yield was 3%), tepid inflation (average inflation was 2.0%) and with an embedded Fed’s put whenever equity vacillates; the late “Alan Greenspan’s Put”.

Prior to 2001, stock and bond have generally been positively correlated. Incidentally during that period, yields averaged 6.0% and inflation at 3.9% were higher as well. From 2021 onwards, after a 20-year hiatus, their returns have converged again. Post 2021, yields have started to climb out of the crazy world of ZIRP as the Fed and many other central banks begun their policy normalization in earnest. Inflation has been volatile but have trended higher averaging 4.5% driven by both structural and cyclical factors like ageing demographics, de-globalization, and the end of goods deflation from China. Furthermore, term premium of bond, compressed for two decades, have started to expand due to burgeoning indebtedness as investors priced in higher risk premium.

If stocks and bond returns are correlated to the upside, this would not be an issue. But what we are seeing is the frequency of both stocks and bonds generating negative returns has increased materially whenever they converge in the recent times. In the low inflation-low yields of 2001-2020, there were six occasions or 7.5% of the time stocks and bonds both fell on a quarterly basis; the figure is 10% if we use monthly performances. But from 2021 onwards, the frequency of negative outcomes has tripled to 23% based on a quarterly basis and more than doubled if based on a monthly performance. Whenever stock and bonds converge and had negative returns, the average declines in 2001-2020 were 3.1% and 1.3% based on quarterly and monthly data respectively. However, in recent periods, the average declines in equities and bonds have more than doubled to 6.6% and 4.3% on quarterly and monthly basis. There is a need to find better alternative to bonds as a diversifier to equities, cue in alternatives particularly semi-liquid hedge funds.

In our 2nd quarter Navigator aptly titled, Regime Change, we downgraded global growth and upgraded inflation outlook due to the ongoing war. Even as we expect global growth to be below potential, we ascribe a low probability of a recession or stagflation. Inflation will spike and stay higher for longer but have argued the Fed has never tightened due to supply shocks since their dual mandate was codified in 1977. Nonetheless, in a stable growth but rising inflation macro regime, empirically Equity returns fall to mid-single digit, Credit returns do not outpace Short-Term Treasuries, while Gold and Commodities tend to be stronger performers. Hedge funds made solid returns and when risk adjusted, it is the 2nd best performing asset class after short-term treasuries.

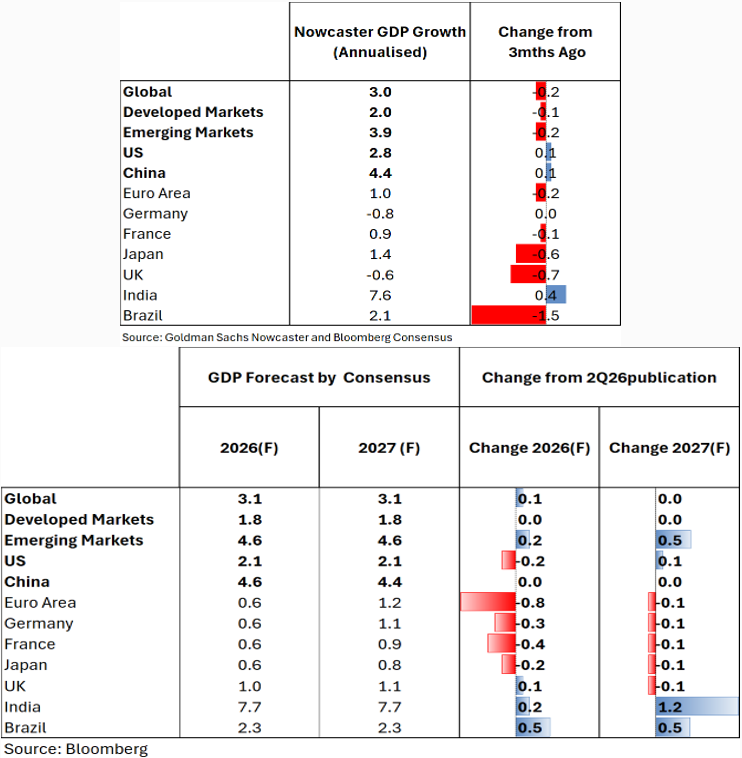

Our latest macro-clock remains in this regime of “Stable Growth but Rising Inflation.” Nowcasting model points to a below potential growth of 3.0%, 0.2ppt lower than 3 months ago with weaker reading across many countries. The downgrade to medium term consensus GDP forecast for 2026 and 2027 is unchanged for Developed Economies while Emerging Economies have slightly improved due to India, Brazil, and several oil-producing countries.

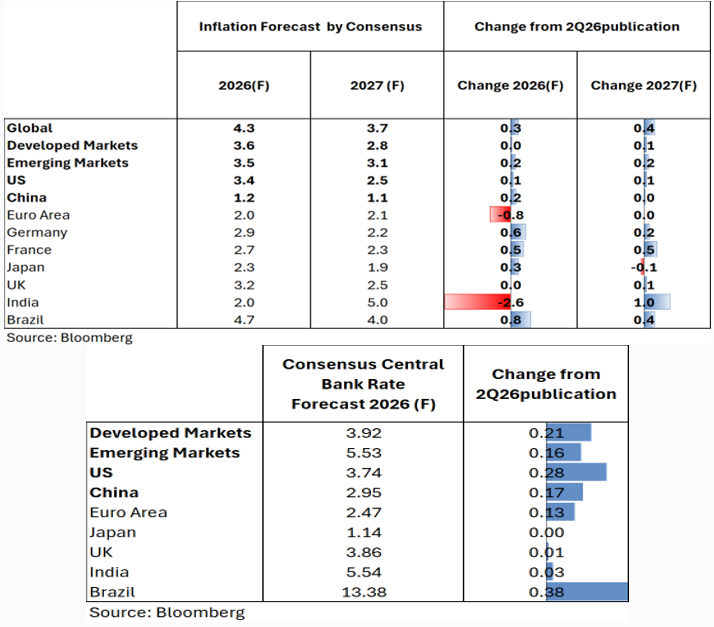

Inflation has been revised higher for both years across all regions for 2026 and 2027, but inflation is expected to peak in 2026. Because of rising and sticky inflation, central banks’ policy rates have increased for most key regions. As oil prices have retraced below $75, this fragile truce provides policy flexibility going into second half of the year after more than 35% of global central banks have raised their policy rates in the last 3 months.

Alternatives: The biggest beneficiary of the resumption of equity- bond correlation is semi-liquid hedge funds. Our approach towards investing in hedge funds is via a combination of more than a dozen managers that invest across equities, FX, rates, credit, deployed across equity long/short, macro, relative-value, and event strategies, and across the globe. This global oriented multi-manager, multi-asset, multi-strategy approach enables us to generate returns that are not correlated to bonds, and with much lower correlation and beta to broader equities. Speak to your wealth manager to find out more about fund of hedge fund (GARP).

Since 2021 when correlation re-converges, there were 17 occasions when both equities and bonds generated negative returns. During those episodes, equities averaged a negative return of -4.3% with the largest monthly decline was -9.2%. Bonds fell -2.4% on average and endured the steepest decline of -4.7%. GARP on the other hand had fewer negative monthly returns in the period when both equities and bonds were down with 9 such episodes. The average decline was inconsequential at -0.70% with a much smaller down of only -1.6%. That is a demonstrable conclusion that our fund of hedge funds is an effective return enhancer and risk diversifier.

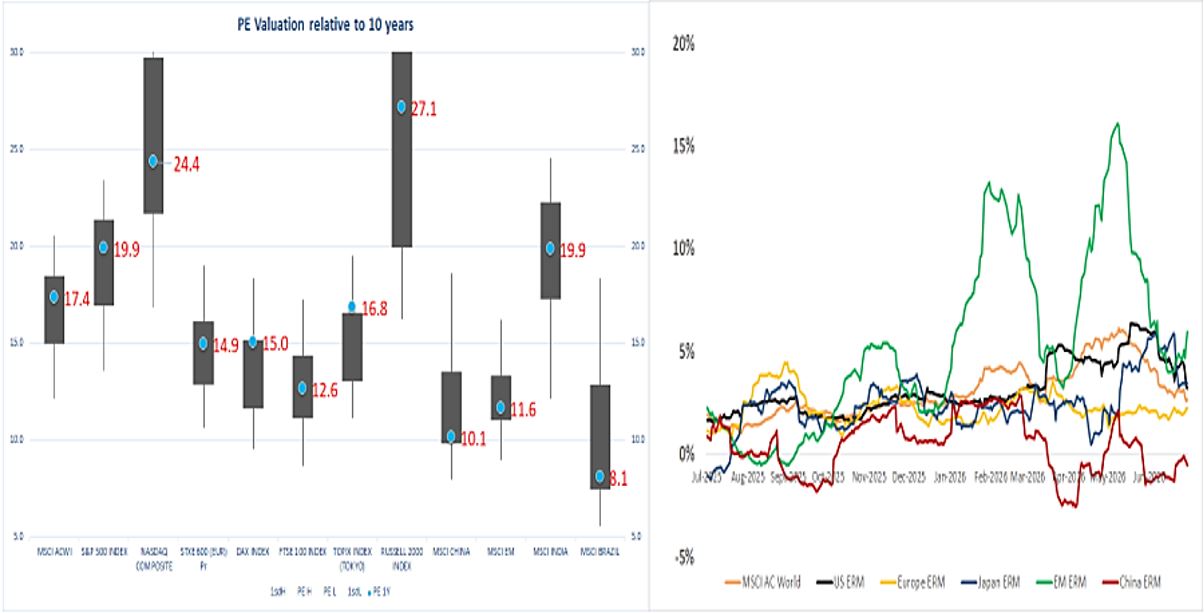

Equities: Neutral. Forward PE multiple for US market has derated by 4 ppt since the peak in Oct last year to 19-20x, which we believe is a fair multiple. The downgrade in multiple is not unusual and is in line with where the macro regime is and that of a late-stage bull cycle. But because of material upgrade in EPS from 15% at the start of the year to 27% currently, S&P500 has been able to return 8% so far. Unless we have a favourable shift in macro-regime either on growth or the interplay with inflation-policy rates, we believe the next 6-12 months return will still be governed by the pace of earnings upgrades particularly in the AI plays and hopefully the broadening of EPS upgrades from other non-tech sectors as well. For now, earnings revision momentum continues across all major regions except China. From a country perspective, we retain our preference for the US over all other markets. It is important to reiterate what we said at the start of the year that flash crash of more than -15% can happen even without a recession in a mature bull.

Fixed Income: Underweight. Our longer-term view of structurally elevated yields limits scope of capital appreciation in bonds; owning bonds here is less about capital appreciation and more about locking in income. While we are not advocating wholesale abandonment of bonds in a 60/40 portfolio as we enter a new correlation regime, it warrants holding a much lower weight in a multi-asset portfolio than history would suggest. We dispute market’s narrative that the next move by Fed is to raise rates. Growth in US labour market is slowing and is highly concentrated in only two sectors, even as monthly data is choppy. AI will lead to both destruction and displacement just as we have witnessed in the jobless recovery era of the early ‘90s when enterprise and consumer PC penetration increased. Contrary to market, we believe the next move for Fed is to cut rates although the cuts will likely be shallow. Staying in shorter duration investment grade bond and selectively in EM credits due to higher carry and also EM countries have been more disciplined than their developed counterparts in fiscal and monetary austerity.

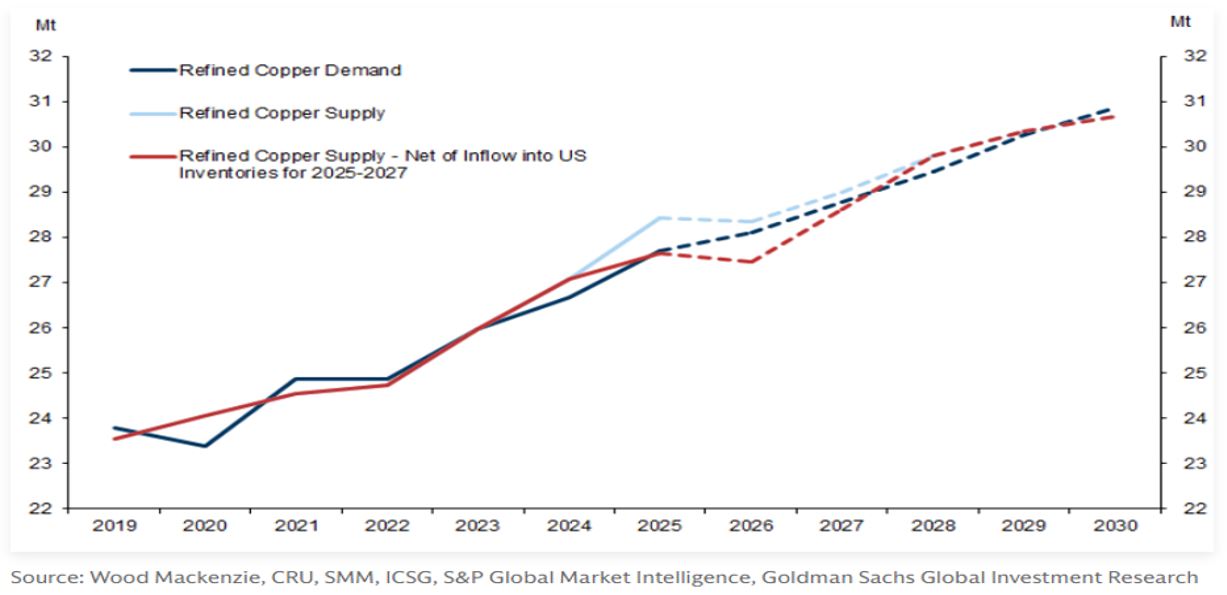

Commodities: The global initiatives we listed above are bullish for metals. From increased penetration of EV cars to further investment into renewable power generation which requires further grid investment, to larger defense spending and growing competition to win the AI race are highly supportive of copper, lithium, and aluminium demand. We prefer copper as it is easily accessible via ETF. Copper demand is expected to be anchored by grid and power infrastructure driving 60% of copper demand into 2030. Defense and electrification of transportation system are additional impetuses. On the supply side, growth remains lethargic from challenges in mining deeper and extracting lower yielding ore. Operating cost of mines have also increased for many. Copper is expected to be in undersupply until 2028. We have been disciplined selling Gold in the last 12 months, our position in gold is immaterial now, so are our bitcoin exposures both of which were hurt by rising yields and the exit of fast money accumulated in the preceding 12 months.

Cash: Holding more Short-term treasuries than Cash in this current macro set-up.

Featured Picture/Quote:

I may be a Liverpool fan, but I recognise talent, grit and yet light-heartedness.

Edward Lim, CFA

Chief Investment Officer

edwardlim@covenant-capital.com

Risk Disclosure

Investors should consider this report as only a single factor in making their investment decision. Covenant Capital (“CC”) may not have taken any steps to ensure that the securities or financial instruments referred to in this report are suitable for any particular investor. CC will not treat recipients as its customers by their receiving the report. The investments or services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to your circumstances or otherwise constitutes a personal recommendation to you. The price, value of, and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is affected by changes in a spot or forward interest and exchange rates, economic indicators, the financial standing of any issuer or reference issuer, etc., that may have a positive or adverse effect on the income from or the price of such securities or financial instruments. By purchasing securities or financial instruments, you may incur above the principal as a result of fluctuations in market prices or other financial indices, etc. Investors in securities such as ADRs, the values of which are influenced by currency volatility, effectively assume this risk.

By entering this site you agree to be bound by the Terms and Conditions of Use. COVENANT CAPITAL PTE LTD (“CCPL”) is a Capital Markets License (AI/II) holder and regulated by the Monetary Authority of Singapore (‘MAS’).

By using this site you represent and warrant that you are an accredited investor or institutional investor as defined in the Singapore Securities and Futures Act (Chapter 289). In using this site users represent that they are an accredited and/or Institutional investor and use this site for their own information purposes only.

The information provided on this website by Covenant Capital Pte Ltd (CCPL) is intended solely for informational purposes and should not be construed as investment advice. It does not constitute legal, tax, or other professional advice. CCPL strongly recommends consulting qualified professionals for personalized guidance. The website does not offer or solicit securities transactions, and users are expected to comply with local laws. Accredited and institutional investors in Singapore may access the information solely for informational purposes.

What types of Personal Data do Covenant Capital collect?

Personal data is any information that relates to an identifiable individual, and we may collect this information when you interact with our staffs:

1. Personal Particulars (e.g. name, address, date of birth)

2. Tax, Insurance and employment details

3. Banking information and financial details

4. Details of interactions with us (eg. Images, voice recordings, personal opinions)

5. Information obtained from mobile devices with your consent

How do we collect your Personal Data?

Below are the ways that we collect your data:

1. Investment Management Agreement forms, Risk Profile forms, Subscription forms;

2. Via emails, SMSes, Whatsapps, phone calls or any other digital means to the office or its’ staffs;

3. Photos and videos of you from our events; and

4. Information about your use of our services and website, including cookies and IP address

How do we use your Personal Data?

1. For General Support

Verify your identity before providing our services, or responding to any of your queries, feed-back and complaints.

2. For our Internal Operations

a. Aid our analysis so that the company can improve our services and products.

b. Manage the company’s day-to-day business operations.

c. Ensure that the information that the company have on you is current and up to date.

d. Conducting Due Diligence checks to reduce Money Laundering and Terrorist

3. Financing Schemes

e. Comply with all laws and obligations from any legal authorities.

f. Seek professional advice, including legal.

g. Provide updates to you.

4. Posting on LinkedIn and Website

We may post personal data, including pictures and videos, on our LinkedIn page and website for purposes such as:

Who do we share your Personal Data with?

1. Any officer or employee of the company and its related companies;

2. Third parties (and their sub-contractors if applicable) that works with us, such as Custodian Bank of choice, Fund Administrators for the Funds that we manage, any third party Fund’s Administrators, IT support who back up our database and other service providers;

3. Relevant authorities such as government or regulatory authorities, statutory bodies, law enforcement agencies.

4. Relevant authorities such as government or regulatory authorities, statutory bodies, law enforcement agencies.

5. We require all personnel of the company and third party to ensure that any of your data disclosed to them is kept confidential and secure

6. We do not sell your Personal Data to any third party, and we shall comply fully with any duty and obligation of confidentiality that governs our relationship with you

When the company discloses your personal data to third-parties, the company will, to the best of its abilities, exercise reasonable due diligence that they are contractually bound to protect your personal data in accordance with applicable laws and regulations, save in cases where by your personal data is publicly available.

Accessing and Correction Request and Withdrawal of Consent

Please contact your advisor/banker or alternatively you can contact ccops@covenant-capital.com should you have the following queries.

1. Regarding the company’s data protection policies and processes

2. Request access to and/or make corrections to your personal data in the company’s possession; or

3. Wish to withdraw your consent to our collection, use or disclosure of your personal data.

The company endeavours to respond to you within 30 days of the submission.

Should you choose to withdraw your consent to any or all use of your personal data, the company might not be able to continue to provide any further services or maintain further relationships. Such withdrawal may also result in the termination of any agreement or relationship that you have with us.

Complaints

If you wish to make a complaint with regards to the handling and treatment of your personal data, please contact the company’s Data Protection Officer, mentioned below, directly. The DPO shall contact you within 5 working days to provide you with an estimated timeframe for the investigation and resolution of your complaint.

Should the outcome of the resolution is not satisfactory, you may refer to the Personal Data Protection Commission (PDPC) for any further resolutions.

If you have any doubt, please contact Mr Tay Kian Ngiap, the PDPA Data Protection Officer for Covenant Capital Pte. Ltd. He can be reached at kntay@covenant-capital.com

By accessing this website, you hereby agree to the terms listed on the website, all applicable laws and regulations, and agree that you are responsible for compliance with any applicable local laws. Any claim relating to Covenant Capital’s website shall be governed by the laws of the Republic of Singapore without regard to its conflict of law provisions.

1. License to Use

Permission is granted to download information and materials on Covenant Capital’s website for personal, non-commercial viewing only. This is the grant of a license, not a transfer of title, and under this license you may not:

i) modify or copy the information and materials;

ii) use the information and materials for any commercial purpose, or for any public display (commercial or non- commercial);

iii) attempt to decompile or reverse engineer any software contained on Covenant Capital’s web site;

iv) remove any copyright or other proprietary notations from the materials; or

v) transfer the materials to another person or “mirror” the materials on any other server.

All content, including but not limited to logo, tagline, graphics, images, text contents, buttons, icons, design and structure are property of Covenant Capital. All content on this website is protected by copyright, patent and trademark laws.

The Covenant Capital logo should not be used for any purpose whatsoever beyond what is available on the website, unless you have obtained written approval from us.

2. Disclaimer

The materials on Covenant Capital’s website are provided “as is”. Covenant Capital makes no warranties, expressed or implied, and hereby disclaims and negates all other warranties, including without limitation, implied warranties or conditions of merchantability, fitness for a particular purpose, or non-infringement of intellectual property or other violation of rights. Further, Covenant Capital does not warrant or make any representations concerning the accuracy, likely results, or reliability of the use of the materials on its Internet web site or otherwise relating to such materials or on any sites linked to this site.

It is your responsibility to evaluate the accuracy, completeness, or usefulness of any information, advice and other content available through this website.

You should not solely rely on the information, advice and other contents available on our website for decisions on investment(s) or decision with respect to our company’s products and services. You are advised to seek additional information required for you to make sound, well-informed and reasonable decision.

3. Limitations

In no event shall Covenant Capital or its suppliers be liable for any damages (including, without limitation, damages for loss of data or profit, or due to business interruption,) arising out of the use, inability to use or user’s reliance on the materials obtained through Covenant Capital’s web site, even if Covenant Capital or a Covenant Capital authorized representative has been notified orally or in writing of the possibility of such damage.

4. No Offer

Nothing in this website constitutes a solicitation, an offer, or a recommendation to buy or sell any investment instruments, to effect any transactions, or to conclude any legal act of any kind whatsoever. The information on this web site is subject to change (including, without limitation, modification, deletion or replacement thereof) without prior notice. When making decision on investments, you are advised to seek additional information required for you to make sound, well-informed and reasonable decision.

5. Revisions and Errata

The materials appearing on Covenant Capital’s website may include technical, typographical, or photographic errors. Covenant Capital does not warrant that any of the materials on its website are accurate, complete, or current. Covenant Capital may make changes to the materials contained on its website at any time without notice. Covenant Capital does not, however, make any commitment to update the materials.

6. Site Terms of Use Modifications

Covenant Capital may revise these terms of use for its web site at any time without notice. By using this website you are agreeing to be bound by the then current version of these Terms and Conditions of Use. If any of the term or change is deemed not acceptable to you, you should not continue to browse this site.

Your privacy is very important to us and we respect your online privacy. This Policy has been developed in order for you to understand how we collect, use, communicate and disclose and make use of personal information. We are committed to conducting our business in accordance with these principles in order to ensure that the confidentiality of personal information is protected and maintained.

1. Collection and Use of Information

We may collect personal identifiable information, such as names, postal addresses, email addresses, etc., when voluntarily submitted by visitors to our website. This information is only used to fulfill your specific request, unless further permission is provided to us to use it in any other manner or for any other purpose.

2. Web Cookies / Tracking Technology

A cookie is a small file which seeks permission to be placed on your computer’s hard drive. Once you are agreeable to the use of cookies, the file is added and the cookie helps analyse web traffic and tracks visits to a particular website. Cookies allow web applications to respond to you as an individual. The web application can tailor its operations to your needs, likes and dislikes by gathering and remembering information about your preferences.

We use traffic log cookies to identify which pages are being used. This helps us analyse data about website traffic and improve our website in order to tailor it to customer needs. We only use this information for statistical analysis purposes and then the data is removed from the system.

Overall, cookies help us provide you with a better website by enabling us to monitor which pages you find useful and which you do not. A cookie in no way gives us access to your computer or any information about you, other than the data you choose to share with us.

You can choose to accept or decline cookies. Most web browsers automatically accept cookies, but you can usually modify your browser setting to decline cookies if you prefer. This may prevent you from taking full advantage of the website.

3. Links to other websites

Our website may contain links to other websites of interest. However, once you have used these links to leave our site, you should note that we do not have any control over that other website. Therefore, we cannot be responsible for the protection and privacy of any information that you provide whilst visiting such sites, and this privacy statement does not govern such sites. You should exercise caution and review the privacy statement applicable to that particular website.

4. Distribution of Information

We will not sell, distribute or lease your personal information to third parties unless we have your permission or are required by law to do so. We may use your personal information to send you promotional information about third parties’ products or services, which we think you may find interesting if you tell us that you wish this to happen.

If you believe that any information we are holding on you is incorrect or incomplete, please write to or email us as soon as possible at the above address. We will promptly correct any information found to be incorrect.

When required by law, we may share information with governmental agencies or other companies assisting in the investigations. The information is not provided to these companies for marketing purposes.

5. Commitment to Data Security

To make sure your personal information is secured, we communicate our privacy and security guidelines to all Covenant Capital’s employees and strictly enforce privacy safeguards within the company.

Your personal identifiable information is kept secure. Only authorised employees, agents and contractors who have a direct need to access the information will be able to view this information.

We reserve the right to make changes to this policy. Any changes to this policy will be posted.